Skin is the Game

Dermatology sector has long produced attractive M&A candidates, but do alluring prospects still exist for growth investors?

Dermatology is a resilient and thriving market for mergers and acquisitions, demonstrating its ability to weather changing tides. Amidst a dynamic deal landscape, we question if compelling opportunities remain for investors who scour lesser known companies in this lucrative field.

The rising prevalence of skin diseases, coupled with increasing demand for dermatological products, serves as a catalyst for ongoing investment. Funding for pharmaceutical advancements and heightened R&D activities have further propelled healthy revenue growth over the long term.

Dermatology's competitive landscape is fragmented, with numerous mid-size and smaller companies vying for market share in prescription and over-the-counter sectors. Competitors focus on developing or acquiring pharmaceuticals, medical devices, and OTC products targeting the same dermatological diseases and conditions.

Strategic factors include quality, efficacy, market acceptance, pricing, and marketing efforts. Adaptation to regional nuances is essential, as competitive dynamics vary across geographic areas. Success lies in differentiation, customer-centricity, and navigating the multifaceted market with agility.

In 2021 the dermatology M&A market saw 13 transactions, according to DealForma, with a combined value of $600 million. This reflects an active but relatively modest landscape. However, the subsequent year witnessed a shift in the number of deals, decreasing to 7, while the total M&A value significantly rose to an impressive $2.1 billion.

Although deal volume for Q1-2023 remained low, a single dermatologic deal stood out, amounting to a substantial $800 million. This reinforces the notion that investors remain confident in the sector’s long-term prospects.

Compared to other therapy areas in the biopharma industry, dermatology M&A is the fourth largest in terms of deal count since 2018, reports DealForma. With 58 deals, the sector amassed a total M&A value of $84.6 billion. In contrast, the cancer therapy field dominated M&A activity, with a staggering 291 deals and a cash value of $265.1 billion, reflecting huge investor confidence.

Notable recent deals in the dermatology sector include Sun Pharmaceutical Industries' (India) acquisition of Concert Pharmaceuticals for $576 million. This strategic move grants Sun Pharma access to a promising experimental hair loss drug, anticipated for U.S. approval in the near future.

Another Indian pharma Eris Lifesciences Ltd acquired a selection of dermatology brands from Glenmark Pharmaceuticals for 3.4 billion rupees ($41.6 million). This targeted acquisition aims to bolster Eris’ position in the anti-fungal and anti-psoriasis segments within the Indian and Nepalese markets.

Despite occasional fluctuations, the dermatologic M&A market has demonstrated resilience, fostering a stable environment for long-term growth. Additionally, smaller deals typically present niche opportunities that are overshadowed by larger transactions, but nevertheless have led to market-beating returns for investors.

