Quarterly Digest: Q1 2023

Notable winners / Bitcoin miners rebound / Two exceptional biotech IPOs / Biopharma R&D dominated by emerging companies / A ProPhase Labs addendum

Third Stream Research tracks more than one thousand companies in what is arguably the most volatile segment of the U.S. equity markets. We believe it’s also the most fascinating because of the captivating ventures and technologies, adventurous spirit of the people, and astonishing variety of experiences. But this isn’t for entertainment value. The most successful investors embrace persistence, dedication and patience to manage risks, generate profits, and build long term wealth.

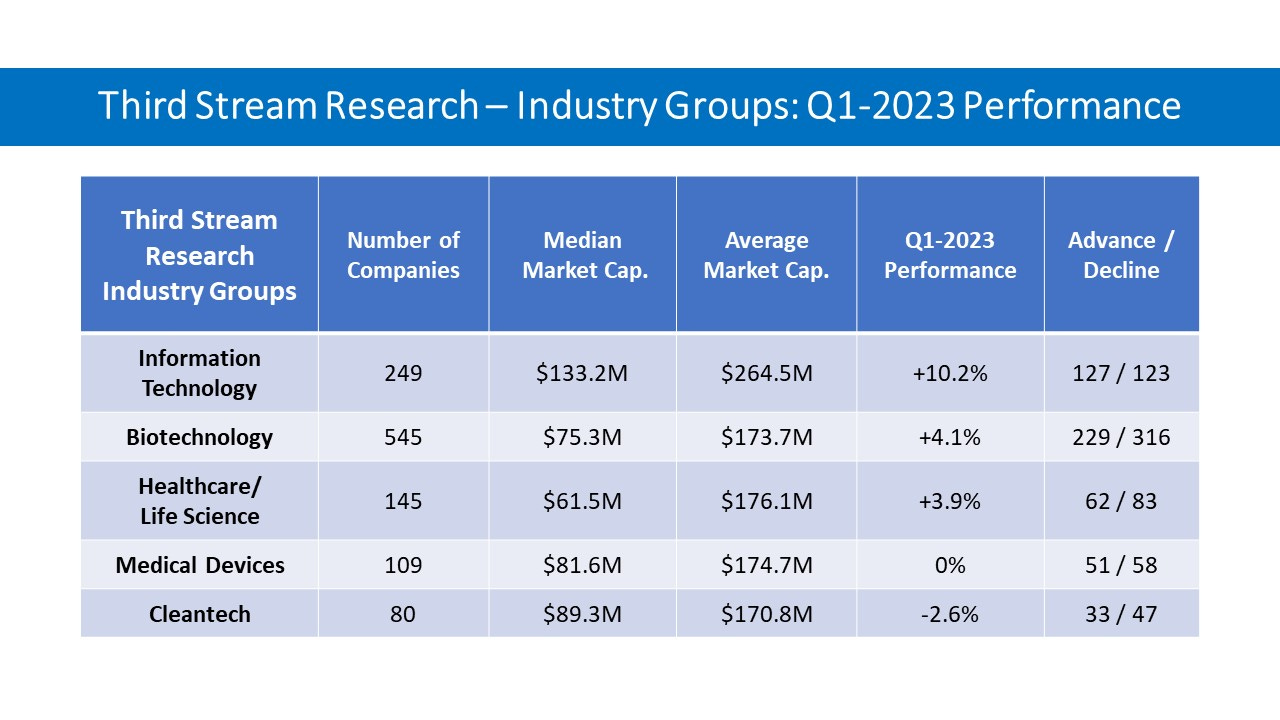

We immersed ourselves in this project to learn about the emerging growth companies (<$1B market cap)—in the Information Technology, Biotechnology, Healthcare/Life Science, Medical Devices, and Cleantech industries—by first assembling an exhaustive database of companies, then continuously monitor their performance and providing context and insights to help investors make informed decisions and identify opportune situations. The new Confluence was launched at the start of this year, so there is much exploring to be done.

