The bear market last year forced many private companies to rethink their plans to go public. This hit Wall Street where it hurts.

Investment bankers remain somber, having lost opportunities for lucrative fees from arranging IPOs and other equity sales. Uncertainties over monetary policies, including the direction of interest rates and concerns surrounding a potential economic downturn, helped to erode confidence in the financial markets.

Globally, IPO activity managed to sustain activity. According to S&P Global, there were 1,671 IPOs worldwide in 2022. But money raised was less than $180 billion, down from $627 billion in 2021.

In the U.S., however, the IPO market in 2022 was in a near-depression. Initial public offerings totaled just 38, down from 311 in 2021, the biggest year since 2000. Last year marked the second-lowest annual number of deals since 1980, with aggregate proceeds of $7 billion—the stingiest amount raised since 1990.

The world of finance has become increasingly dominated by big institutions and their desires. This evolution, which includes the removal of crucial incentives associated with smaller IPOs in the emerging growth market, has caused smaller deals to be overwhelmed by larger raises for fewer companies. Lots of things factored into this shift, most notably the ascension of the venture capital industry and the decimalization of the U.S. stock market in 2001.

Today’s dominance in new issues by powerful financial institutions is best illustrated with this data:

From 1983 to 2000, 6,179 IPOs were launched; this compares to 2,608 go-public offerings between 2001 and 2022.

Average money raised in an IPO in 1995-2000 was $96.6 million. In 2021-2022, it was nearly 4x at $362 million.

While many private companies are delaying their IPO plans due to 2023’s challenging environment, a smattering of fresh faces realized their dream. Still, you know it’s tough out there when amidst the mania for all things associated with artificial intelligence, there has been a dearth of IPOs for AI software companies.

When Barron’s Eric Savitz recently asked Lise Buyer of Class V Group about this, she answered as follows:

“Most AI software companies don’t have enough there yet to go public,” Buyer says. “If this were 2021, companies with hope and a good story could go. Today, it takes more than that. Public-market investors have no interest in being the greater fool. They can ride the AI wave with Microsoft, Alphabet, and Nvidia. Other than OpenAI, which could probably go tomorrow, others will have to show something very tangible before the institutional investors dive in.”

Additionally, a pipeline of star IPO candidates are biding their time. Popular tech companies such as ARM Holding, Discord, Reddit, Databricks, and Stripe are among the prospects that could potentially go public over the next 6 to 12 months.

