Submerging Growth in 2022

Submerging Growth in 2022

Due diligence set for comeback in the new year.

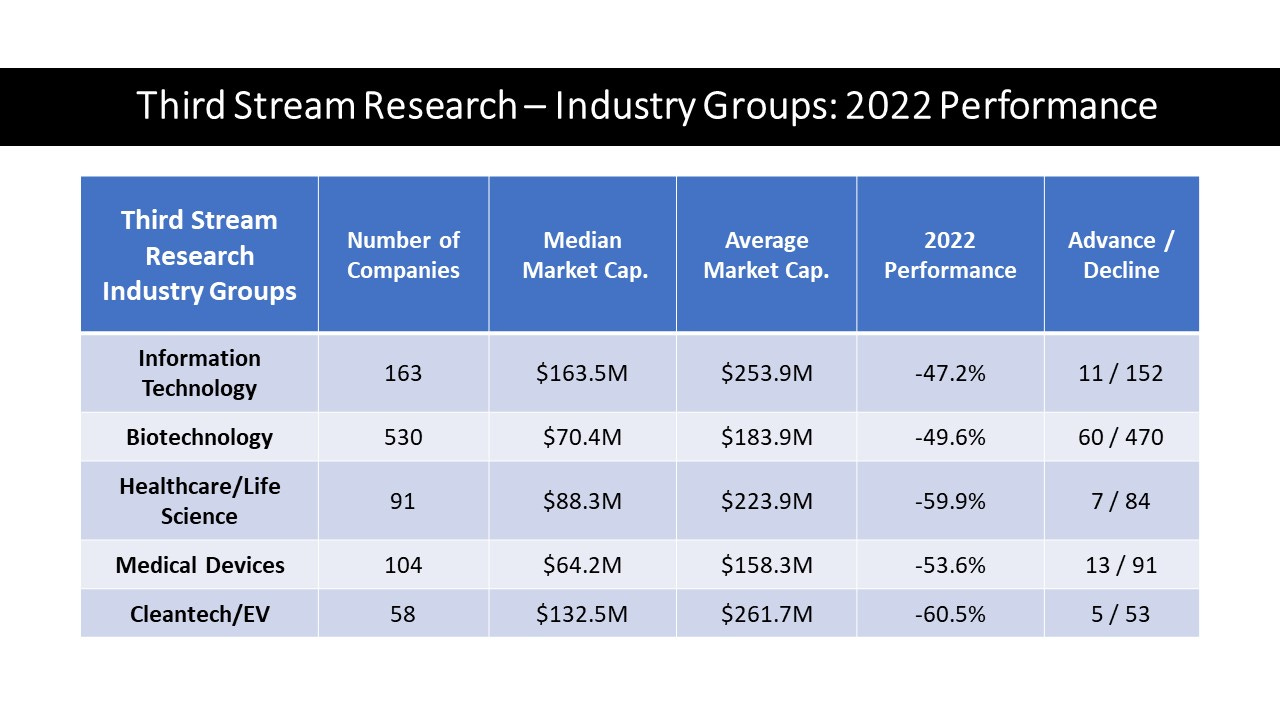

Today we introduce Third Stream Research’s Industry Groups, comprised of Information Technology, Biotechnology, Healthcare/Life Science, Medical Devices, and Cleantech/EV. An essential part of Confluence in 2023 features weekly data, analysis and coverage of the emerging growth universe of technology-intensive companies (<$1 billion market cap).

In a year in which most large technology stocks dropped between 20% to 70%, their smallest brethren were also hit with a steep revaluation. According to Third Stream Research, the 946 North-American based small- and micro-cap companies that we track across leading high-growth industries had an average loss of -52.1% in 2022. By another measure, losers outpaced winners by more than an 8-to-1 margin, 850 to 96.

The table below illustrates some variation in the distribution of the damage, with the Information Technology companies holding up best (-47.2%), followed by Biotechnology (-49.6%) and Medical Devices (-53.6%). Cleantech/EV (-60.5%) and Healthcare/Life Science (-59.9%) suffered the biggest losses.

Among the 946 companies tracked, we found that the stocks with market caps below $150 million performed dramatically worse than those with larger valuations. Additionally, the vast majority of cash-strapped companies were below the $100 million threshold and included an overwhelming number of the biggest decliners.