This year’s first quarter offered investors a few rays of sunshine after the darkness of 2022. According to Third Stream Research, the 1,128 North-American based small, microcap, and nanocap companies that we track across the most technology-intensive industries had an average gain of +2.95% in Q1 2023. This performance topped the benchmark Russell Microcap Index (-3.08%) over the same period, but trailed the S&P 500 (+7.03%) and Nasdaq Composite (+16.77%).

Negative breadth indicates that a majority of stocks continue to struggle despite improved market conditions, with losers outpacing winners 627 to 502. Still, this was far better than full-year 2022 when losers overwhelmed gainers by an 8-to-1 margin and the overall performance was -52.1%.

However, the battering of the most vulnerable stocks, particularly nanocaps (<$50 market capitalization) and low-priced microcaps (<$2 per share), carried through from last year’s decimation. All of the trends in place in 2022—declining corporate cash levels, harsh dilutive financings, reverse splits (we counted 101 in Q1), CEO resignations, employee layoffs, increasing ‘bag holders’, and a host of macro headwinds—exist in the new year.

It's worth repeating what we wrote in our 2022 performance review in January:

Cash is the lifeline for the overwhelming number of emerging growth companies, particularly in biotech where quarterly burn rates are monitored closely like EKG readings for cardiac patients. Under current stock market conditions, weighed down by interest rates, inflation and a looming recession, the most financially strained businesses face existential consequences. Management and boards will have little choice but to engage in the kind of massively dilutive financings that frequently bury stocks. Separately, mergers and acquisitions will present attractive exits for very few.

It’s unsurprising that the weak are getting weaker. Such trends are painfully clear in the data for the worst performers in the lowest tier of each industry group. For example:

Eighteen of the biggest percentage losers in Cleantech were all trading below $2 per share at the end of Q1 2023. The poor activity generally mirrors longer term downtrends: 15 of the 18 have declined >80% over the last year.

Eleven of the 15 biggest Q1 losers in Medical Devices are down >80% over the last 52 weeks.

In Q1 2023, 22 biotechs declined at least 75%; half of them have plunged >93% over the past year.

Alternatively many stocks in the small-cap tier of the TSR universe produced strong gains in the first quarter. In fact, several leading performers surged well beyond our $1 billion upper threshold during this period. We look at two of them below.

Notable Top Stock Performers: Q1 2023

(>$5 share price; >$50M market capitalization; market caps as of 4/14/23)

