Monthly Digest: June 2023

Sizing Up Growth Stocks / eMagin This / Watchlist Update / ‘Finfluencers’ vs. Pros

Sizing Up Growth Stocks

Investors are witnessing a striking transformation in 2023, a shift from a bearish sentiment to a tentative emergence of a new bullish era. Spearheading this resurgence are mega-cap tech stocks.

Notably, these giants have shown a newfound indifference towards the actions of the Federal Reserve, marking a departure from their previous sensitivities to interest rate fluctuations.

Around Wall Street, ‘quality’ companies are defined by their ability to generate substantial cash flow and maintain robust balance sheets. Consequently, the headline winners in the current year are Big Tech’s ‘kings of cash’.

While the much-anticipated recession has yet to materialize, the looming threat of an economic downturn coupled with the bank runs witnessed in March have bolstered the appeal of fund managers’ favorite unintelligible acronym. For purposes here, let’s call it ‘NAMTAMA’.

Even in the absence of a full-blown recession, it is widely acknowledged that slower economic growth is an inevitable reality. This inevitability has given rise to an increased attraction towards stocks that exhibit consistent growth regardless of broader economic trends.

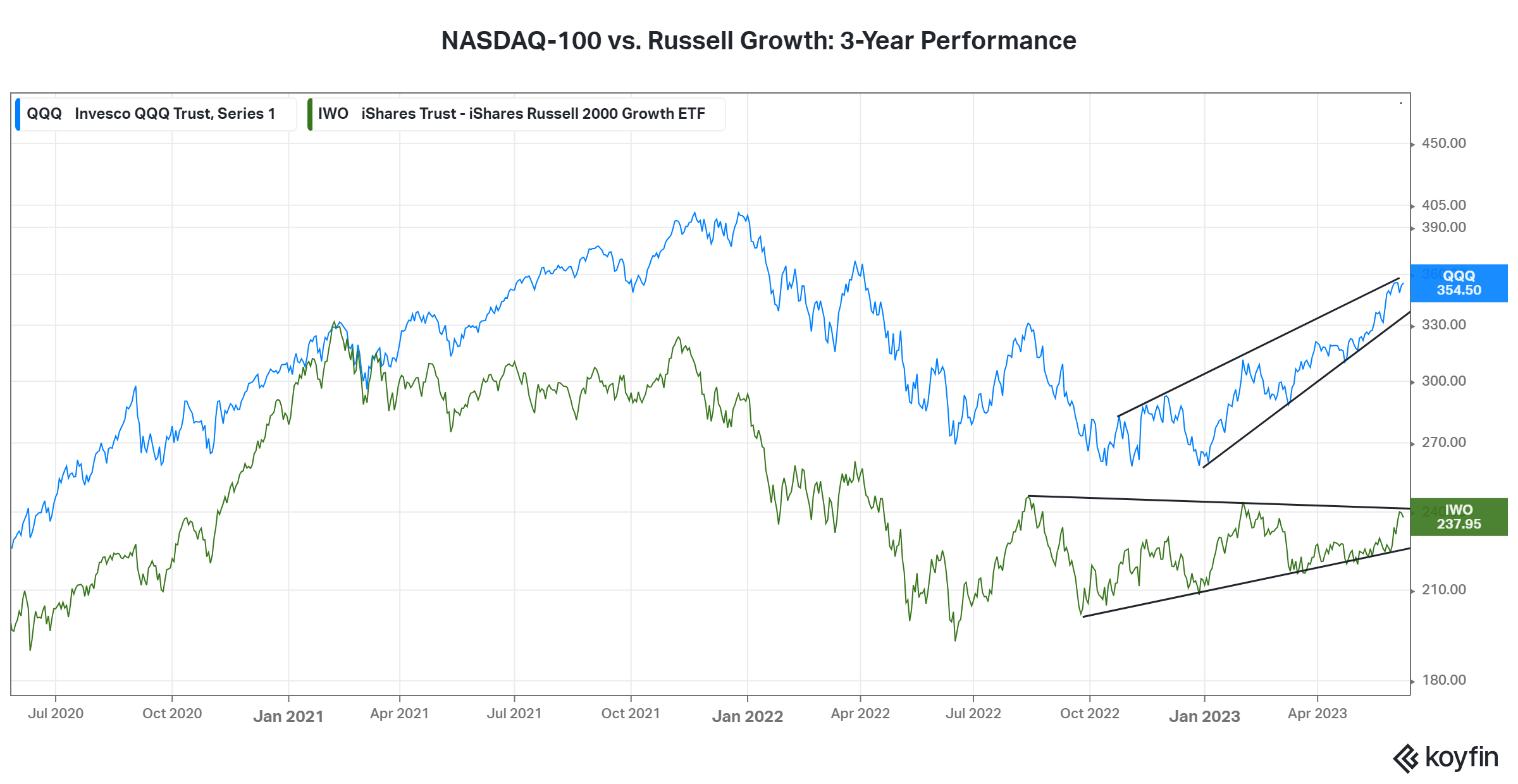

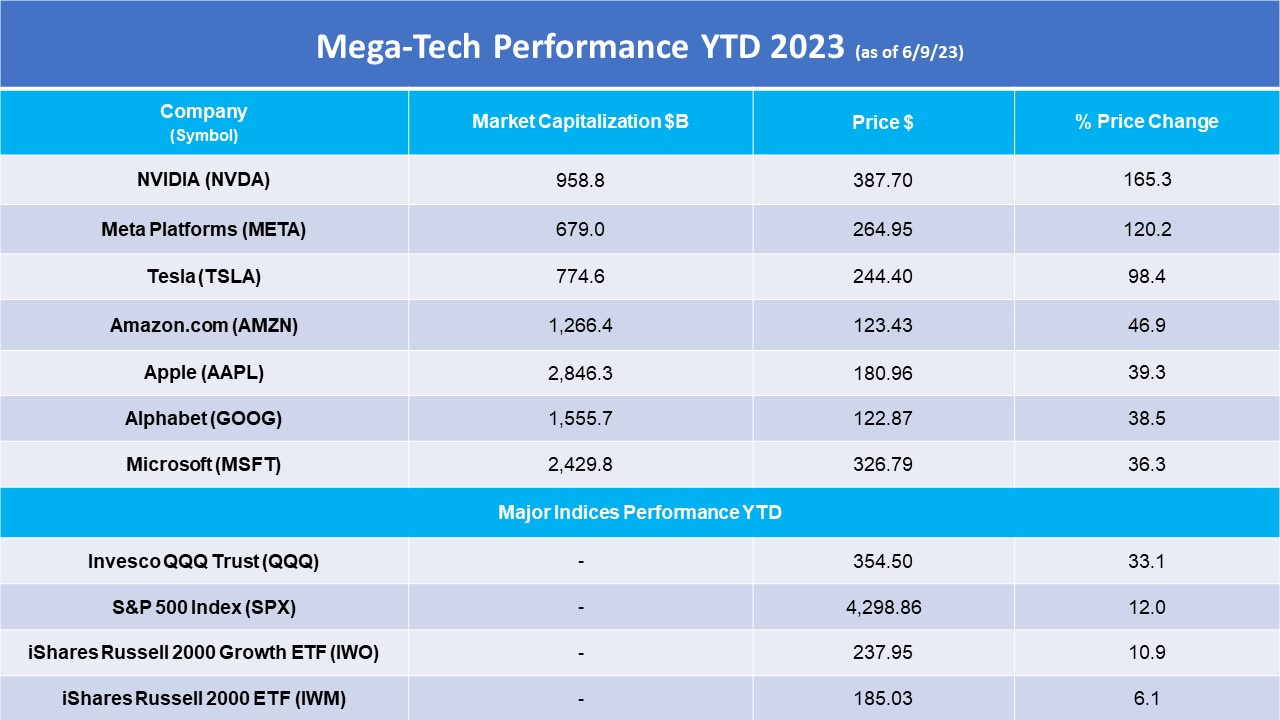

Gains in small-cap growth year-to-date severely lag the Nasdaq 100—an index overwhelmingly represented by the largest technology firms—by a 3-to-1 margin, or 33.1% to 10.9%.

We slotted the Russell 2000 Growth Index into our chart because it is a good barometer for the small-cap growth segment, with a median market capitalization of $1.1 billion. In addition, 60% of the companies operate in healthcare, industrials, and technology.

Of course, it’s no state secret that credit for much of the overall stock market’s surge goes to seven companies: NVIDIA (NVDA), Meta Platforms (META), Tesla (TLSA), Amazon.com (AMZN), Apple (AAPL), Alphabet (GOOG), and Microsoft (MSFT).

