Serving the Global Economy

Data center and digital infrastructure companies anchor growth in data and AI

The nervous system of the world’s information economy runs on server farms inside data centers. For most businesses however, the cost of maintaining an on-premise data center is prohibitive due to constant product development and upgrades, maintenance of the physical infrastructure and upkeep of mission-critical security protocols and technology. This is the opportunity captured by the big data-center operators, who have the intellectual and financial capital to rapidly scale and extend service offerings.

Data centers are essential for hosting and managing large volumes of data and computing power. They are typically owned and operated by cloud vendors, banks or telcos for their own specific needs. Alternatively, co-location companies provide the space, network capacity, power, and cooling equipment necessary for other businesses to bring in their own IT equipment.

The most powerful companies in the world—Amazon Web Services (AWS), Alphabet (Google Cloud) and Microsoft Azure—dominate the industry as ‘hyperscalers’ or cloud providers that operate data environments at a massive scale. This trio controls a 65% share of the world cloud market between them.

Amazon's cloud-computing division is the industry leader based on revenue. In recent months, AWS saw its sales growth slow as wary businesses scrutinized their cloud bills. While such ‘cost optimization’ continues to be a factor, large companies are embracing the cloud anew—thanks in part to the surge of interest in AI—helping to stabilize AWS growth.

AWS beat Wall Street estimates of around $21.7 billion in Q2 cloud sales, increasing them 12% to $22.1 billion. Its rivals posted bigger jumps off smaller bases: 28% growth in Alphabet's June-quarter cloud revenue and a 26% quarterly increase for Microsoft's Azure.

Explosive demand for data centers is also attracting investors of all types, including growth capital, buyout, real estate and infrastructure investors. They are attracted to the steady, utility-like cash flows and risk-adjusted yields, according to McKinsey & Company :

In 2021, data center transactions numbered 209, accruing an aggregate value exceeding $48 billion, marking an impressive 40% uptick from the preceding year.

The first half of 2022 witnessed 87 deals, collectively valued at $24 billion.

Private equity acquirers solidified their position, contributing to 42% of deal value between 2015 and 2018. Their prominence escalated to 65% between 2019 and 2021, skyrocketing beyond 90% during the initial half of 2022.

In the United States alone, the appetite for data centers—quantified by power consumption as a proxy for server capacity—is projected to surge to 35 gigawatts by 2030, more than doubling 2022's 17 gigawatts, as per McKinsey's insights. The US commands nearly 40% of the global data center market share.

The resources quandary and the path to sustainability

Data centers are one of the most energy-intensive building types, consuming 10 to 50 times the energy per floor space of a typical commercial office building, according to the U.S. Department of Energy.

Because water is the most common method for cooling data centers, it also makes them heavy water users. Researchers at Virginia Tech found that, in just one day, the average data center could use 300,000 gallons of water, or about the same consumption as 100,000 homes.

As the world’s use of information technology grows, both data center growth and energy and water usage is expected to increase. For this reason, sustainability is an urgent matter for operators and their customers.

Indeed, Microsoft has a sustainability goal to replenish more water than it uses in its data centers by 2030. The company also provides an example of the potential to increase use of fossil-fuel alternatives and preserve natural resources. Microsoft intends to shift 100% of its energy use to renewable energy sources by 2025, and by 2030, have all of its energy use matched by zero-carbon energy purchases.

The effects of climate change globally will compound the need for transformational solutions in the years to come.

40 Leading Operators and Suppliers in Data Centers & Digital Infrastructure

As massive, non-descript structures resembling distribution warehouses, data centers house thousands of interconnected computer servers and the equipment to keep them running. The space occupied by an average data center is estimated to be 100,000 square feet, while the world’s largest, located in China, spans 6.3 million square feet of space—equal to 110 football fields. Interestingly, only about 50 employees are posted in a typical data center.

Data center facilities incorporate routers, switches, firewalls, storage systems, servers, and application delivery controllers. Because these components store and manage business-critical data and applications, security is a vital part of data center design.