Bellerophon Therapeutics (BLPH; $117M): +776.6%

Ambrx Biopharma (AMAM; $549M): +292.9%

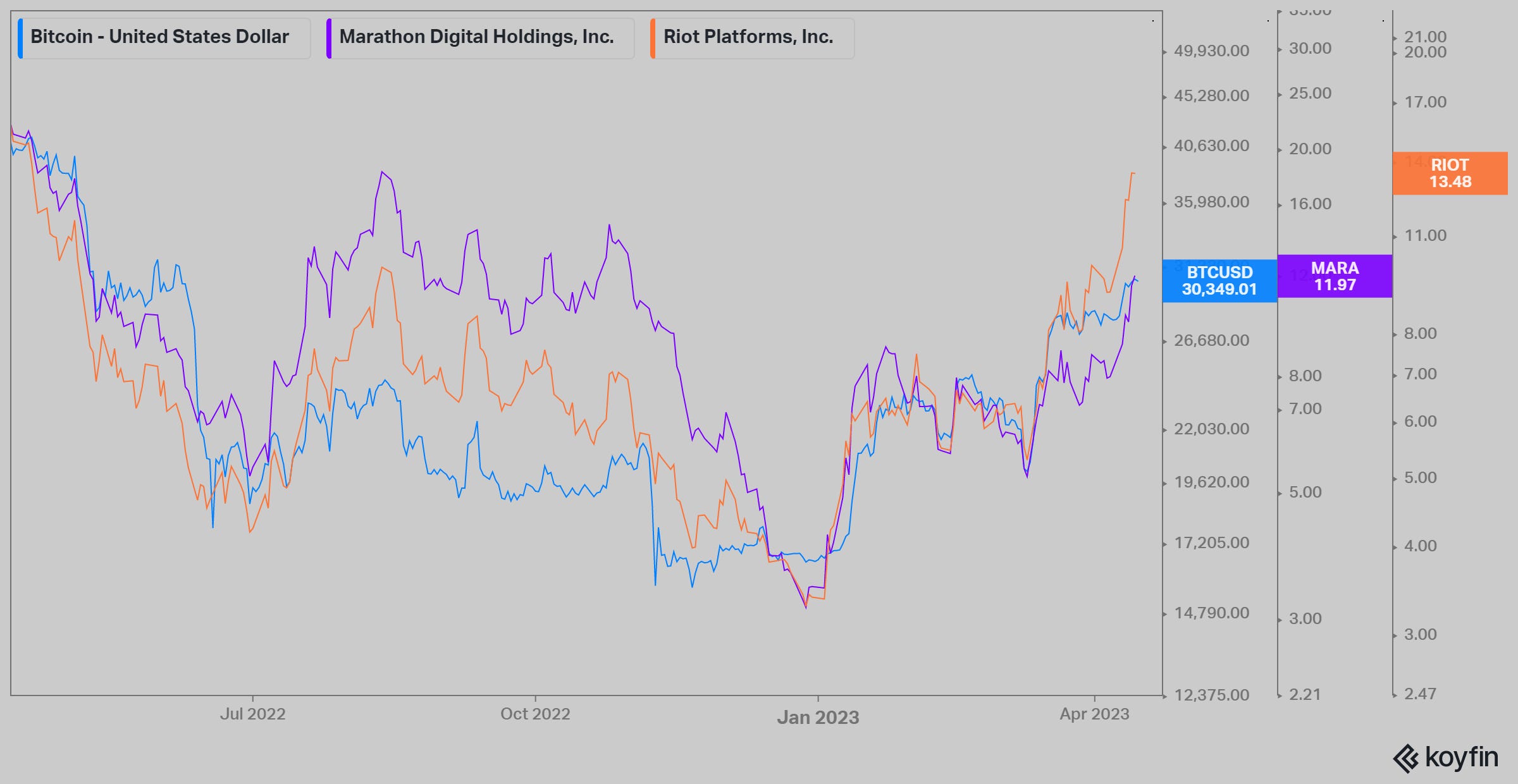

Riot Platforms (RIOT; $2.1B): +160.8%

Marathon Digital Holdings (MARA; $1.9B): +154.9%

Bitcoin Miners Riot Platforms and Marathon Digital Rebound Off Historical Lows

Bitcoin mining is the process of adding transaction records to Bitcoin’s public ledger of past transactions or blockchain. The blockchain serves to confirm transactions to the rest of the network as having taken place. Miners compete to solve complex mathematical problems using powerful computers in order to validate transactions and earn new bitcoins as a reward. The mining process is designed to ensure that new bitcoins are created at a steady rate and that the supply of bitcoins is limited to 21 million. Bitcoin mining requires a significant amount of computational power and electricity, as well as specialized hardware called Application-Specific Integrated Circuit (ASIC) miners. As a result, mining is a highly competitive and expensive process, and it’s dominated by large mining operations.

The price of Bitcoin recently bottomed just below $20,000 on March 10. Thirty days later it had surpassed $30,000. In fact, Bitcoin is up 85.0% year-to-date as of April 14, far exceeding the gains for the Nasdaq 100 (+19.8%) and S&P 500 (+8.3%).

Two of the largest Bitcoin producers in the U.S., Riot Platforms (RIOT) and Marathon Digital Holdings (MARA), have rallied from near-historical lows. The advance was due to a combination of factors, but mainly a renewed interest among investors in risky assets and tech stocks in the wake of shaken confidence in the traditional banking sector. Anticipation of the Federal Reserve possibly ending its rate-hiking cycle has also lifted sentiment.

Riot Platforms (RIOT) is focused on supporting the Bitcoin ecosystem through proof-of-work mining. RIOT generated 695 bitcoin (BTC-USD) in March 2023, reflecting approximately 36% growth from a year earlier. During the same period, Riot sold 675 bitcoin, generating net proceeds of approximately $16.7 million.

For the full year 2022, RIOT had revenue of $259.2 million, consisting of $156.9 million in Bitcoin Mining; $36.9 million in Data Center Hosting, and $65.3 million in Engineering. The company reported a net loss of $509.6 million, as compared to a net loss of $15.4 million in the same period in 2021, which was heavily impacted by non-cash impairment charges totaling $538.6 million.