As of last Friday, the S&P 500 Index entered a technical bull market, gaining 20% off of its lows in October 2022. This is largely due to the stunning performances of the Big 7 (or ‘NAMTAMA’), which account for more than one-quarter (25.4%) of weightings in that benchmark.

To start the year, small-cap growth had kept pace with Nasdaq 100 into February before trending sideways over subsequent months; meanwhile, mega-tech stocks continued their impressive climb. Whether the emerging growth stocks will follow suit is dependent on a panoply of factors, but most of all it is the animal spirits of investors, and they remain tepid based on data in our universe of coverage, a majority of which are nano- and micro-cap companies.

Third Stream Research tracks 1,200+ companies with market capitalizations below $1 billion, covering the TMT, Biotechnology, Healthcare/Life Science, Medical Devices, and Cleantech industries. The average YTD gain of all 1,237 stocks is 6.4%, which trails the Russell Growth Index by 4.5 percentage points. However, when we exclude all companies below the $10 million market-cap threshold and trading under $1 per share, the performance is strikingly improved: +15.2%, with winners outpacing losers by a 475 to 371 margin.

We’ll be taking an in-depth look at their performance and the most impactful trends in our Mid-Year 2023 Digest in July.

eMagin This

Early-stage companies jumping into the public markets at their first opportunity is central to the history of emerging growth stocks. The first massive wave occurred in the early to mid 1980s, following the IPOs of Apple (AAPL) and Genentech (now part of Roche), which lit the passions of Wall Street and retail investors.

This typically happens when investment bankers or other types of financiers come along with offers that can’t be refused. For companies unable to tap into the venture capital circuit, or uninterested, it’s an appealing chance to raise a nice chunk of cash, gain status, and broaden investor visibility. Details to be worked out later.

Unfortunately, many of these fledgling companies evolve into virtual zombies, committed to meeting the demands of remaining public but in effect operating as private firms. Others, such as eMagin Corp. (EMAN; $165M), stay in the fight for years without realizing their promise for long term stakeholders.

Now, eMagin has agreed to be acquired by Samsung Electronics’ display subsidiary for $218 million in cash, or $2.08 per share—placing a tiny exclamation mark on its 24-year life as a publicly-traded company.

The purchase price represents a premium of ~10% to eMagin’s closing stock price of $1.89 on May 16, 2023, and a premium of ~24% to eMagin’s six-month volume-weighted average price of $1.68.

Founded in 1999, eMagin was named the winner of 2000 SID Information Display Magazine Display of the Year Gold Award, for its achievements in organic light emitting diode (OLED) microdisplay technology, referred to as OLED-on-silicon.

