Peak Venture Capital

Predatory behavior by largest VCs is bad for business in the long run

Intel (INTC; $142B) was founded in July of 1968 by Robert Noyce and Gordon Moore, who had raised $2.5 million in capital to start their new company. Within about three years, Intel went public at a market cap of $70.5 million, or ~$530 million in current dollars. Today, the U.S. is home to over 1,200 unicorns (private firms with valuations over $1 billion).

What better way to follow-up last week’s coverage on the IPO market than with a look at venture capital, which has been in a sustained downturn for almost 18 months. Exit value is on pace to finish the year just over $20 billion, which would be the lowest in the past decade by almost $50 billion. Initial public offerings have not been viable options for VC-backed companies in 2023, despite the 34% gain in the Nasdaq Composite.

Fred Wilson, a co-founder of Union Square Ventures and investor in startups including companies like Twitter, Tumblr, and Coinbase, frequently shares his observations on trends in the venture capital industry. From his latest note:

“Private capital markets, like venture capital, lag public markets by a few quarters. That is because it takes time for private market investors to react to the public markets. The NASDAQ peaked in Nov 2021, but VC markets did not really start slowing down until the second quarter of 2022.

Now that the NASDAQ has posted a couple of strong quarters, I would expect venture capital to respond. But it won’t happen overnight. We are in the summer doldrums. It takes time for VCs to raise new funds. And deals take months to come together.

So my guess is we are mostly through this downturn. We will know for sure in a couple of quarters.”

Do most investors even care? Certainly not anyone focused on Third Stream Research’s universe of companies with market capitalizations up to $1 billion and a median market cap of ~130 million. Besides, VC-backed companies, along with the smallest IPOs, have severely underperformed in recent years.

By the time the vast majority of venture-funded companies go public, they debut on the stock market as mid-caps or large-caps. Shepherded by the major investment banks and touted by factions of sell-side analysts, the former unicorns are fawned over by the financial media, while their CEOs transform into reality-show celebrities for CNBC and other outlets.

Take, for example, Forbes’ ‘Midas List’, which an annual ranking of the top 100 VC investors who have scored the biggest wins in the hottest technologies, including service platforms, blockchain and AI. This recognizes early investors who benefit from windfall profits following the liquidity event—but what trickles down to post-IPO investors? Bupkis.