Marathon Digital’s (MARA) goal is to improve Bitcoin production by increasing the hash rate, or the amount of computing power used by Bitcoin miners to mint new Bitcoins while verifying transactions on the network. The company enjoyed a boost early this year after it recorded a 687 bitcoin production in January 2023, up 45% from 475 bitcoin produced in December 2022.

MARA, which recently announced the retirement of its CFO in May, is coming off a tough year. In February, the company said it would restate its earnings for 2021 and the first three quarters of 2022 after discovering certain accounting errors.

For full year 2022, MARA logged a $686.7 million net loss due to a combination of a more than 60% plunge in the price of BTC and surging energy costs. The shortfall was much wider than the $37.1 million net loss recorded for the year ended December 31, 2021.

Since the end of the first quarter, shares of RIOT and MARA have surged ahead, increasing an additional 35% and 37%, respectively. RIOT is now up 252% this year, and MARA 250%.

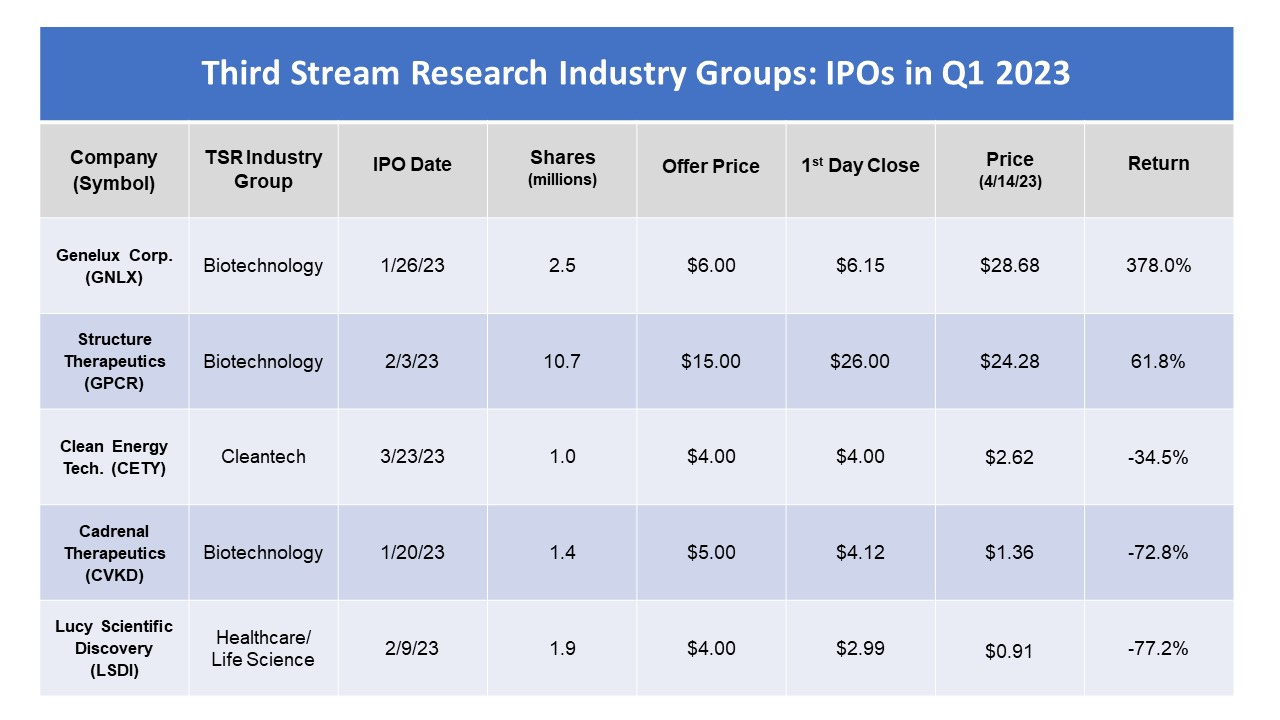

Among the Five IPOs in Q1 2023, Genelux and Structure Therapeutics Emerge as Top Performers

After one of the slowest U.S. IPO markets in decades in 2022, the first quarter offered little solace for anxious investment bankers, or the lengthy pipeline of companies that have filed an S-1. In Q1 2023, venture capital-backed issuers had their slowest first quarter since 2009 with only 23 deals raising $2.2 billion. The median deal size was a low $15 million, according to Renaissance Capital.