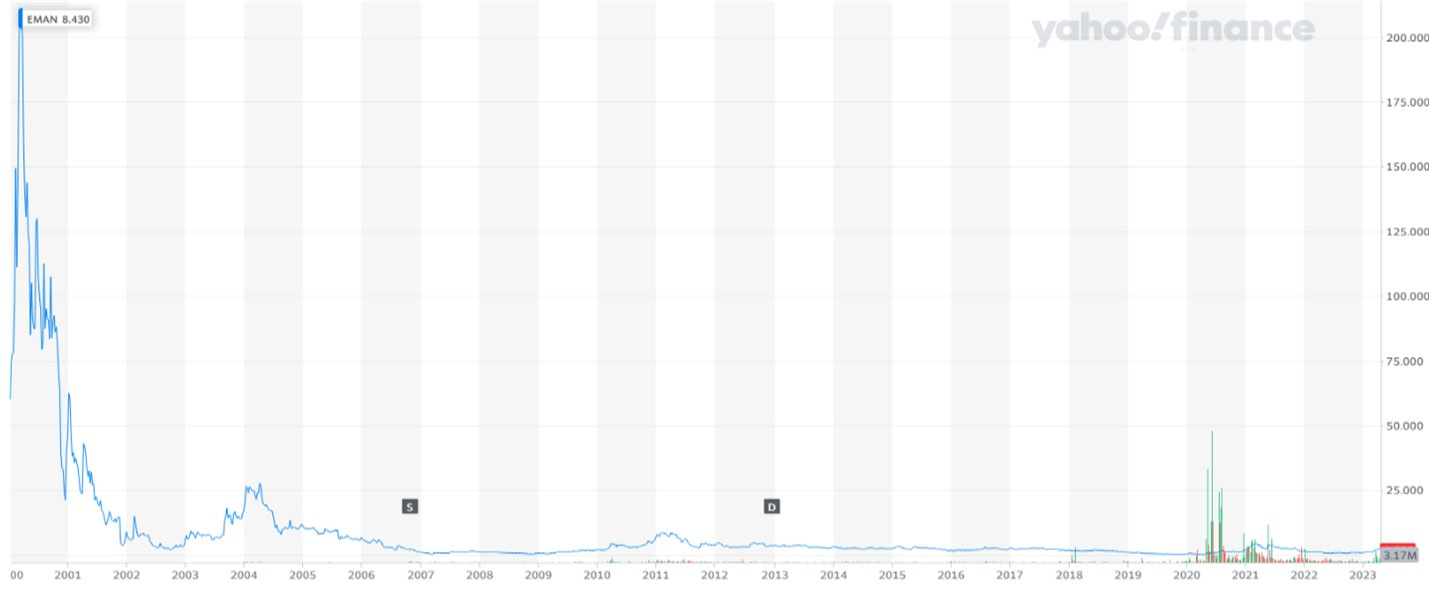

On March 22, 2000, only days after the Tech Bubble had reached its apex, eMagin’s management seized an opportunity to obtain a public listing.

eMagin chose to bypass the traditional IPO route. Instead, the company merged with with a publicly traded shell company called Fashion Dynamics Inc. to reach the public market. Coincident with the merger, the company raised $27 million in a private placement led by Citigroup and Verus International Ltd.

“It saved several months of time in getting stock out there in public market,” said eMagin’s CEO at the time, explaining his market-entry strategy. “This was really the right time to be in the public market for our sector.”

For a brief and shining moment, it was. Then, eMagin’s share price tumbled below its opening day price and continued downward. Except for some modest gains in 2003-04, the stock has flatlined ever since, as seen in the chart below.

eMagin, based in upstate New York, stuck to its competencies all these years and today develops, designs, and manufactures Active-Matrix OLED microdisplays for high-resolution, AR/VR and other near-eye imaging products.

eMagin’s latest tiny 2K display is set to be in production next year.

Source: eMagin

EMAN’s annual revenues first topped $20 million in 2009 but never exceeded more than $30.5 million, which it attained in 2010 and again in 2022. eMagin lost money in every year but two—2010 and 2011, netting $5.0 million and $2.3 million, respectively—leading to an accumulated deficit of $261 million as of its latest quarter. It’s notable that since 2017, outstanding shares have jumped 130% to 78 million.

Today, EMAN is covered by two analysts, while institutions own merely 9.5%.

Samsung’s acquisition of eMagin is expected to close in the second half of 2023, subject to the approval by eMagin’s stockholders, applicable regulatory approvals and other customary closing conditions.

Third Stream Research - Watchlist Updates: ORGS, PRPH

Orgenesis (ORGS; $38M) is partnering with the University of California system to deploy its Orgenesis Mobile Processing Units and Labs (OMPULs) in medical and academic institutions.

This collaboration aims to decentralize the development and manufacturing of cell and gene therapies, showcasing the advantages of ORG's innovative OMPUL design for the healthcare market.

The phased rollout of OMPULs will begin at UC Davis, where the first unit will be established and validated. Subsequently, OMPULs will be deployed at various healthcare facilities in California. This initiative will facilitate on-site production for clinical trials, particularly for the advancement of cell and gene therapies at UC Davis Health's Alpha Stem Cell Clinic.

Morgenesis LLC, a subsidiary of Orgenesis' POCare service, will handle the installation and operation of OMPULs in the United States and internationally. UC Davis Health has been an active participant in the Orgenesis POCare Network since 2020, leveraging the POCare Service Platform to develop and supply cell and gene therapies at the point of care, benefiting patients in need.

This collaboration follows a recent $8 million grant renewal from the California Institute for Regenerative Medicine to UC Davis Health's Alpha Stem Cell Clinic. The grant supports the expansion of the clinic's clinical trials program and contributes to advancing on-site manufacturing of advanced therapies.