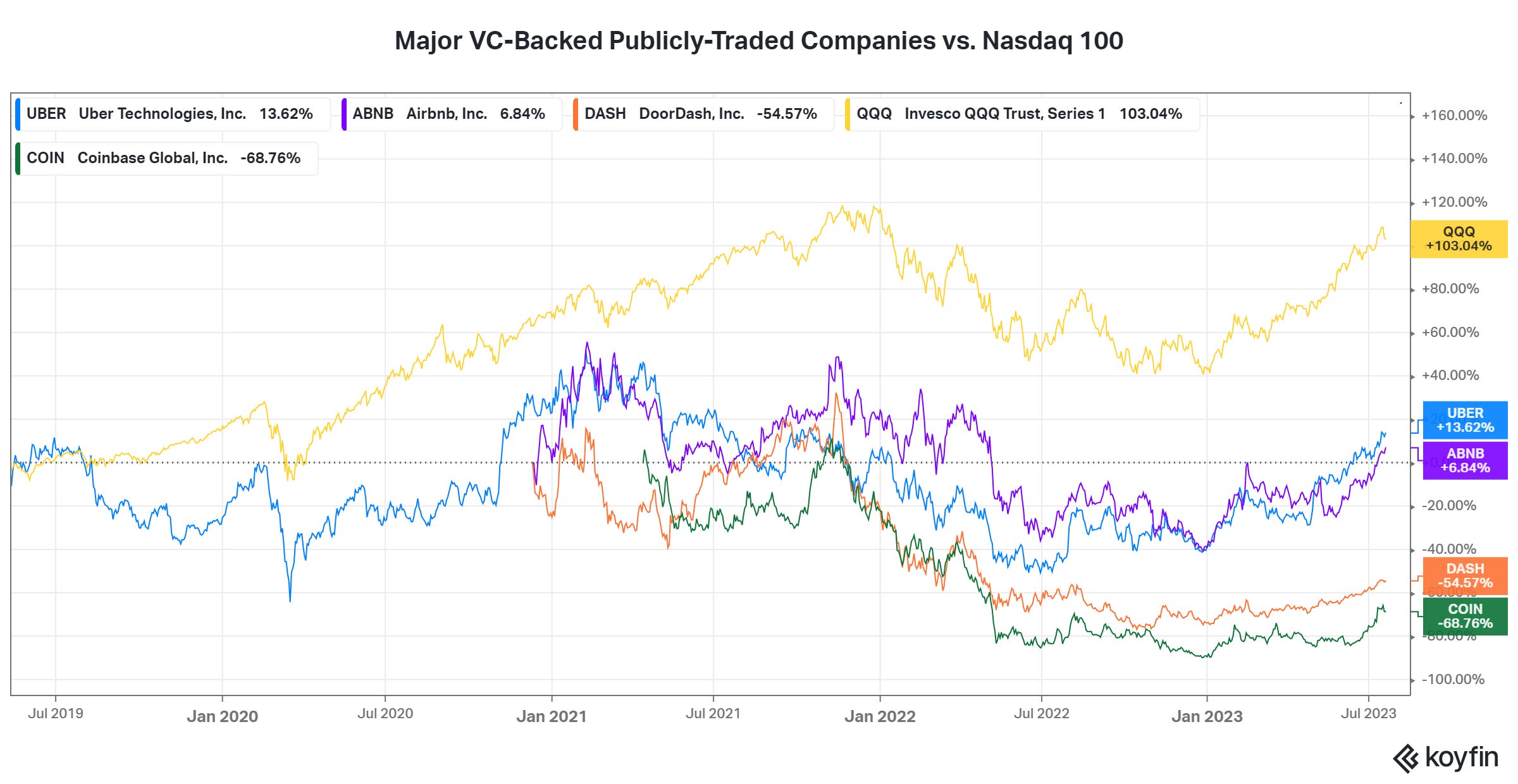

Notably, the four largest VC-backed IPOs since 2019 have delivered embarrassingly weak performances. As the chart below shows, the quartet has been decimated by the Nasdaq-100.

The following data tells the tale of woe for the majority of investors late to the party:

Uber Technologies (UBER; $95B)

Funded by 115 investors and raised ~$25.2 billion in funding over 32 rounds.

IPO Date: May 2019

Offering Price: $45.00

Opening Price: $42.00

Current Price: $47.23

Airbnb, Inc. (ABNB)

Total of 81 investors. Raised ~$6.4 billion in funding over 30 rounds.

IPO Date: December 2020

Offering Price: $68.00

Opening Price: $146.00

Current Price: $148.77

DoorDash, Inc. (DASH; $33B)

Total funding of $2.5 billion in over 13 rounds, with Series H being the latest funding round in July 2020.

IPO Date: December 2020

Offering Price: $102.00

Opening Price: $182.00

Current Price: $184.29

Coinbase Global (COIN; $23B)

Total funding of $498.7 million from 75 investors.

IPO Date: April 2021

Offering Price: $250.00*

Opening Price: $381.00

Current Price: $99.32

*Coinbase chose the direct listing path to the public market rather than pursuing a traditional IPO. That means instead of raising cash by selling new shares to a group of institutional investors, Coinbase allowed existing stakeholders to start selling immediately at a market-driven price.

To make things worse, overanxious investors who jumped in on the first day of trading experienced short-lived gains; those who held longer were likely to have been hammered with losses.

Venture Predation: Unmasking the Silicon Valley Grift

Predatory pricing has long been a strategy used by firms to stifle competition, but a new breed of company is taking it to a whole new level. Lawyers Matt Wansley and Sam Weinstein, colleagues at the Yeshiva University’s Cardozo School of Law, make their case in a research paper entitled “Venture Predation.”

Big venture-backed startups, fueled by massive infusions of capital from VCs, are using predatory pricing to drive rivals out of the market and secure a dominant position. While the Supreme Court has historically considered predatory pricing rare and rarely successful, venture predators see it as a potentially lucrative strategy worth pursuing.

The rise of Uber is a prime example. By initially offering attractively low fares, Uber rapidly gained market share and disrupted the traditional taxi industry. However, the company's success was sustained by fat VC subsidies, while Uber racked up heavy losses.

Unlike traditional predators, venture predators don't necessarily need to recoup their losses to succeed. Their primary objective is to create the perception of potential recoupment, enticing investors who anticipate future monopolistic pricing. This approach, however, has social costs. It distorts price signals, misallocates capital, and ultimately harms consumers through reduced choices and stifled product innovations.

Adam Rogers, writing for Insider, sums it up this way:

“Let's be clear here: This isn't the traditional capitalist story of ‘you win some, you lose some.’ The point isn't that venture capitalists sometimes invest in companies that don't make their money back. The point is that the entire model deployed by VCs is to profit by disrupting the marketplace with predatory pricing, and leave the losses to the suckers who buy into the IPO. A company that engages in predatory pricing and its late-stage investors might not recoup, but the venture investors do.”

Wansley and Weinstein propose two types of interventions to combat venture predation:

First, antitrust law could be reformed, removing hurdles in suing venture predators; eliminating the recoupment requirement or proving investor expectations of recoupment could deter predatory practices and protect competition.

Second, securities regulation reforms could increase transparency for private companies, exposing venture predators sooner and thwarting their strategies.

Finally, Wansley and Weinstein ask: Will Uber ever recoup the losses from its sustained predation?

“We do not know. Our point is that, from the perspective of the VCs who funded the predation, it does not matter. All that matters is that investors were willing to buy the VCs’ shares at a high price. The VC firm Benchmark, which led Uber’s Series A round, generated a return of about $5.8 billion on its investment.”

In 2022, Uber reported net revenues of $31.87 billion and yet it posted a net loss of $9.14 billion. The company has been in business for over 14 years. Go figure.

See you next week.

Josh

Connect with me on Twitter and LinkedIn.

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. Joshua Levine and Third Stream Research were not compensated by any company, directly or indirectly, mentioned in Confluence, and we do not own shares in any companies mentioned.