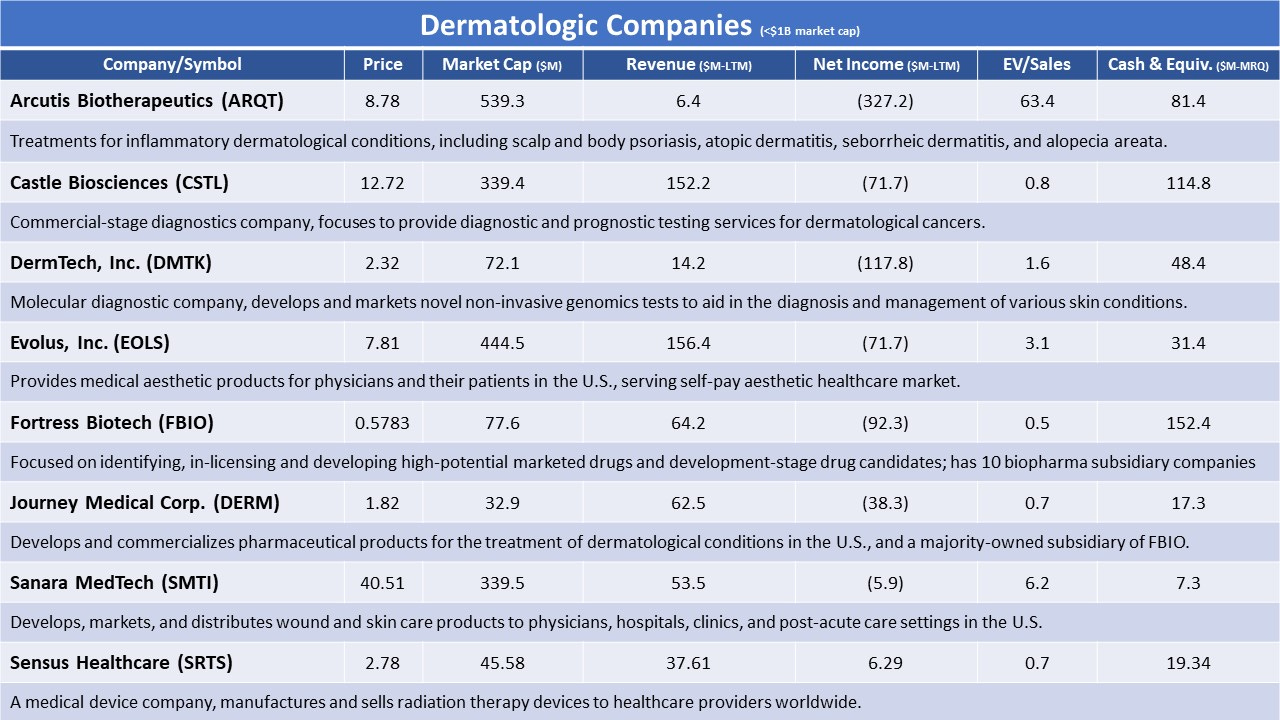

Dermatologic Companies

To successfully compete for business, smaller companies need to show that their products offer medical benefits, but also cost advantages versus other forms of care. Accordingly, they face pressure to continually seek out technological innovations and to creatively market their products.

The eight US-based dermatologic companies in the table below have market capitalizations from $30 million to $540 million. As a group, they trailed the benchmark Russell 2000 Growth Index by a wide margin year-to-date (-13.7% vs. +9.0%) and year-over-year (-21.7% vs +12.9%).

These companies are representative of the diversity of the science, technology, and products across the dermatologic landscape. Each one has a track record of revenues, but 4 of the 8 stocks on this list are sporting an EV/Sales ratio below 1.0x, and only one, Sensus Healthcare (SRTS), reported a profit over the last 12 months.

Additional dermatologic companies to note are: Biofrontera Inc. (BFRI), Dermata Therapeutics (DRMA), Novan Inc. (NOVN), STRATA Skin Sciences (SSKN), and Sonoma Pharmaceuticals (SNOA). All have sub $35 million market caps, and 4 of the 5 are trading near or below cash value.

Many leading prospects in this area were taken out of the market through mergers and acquisitions over the past 15 years. Today, the small and microcap firms are less desirable targets due to excessive debt load, bleeding cash flow, and underperforming sales growth. However, we do think there’s one company worth a serious look.

Sanara MedTech (SMTI) outshines peers with 10 consecutive years of revenue growth (+100% year-over-year in 2022); shares +107% in past year.

Sanara MedTech is experiencing impressive triple-digit annualized growth in its top line. The company's expansion into new territories and ability to secure additional contract wins are driving this stellar performance.

In Q1 2023, Sanara generated $15.5 million in net revenue, marking a 99% increase compared to the same period last year. The quarter was a record-breaking one for the company, with March achieving the highest sales month in its history. Although Sanara reported a net loss of $1.2 million, it represents a significant improvement compared to the net loss of $3.2 million in the previous year's period.

Sanara's extensive distribution network serves as evidence of its successful market share capture, with the company experiencing substantial uptake in hospitals and other facilities where its products are sold. Impressive over-year revenue growth compounding on a quarterly basis indicates that the market eagerly embraces Sanara's offerings.

The company's surgical sales team has been instrumental in driving growth by penetrating deeper into the existing customer base and expanding into new geographic areas. As of March 31, 2023, Sanara's products were sold in over 800 hospitals and ambulatory surgery centers across 30 states, with contracts or approvals secured for sale in over 1,800 facilities.

Sanara MedTech specializes in providing surgical, wound, and skincare products for use in hospitals, clinics, and post-acute care settings. Operating primarily in the advanced wound care and surgical tissue repair markets in North America, its product portfolio includes CellerateRX Surgical Activated Collagen, FORTIFY TRG Tissue Repair Graft, FORTIFY FLOWABLE Extracellular Matrix, as well as advanced bone matrix biologics, which promote bone growth, stimulates the body's natural healing response and encourages the growth of new bone tissue.

Notably, SMTI insiders—primarily two board members—own a majority of the shares in the company, while institutions hold less than 5%. Additionally, with only 8.4 million shares outstanding and a float of 3.2 million shares, this tightly held stock could be potentially explosive should it continue delivering strong operating results into next year.

Overall, Sanara MedTech's impressive revenue growth, expanding market presence, and strategic product offerings indicates SMTI is a formidable competitor in the advanced wound care and surgical tissue repair sectors. Consequently, we’re adding SMTI to Third Stream Research’s Watch List.

See you next week, and thank you for your support.

Josh

Connect with me on Twitter and LinkedIn.

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. Joshua Levine and Third Stream Research were not compensated by any company, directly or indirectly, mentioned in Confluence, and we do not own shares in any companies mentioned.