Cash is the lifeline for the overwhelming number of emerging growth companies, particularly in biotech where quarterly burn rates are monitored closely like EKG readings for cardiac patients. Under current stock market conditions, weighed down by interest rates, inflation and a looming recession, the most financially strained businesses face existential consequences. Management and boards will have little choice but to engage in the kind of massively dilutive financings that frequently bury stocks. Separately, mergers and acquisitions will present attractive exits for very few.

We don’t recommend that investors take shortcuts in due diligence on emerging growth companies. But a useful starting point — and one that will help to protect against severe losses — is to ask how long a business can operate with its current capital, and what is the anticipated cost of any future capital raise?

In this context, let’s take a look at some interesting findings uncovered within each industry group:

Information Technology

Nearly one-third (52 of 163) were down 75% or more.

7 stocks gained at least 20%.

More than one-quarter (28%) have cash positions below $10 million.

Biotechnology

One-third (176 of 530) were down at least 75%; one-in-eight fell by at least 90%.

Shares of 15 companies doubled or better, with gains ranging from 103% to 211%.

201 (38%) are valued for less than the amount of cash they have in the bank.

One-in-five (109) companies have cash positions below $15 million.

Healthcare/Life Science

More than 2-in-5 companies (38 of 91) dropped 75% or greater.

4 companies gained 30% or better.

16 companies have cash positions exceeding market cap.

Medical Devices

39 of 104 (38%) suffered a loss of more than 75%.

9 companies produced double-digit gains.

Nearly one-in-five (19) companies have market caps below cash level.

Cleantech/EV

25 of 58 (43%) were down at least 75%.

Only 2 companies generated double-digit gains.

22 have cash positions below $15 million.

10 companies are valued below their cash position.

Naturally, due diligence on smaller tech-driven companies requires far deeper investigation than a cursory glance at financials. Yet a basic understanding of a company’s liquidity and long-term viability is a fast and effective way to filter out weak players.

Maybe a better strategy is one that begins at the other end of the list, by identifying companies with strong financials and the means to invest in growth projects in a difficult business climate. There’s usually a good reason why they got in that position in the first place.

We recommend that you stay tuned to this publication because upcoming issues of Confluence will take deeper dives into each of the industry groups, assessing the outlook for winners and losers, and exploring the economic and market forces influencing their direction.

Was Emerging Tech a Leading Indicator for Downturn?

2020 and 2021 were impressive years for tech stocks. From the March 2020 low through November 15, 2021, the Nasdaq 100 surged 137%. However, since its peak the benchmark index has slumped nearly 35%

The era of free money ended last year when the Federal Reserve’s aggressive interest-rate increases shifted the momentum. Investors no longer could rationalize the merits of holding the shares of tech firms whose appeal centered on their potential for generating windfall profits many years in the future.

It’s notable that the Nasdaq Composite’s 33% slide in 2022 marks its steepest decline since 2008 and the third-worst year on record; the drop 14 years ago came during the financial meltdown caused by the housing crisis. The tech-heavy Nasdaq fell 1% in the fourth quarter, wrapping up its first four-quarter losing streak since 2000-2001.