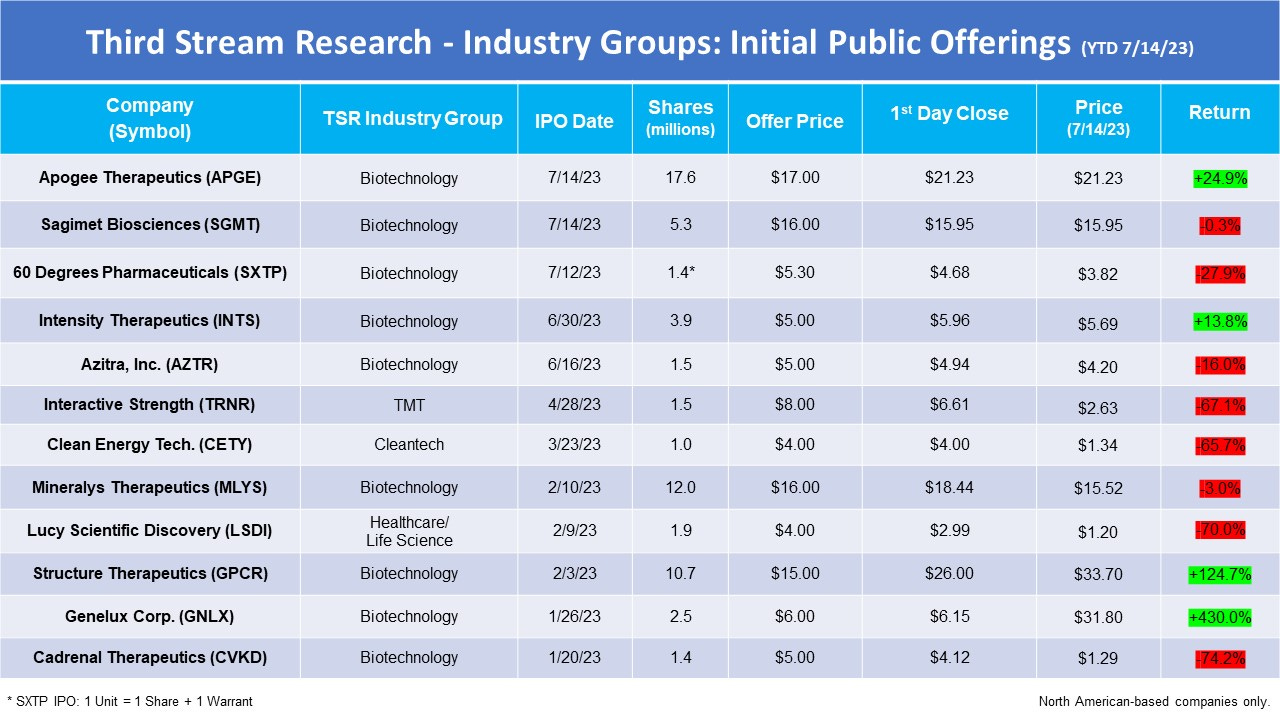

Third Stream Research – Industry Groups: IPOs in 2023

Third Stream Research tracks 1,200+ North American-based companies in the TMT, Biotechnology, Healthcare/Life Science, Medical Devices, and Cleantech industries with market capitalizations up to $1 Billion.

Reviewing the performances of the 20 IPOs in 2022 within our universe of coverage, we find that only 3 currently trade above their offer price. Of the 17 below this price point, 11 are down more than 50% and 8 have plunged at least 80%.

A track record so awful does little to bolster investors’ faith in the process of taking small companies public. However, on a positive note the 3 winners—Nuvectis Pharma (NVCT; $235M), Belite Bio (BLTE; $441M), and Applied Digital (APLD; $775M)—are up +198%, +170%, and +60%, respectively.