We introduced ORGS in Perspectives: Orgenesis: Nano-captivating prospect is industrializing cell and gene therapies on May 10.

ProPhase Lab’s (PRPH; $127M) Linebacker-1 (LB-1), a multi-kinase inhibitor developed by its biopharma subsidiary, has shown promising results in inhibiting cancer cell growth, according to studies conducted at Harvard's Dana Farber Cancer Institute.

In lung and colon cancer models, Linebacker demonstrated the ability to halt cancer cell proliferation. Lung cancer cells treated with Linebacker monotherapy showed no cell proliferation, suggesting its potential as a stand-alone therapy. In the colon cancer model, Linebacker displayed synergistic effects when combined with low doses of chemotherapy drug Doxorubicin.

The positive preliminary results have bolstered ProPhase's confidence in the therapy's potential. PRPH plans to conduct in-depth cancer modeling to refine its clinical pathways. The company is collaborating with experts from prestigious institutions, including the Dana Farber Cancer Institute, Baylor College of Medicine, Reprocell, and Charles River Laboratories.

Phase I human studies, with a budget of ~$3+ million, are expected to take place next year. ProPhase aims to position itself for licensing opportunities with major pharmaceutical companies upon obtaining positive results and necessary regulatory approvals.

The Linebacker compound, derived from the plant flavonoid Myricetin, is a modified polyphenol. Myricetin exhibits various beneficial activities, including antioxidant, anti-cancer, anti-diabetic, and anti-inflammatory effects. Linebacker's specific forms, LB-1 and LB-2, have chlorine atom substitutions at key positions.

These developments support ProPhase's diversification strategy, positioning PRPH as a multi-dimensional pharmaceutical enterprise with promising business lines in biotech, genomics, and diagnostics.

Third Stream Research provides independent coverage on PRPH, with a Strong Buy rating. You can read our Initial Report and Updates here.

‘Finfluencers’ vs. Fund Managers

A recent study published by the Swiss Finance Institute looks at the phenomenon of ‘Finfluencers’–-individuals on social media platforms who offer financial advice based on "Tweet-level data." The paper examines the performance and influence of these Finfluencers and raises important questions about the efficacy of their recommendations.

Additionally, it highlights the impact these influencers can have on retail trading behavior and market efficiency. While it is tempting to solely blame the Finfluencers for their shortcomings, let’s recognize that skilled professionals also struggle to outperform benchmarks with any consistency.

Finfluencer performance and influence

According to the Swiss Finance Institute's research, a significant proportion of Finfluencers demonstrate varying levels of skill in generating abnormal returns. Out of the sampled Finfluencers, 28% were identified as skilled, generating monthly abnormal returns of 2.6%. Conversely, 16% were deemed unskilled, while a majority of 56% exhibited negative skill, with monthly abnormal returns of -2.3%.

Surprisingly, the researchers discovered that it is the anti-skilled Finfluencers who amass more followers and wield greater influence over retail trading compared to their skilled counterparts.

The advice disseminated by these anti-skilled Finfluencers tends to foster overly optimistic beliefs among their followers, leading to persistent biases and exaggerated market swings. Consequently, the prevalence of Finfluencer advice contributes to excessive trading and inefficient prices, ultimately undermining market performance. For what it’s worth, the researchers propose a contrarian strategy that shows promise, yielding a monthly out-of-sample performance of 1.2%.

Alpha-deficient skilled professionals

While the study's focus centers on the influence of Finfluencers, it should be pointed out that seasoned professionals struggle to consistently outperform market benchmarks.

A 2022 study conducted by S&P Dow Jones Indices on actively managed mutual funds in the U.S. stock and bond markets over five years revealed a lackluster performance record. None of the 2,132 analyzed mutual funds managed to beat their respective benchmarks on a regular and convincing basis.

This finding underscores the difficulties faced by investment professionals in delivering consistent alpha. It raises questions about the effectiveness of traditional investment strategies and the ability of professional money managers to generate superior returns over time.

Together, both studies highlight the need for investors to carefully evaluate any source of financial advice and exercise caution, whether relying on Finfluencers or professionals.

See you next week, and thank you for your support.

Josh

Connect with me on Twitter and LinkedIn.

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. Joshua Levine and Third Stream Research were not compensated by any company, directly or indirectly, mentioned in Confluence, and we do not own shares in any companies mentioned.