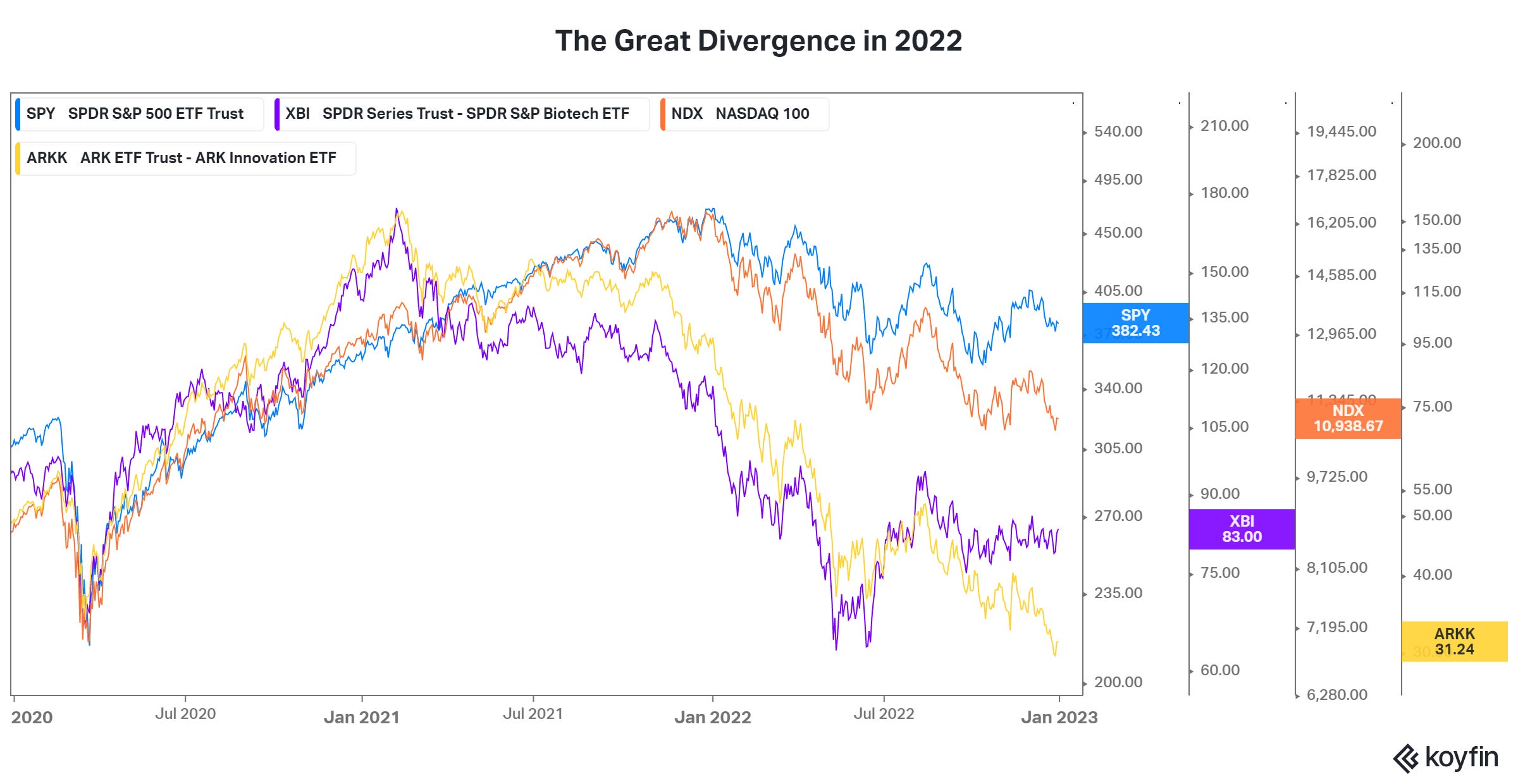

Importantly, for the small- and micro-cap companies tracked by Third Stream Research, peak levels occurred one year earlier than the large tech stocks, and the subsequent drop was far more punishing. This fact is rarely mentioned in market commentaries, which tend to lump tech stocks of all shapes and sizes together.

As the chart below indicates, two proxies for emerging growth stocks — the SPDR S&P Biotech ETF (IBB) and the ARK Innovation ETF (ARKK) — peaked in January 2021 (whereas big tech reached highs in January 2022) and ultimately plummeted in the first half of 2022, ending the year with losses of -15.4% and -68.5%, respectively.

Let’s remember, too, that the IPO market in 2022 left considerable wreckage in its wake. IPO deal proceeds nosedived 94% in 2022 — from $155.8 billion to $8.6 billion — according to Ernst & Young’s IPO report published in mid-December. Not a single tech deal raised $1 billion last year, after 15 IPOs raised at least that much in 2021.

Many of the companies that did manage to go public last year — a large percentage of them represented in Third Stream Research’s industry groups — lost 80% or more of their value. New issues were priced at astronomical valuations that could not be justified in any market environment, let alone the one we experienced in 2022.

For companies still in the IPO pipeline, the challenge isn’t simply overcoming a bear market and volatility. They also need to face the reality that the valuations granted by venture capitalists and other private investors such as private equity and hedge funds don’t reflect the changes in the economic environment or public market sentiment.

See you next week, and thank you for your support.

Josh

Connect with me on Twitter and LinkedIn.

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. I do not own shares of companies mentioned.