The following owners, operators, suppliers and partners of data centers represent a diverse selection across technology and adjacent industries. (Market cap and revenues in millions).

Data centers are an essential part of the businesses for these companies, which represent more than one-third of the weighting in the Nasdaq-100. Now, let’s focus on the two smallest members of this list.

Two Small-Cap Companies in Data-Center Space: Applied Optoelectronics and Rackspace Technology

Among the 40 active companies in the business of data centers and digital infrastructure, only two small-cap targets emerge: Applied Optoelectronics and Rackspace Technology.

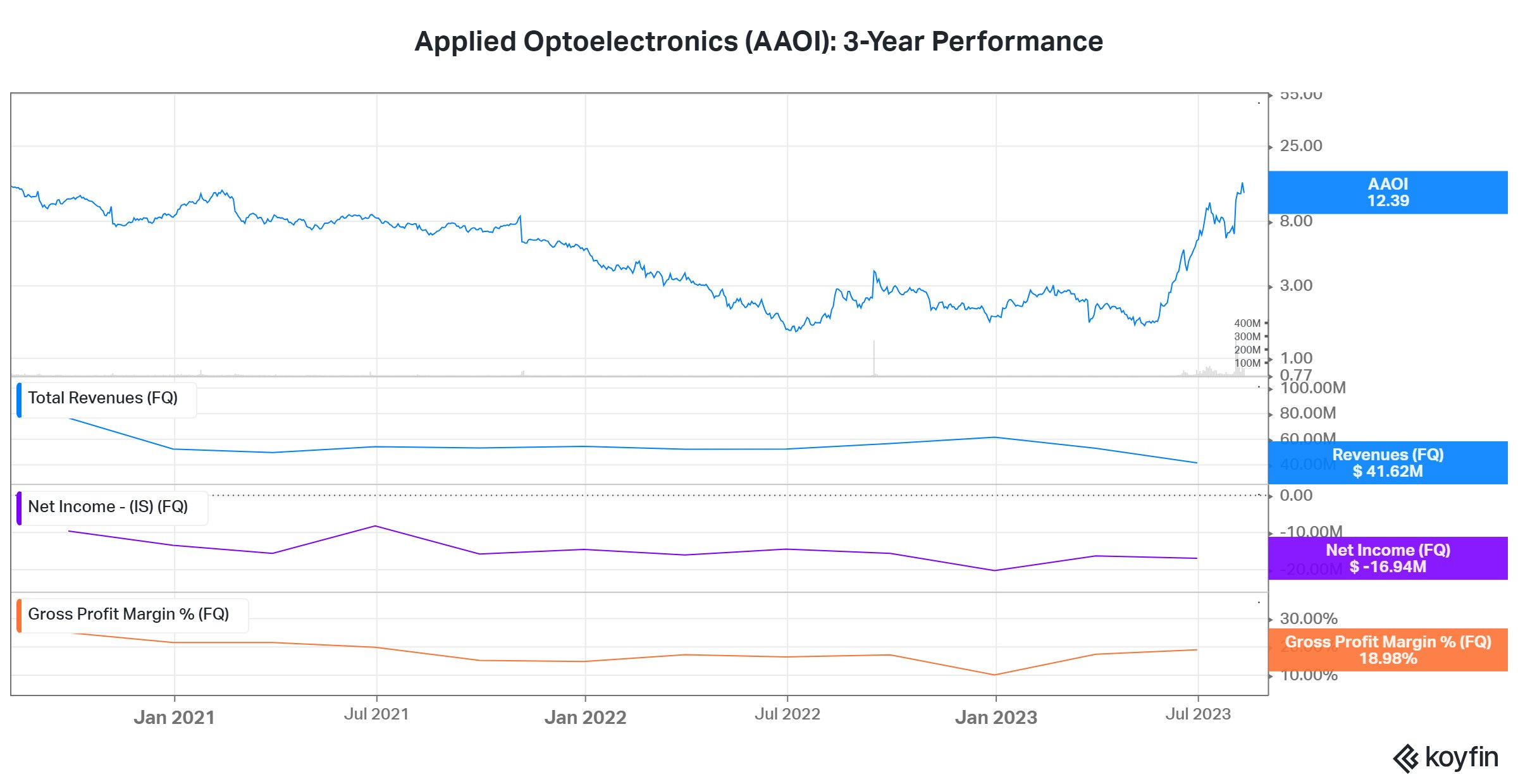

Applied Optoelectronics (AAOI; $398M)