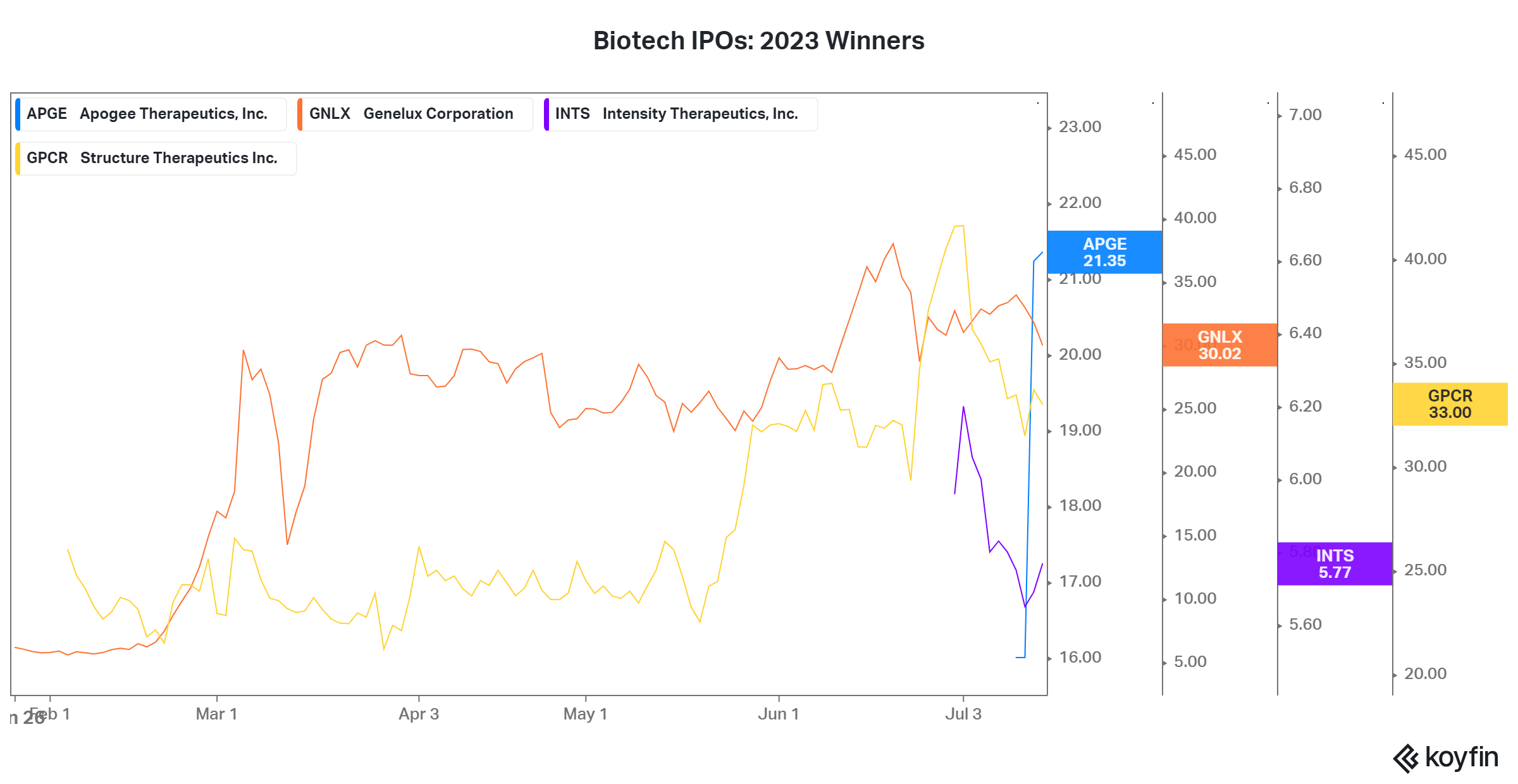

The 2023 IPO picture is improving, as 4 of 12 stocks have recorded gains from 13.8% to 430% from their offer price. All are biotechnology firms, and two winners stand apart.

Genelux Corp. (GNLX; $747M, +430%) went public on January 25 at $6.00 per share to raise gross proceeds of $15 million. Among GNLX’s therapeutic candidates is Olvi-Vec, a proprietary oncolytic vaccinia virus tailored to combat ovarian cancer. Through multiple early- and mid-phase clinical trials involving ~150 patients, Olvi-Vec has showcased positive efficacy and safety results.

Structure Therapeutics (GPCR; $1.3B, +125%) began its public life on February 2, priced at $15 per share with proceeds of $161 million. GPCR is a clinical-stage biopharma developing oral therapeutics for chronic diseases. The company’s IPO can be attributed to positive outcomes from GSBR-1290, an orally available small molecule agonist for treating type 2 diabetes and obesity.

In 2022, a total of 47 biotech IPOs raised a total of about $4 billion. That was a steep drop from 2021, when 152 offerings raised more than $25 billion, according to Reuters. This year so far resembles the 2022 pace, but two biotech IPOs completed last week suggest that 2H 2023 might cheer up a few investment bankers.

Two New Biotech IPOs

After a nearly year-long slowdown in IPO conditions for biotech, with only a handful of companies debuting on the market in 2023, two biotechs initiated trading on the Nasdaq on July 14. In fact, both companies overshot expectations, reflecting greater investor confidence.

In the second-largest biotech IPO since the start of 2022, Apogee Therapeutics (APGE; $943M) upsized and priced at the high end to raise $300 million at an $815 million market cap.

Founded by healthcare investors Fairmount Funds and Venrock as a spinout of Paragon Therapeutics, Apogee is targeting inflammatory and immunological disorders with its two leading product candidate—monoclonal antibody treatments in clinical trials:

· APG777 is targeting AD (atopic dermatitis), a chronic skin disease, and

· APG808 is targeting COPD, also known as chronic obstructive pulmonary disorder, which can lead to emphysema and death.