The IPO pipeline held 147 companies seeking a total of $14 billion as of late March. That includes 105 companies in what Renaissance calls the “active pipeline” — companies that have filed or updated their filings within the last 90 days. Only 11 of those 105 are looking to raise $100 million or more.

In the Third Stream universe, five companies went public in the first quarter. This select group is representative of our scope of coverage, with market capitalizations ranging from $16 million to $900 million. Their post-IPO performance also reflects a broader pattern that we’ve observed for the past 18 months: the smallest deciles (<$100 million market cap) have had a difficult time. Overall, stocks have generally performed far better among the higher market cap levels.

Genelux’s (GNLX; $709M) short-term gain is impressive by any measure, but it’s even more stunning when we learned the backstory. On January 25, GNLX priced its IPO at $6 a share—the low end of its $6 to $7 a share range. With 2.5 million shares in the IPO, the biotech company raised $15 million with underwriters. Shares of Genelux opened at $6 at around noontime on Day 1, reaching a high of $7.94 before sliding to a low of $5.95 in early afternoon, then closing at $6.15.

Five weeks after its IPO, GNLX shares hit $29.63—a nearly 400% increase—without a single news item on the company.

In February 2023, investment bankers The Benchmark Co. and Brookline Capital Markets purchased an additional 153,000 shares of common stock at $6.00 per share pursuant to the underwriters’ partial exercise of their option to purchase additional shares. This duo is sitting with a nice paper gain from the deal and early investors are smiling, but Genelux’s board of directors and management could be questioning the IPO pricing.

Genelux has been working on oncolytic viral immunotherapies for aggressive or hard-to-treat cancerous tumors. The company recently started Phase 3 clinical trials for its lead drug candidate, Olvi-Vec, in the treatment of ovarian cancer. This is GNLX’s only product candidate in clinical development.

Olvi-Vec (olvimulogene nanivacirepvec) is a proprietary, modified strain of the vaccinia virus, a stable DNA virus with a large engineering capacity having the potential to directly kill cancer cells, stimulate a tumor-specific immune response, and transform immunologically ‘cold’ tumors into ‘hot’ tumors allowing for responsiveness for immunotherapy.

Structure Therapeutics (GPCR; $925M) took a different route than GNLX. Its stock soared 73% after the diabetes drug developer raised $161 million through an upsized IPO on February 3. Shares opened at $25 after being priced at $15 apiece. The stock hit an early high of $27.46 and ended the session at $26.

Structure offered 10.7M ADSs, with each ADS representing three ordinary shares. Underwriters were granted a 30-day option to buy up to 1.6M additional shares to cover over-allotments. Jefferies, SVB Securities, Guggenheim Securities and BMO Capital Markets were joint bookrunners on the deal. Only days before the IPO, Structure had said in a filing that it was looking to raise around $125 million.

Structure, formerly known as ShouTi (the company has operations in the U.S. and China), is developing drugs that target G-protein receptors to treat pulmonary, metabolic and cardiovascular diseases. Its lead drug candidate, GSBR-1290, is a GLP-1 receptor agonist for the treatment of Type 2 diabetes.

Other leading makers of GLP-1 agonists for diabetes include Eli Lilly (LLY), Novo Nordisk (NVO) and AstraZeneca (AZN). Investor interest in the drugs has grown recently amid reports that they're being increasingly prescribed for weight loss.

Two-Thirds of Biopharma Industry R&D Driven by Emerging Firms

According to a report by IQVIA, emerging biopharma companies (EBPs)—those with an estimated expenditure on R&D of less than $200 million and less than $500 million in revenue annually—are responsible for a record 65% of the molecules in the R&D pipeline, up from less than 50% in 2016 and one-third in 20011. This confirms big pharma’s growing dependence on emerging companies for new ideas.