AAOI manufactures fiber-optic networking products, offering optical modules, lasers, subassemblies, transmitters and transceivers and other equipment that it sells to internet data center operators, cable television and telecom equipment manufacturers, and internet service providers.

Within the internet data center market, Applied Optoelectronics benefits from the increasing use of higher-capacity optical networking technology as a replacement for copper cables, particularly as speeds reach 400 billion bits per second (Gbps) and above, as well as the movement to open internet data center architectures and the increasing use of in-house equipment design among leading internet companies.

AAOI’s 10-Q filing for Q2 2023 indicates that its data center business represents two-thirds (66%) of revenue, up from 41% for the same period one year earlier.

A big positive for Applied Optoelectronics is the strong demand being driven by AI applications, particularly for Microsoft, its biggest data center customer. AAOI’s CEO reported in the recent quarterly earnings call that Microsoft is adding a lot of optical modules and interconnect modules:

“If you kind of look at some of the forecasts that we've received from them, the minimum contractual levels of manufacturing that they've asked us to prepare would imply revenue of $300 million plus over the next few years just in those products.”

Second quarter revenue for AAOI’s datacenter business was $27.6 million, up 28% year-over-year and up 35% sequentially large due to increased demand for its 100G and 400G transceivers, which are networking components used for high-speed data transmission.

AAOI shares surged 40% on August 4 after B. Riley Securities upgraded the stock to Buy from Neutral based on improving demand and margins, following the company's Q2 results on August 3, when it closed at $6.39. B. Riley also took a sharp U-turn on its price projection, raising its target to $11.50 from $2.50.