Apogee has plans to use part of the IPO proceeds to push lead candidate APG777 into a phase 1 trial, which it anticipates initiating in 2H 2023. The biotech is also pitching the IL-13 signaling monoclonal antibody as a potential rival to Regeneron and Sanofi’s atopic dermatitis blockbuster Dupixent.

In its second IPO attempt, Sagimet Biosciences (SGMT; $345M) priced a slightly upsized deal at the midpoint to raise $85 million at a $386 million market cap. The company is backed by NEA, Kleiner Perkins, and Baker Bros.

SGMT’s lead product candidate, denifanstat, is a once-daily pill undergoing evaluation in a Phase 2b clinical trial to treat NASH, also known as nonalcoholic steatohepatitis, or fatty liver disease. NASH is a chronic and potentially fatal liver disease for which there is currently no approved treatment in the United States and Europe. Patients with NASH face an increased risk of developing cirrhosis of the liver or liver cancer.

Sagimet has a license partnership with Ascletis Bioscience Co. Ltd. to conduct clinical trials in China to evaluate denifanstat in indications to treat moderate to severe acne and to treat recurrent glioblastoma multiforme, an aggressive type of brain cancer—in combination with an established cancer drug, a monoclonal antibody called bevacizumab.

Afterthoughts: Coping with Biotech’s Challenges

Growth-oriented self-directed investors are confronted with a massive selection of small and microcap biotech stocks. Since biotechnology is complex and especially so for generalists who lack deep knowledge in the field, it can be intimidating to sort through the scientific information and data. Still, the opportunities are real and there are simple ways to increase your probabilities for success.

Third Stream Research tracks more than 550 biotech companies with market capitalizations up to $1 billion with a median of $75 million. An alarming percentage (~40% of the smallest 200) trade below their cash value. About a dozen larger companies can be added to this group, too.

While some investors are tempted to buy assets for what they perceive to be zilch, biotechs burn through money as aggressively as any business. In most cases, the market has done the math and knows that some combination of layoffs, R&D cutbacks, panic asset sales, dilutive financings, and possibly worse, lies ahead.

Thus prospects should have sufficient capital to sustain them for a minimum of two to three years, or through an event(s) (e.g. pivotal clinical trial results, license agreement) that lifts a company’s value and increases its optionality in relation to future financings, M&A or strategic partnerships.

By definition, the smallest companies have the earliest-stage pipelines and thus the longest trajectory for cash burn. It can be a dangerous endeavor at this level.

Focusing on biotechs with robust cash positions will put you in a stronger position to profit over the long run. It’s equally critical to look into management’s experience, vision, motivations, and demonstrated ability to execute based on views or projections delivered in quarterly-call transcripts and investor presentations.

So far, all of this can be done whether or not you have a biology degree. It’s the kind of discipline that generally applies to equity research. And in the process, you will have dramatically narrowed your scope.

Third Stream’s recent data on the stock performance of the companies in our universe of coverage shows that the fifth (top) quintile is comprised, on average, with significantly higher market caps and share prices than the other four quintiles. Unsurprisingly, along with steep declines in share price performance, the market caps and stock prices descend sharply from the fourth to first quintiles.

In the sections above, the best performing IPOs (all biotechs) for 2022 and 2023 were bona fide small-caps that raised substantial amounts of capital to sufficiently advance their pipelines over the next 24 to 36 months. Alternatively, the biggest IPO losers were overwhelmingly small firms with market caps below $100 million; many with barely enough cash to last until 2024.

A useful guideline in biotech investing is to concentrate on quality companies and management that have a relatively higher degree of control over their own destiny.

See you next week.

Josh

Connect with me on Twitter and LinkedIn.

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. Joshua Levine and Third Stream Research were not compensated by any company, directly or indirectly, mentioned in Confluence, and we do not own shares in any companies mentioned.