The report also highlights that EBPs are increasingly focusing on rare diseases and oncology. They are also shifting to a fully integrated biotech model, which means they are thinking beyond R&D and shifting focus on commercializing their assets. These biotechs are hence incorporating data generation and access considerations in parallel to clinical development.

“’Emerging biopharma has been rising at roughly 4% a year for each of the last five years,’ Tim Opler, Ph.D., managing director at investment bank Torreya, said during a presentation of IQVIA’s report on global R&D trends. Opler, citing the QVIA data, dubbed the stat an ‘absolutely stunning finding.’”

At work is a combination of factors, including changes in the healthcare landscape, the increasing cost of drug development, and advances in technology.

One big reason is the increasing cost of drug development, which is estimated to have an average cost of $2.6 billion today. This has made it increasingly difficult for larger, established pharmaceutical companies to tackle the financial risk of developing new drugs, leading to a greater focus on partnering with or acquiring emerging biopharma companies.

Another factor is the changing healthcare landscape. With a greater emphasis on personalized medicine and targeted therapies, there is a growing need for smaller, more agile companies that can quickly develop innovative new treatments. This has created opportunities for emerging companies that specialize in niche areas, such as gene therapy or immunotherapy.

Finally, advances in technology have made it easier for emerging companies to compete with larger, established players in the biopharma industry. For example, the rise of cloud computing and big data analytics has made it possible for smaller companies to analyze vast amounts of genetic and clinical data, allowing them to identify new drug targets and develop more effective therapies.

This last point about digital transformation and its impact on emerging growth companies is the heart of Third Stream Research’s investment strategy.

Addendum (April 5, 2023): ProPhase Labs (PRPH) Buys Shares in Lantern Pharma (LTRN)

We had planned to address ProPhase’s investment in Lantern Pharma in a separate research update, but decided to add this note to our April 4 Update Report on PRPH.

On November 21, 2022, Lantern filed a 13G reporting ProPhase as the owner of 910,000 shares of LTRN, representing 8.4% of the outstanding shares. The date of the event was listed as November 8. On this day, 1.06 million LTRN shares had traded—more than 30 times the average daily volume. LTRN’s share price on this day ranged from $4.27 to $4.45. The stock closed at $5.11 on April 4, 2023.

The market responded poorly to the news of ProPhase’s investment. PRPH shares declined 20% immediately after the 13G filing, and the downtrend continued into early March. Unquestionably, at first look this is an unusual transaction for a development-stage company managing the rapid growth of five subsidiaries. ProPhase had already surprised investors when it made its aggressive entry into the biopharma arena in mid-2022.

When asked about the approximately $4 million investment, the respective CEOs suggested only that LTRN was good value (market capitalization is below cash on hand). Additional motivations or potential synergies between the two companies were not disclosed, but the connections are apparent. Lantern deploys artificial intelligence, machine learning and genomic data to streamline drug development and identify the patients that will benefit from the company’s target oncology therapies. The company has more than 10 cancer development initiatives. In addition, Lantern CEO Panna Sharma is an advisor to ProPhase.

Lantern’s RADR® platform, a proprietary A.I. enabled engine it created and owns, currently includes more than 25 billion data points, and uses big data analytics and machine learning to rapidly uncover biologically relevant genomic signatures correlated to drug response, and then identify the cancer patients that may benefit most from its compounds. This data-driven, genomically-targeted and biomarker-driven approach allows Lantern to pursue a transformational drug development strategy that identifies, rescues or develops, and advances potential small molecule drug candidates in potentially a fraction of the time and cost associated with traditional cancer drug development.

We believe that ProPhase’s ~$4 million investment is more than a passive act. Lantern’s A.I. platform and drug pipeline appear to be extremely complementary with Nebula Genomics and ProPhase BioPharma. By taking a significant stake in Lantern, ProPhase demonstrates a commitment that could potentially lead to an alliance or partnership that leverages the strengths of each company. This is consistent with ProPhase management’s strategy of building value through creative initiatives that favorably balance risk and reward.

See you next week, and thank you for your support.

Josh

Connect with me on Twitter and LinkedIn.

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. I do not own shares of companies mentioned.