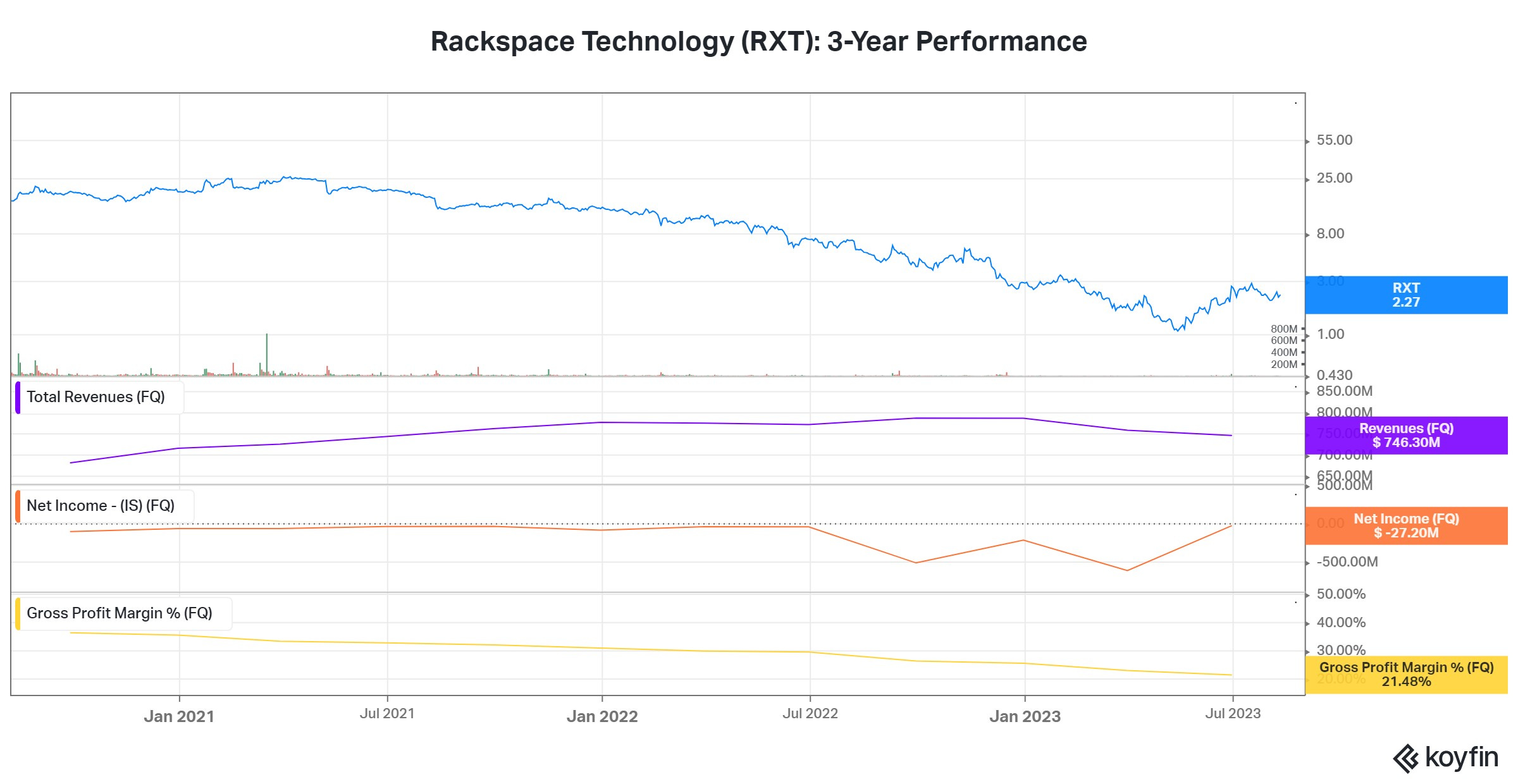

Rackspace Technology (RXT; $491M)

RXT operates as a multi cloud technology services company worldwide through its new operating model—Public Cloud and Private Cloud segments—and has recently hired several industry veterans into management roles.

RXT shares rose 74% in June 2023 after turning its focus on the explosive AI market and signing a long-term generative AI partnership with Google Cloud. The deal gives Rackspace customers access to Google Cloud's growing portfolio of generative AI tools, and the two companies will cross-promote this technology hub.

For Q2 2023, RXT reported revenue of $746 million, down 3% year-over-year; while public cloud revenue grew 3% to $435 million and private cloud revenue was $311 million, down 11%. For the current quarter, Rackspace provided the following guidance: total revenue $722-$732 million, public cloud revenue $428-$433 million, and private cloud revenue $294-$299 million—all sequentially lower.

In late July, Citi Research downgraded the shares of the cloud tech services provider to Sell/High Risk from Neutral/High Risk, but raised its target price on RXT to $1.50 from $1.25. Citi analysts noted that Rackspace's sustained investments in technology, service levels, ecosystem partnerships and sales helped it in the growing multi-cloud end market.

Still, certain factors weigh on the Rackspace. Its revenue mix is lower-margin, the company’s larger focus on profitability has hurt growth and growth prospects, and cash flow initially improved, though this may change depending on the revenue mix and level of investments. Ultimately, Citi’s negative view was largely based on lingering execution risk and the belief that RXT’s multi-year transformation may take even longer than planned.

Companies continue to place more workloads in the cloud as they pursue a hybrid approach to IT. The share of enterprise workloads that are run in corporate, on-premises facilities has fallen below 50% for the first time, according to Uptime Institute. The organization expects the percentage of on-premises workloads to continue to shrink, despite lingering concerns about data security. Importantly, Uptime reports that reducing energy use and keeping qualified staff are priorities for data center operators, so keep this in mind when researching prospects in this space.

See you next week.

Josh

Connect with me on Twitter and LinkedIn.

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. Joshua Levine and Third Stream Research were not compensated by any company, directly or indirectly, mentioned in Confluence, and we do not own shares in any companies mentioned.