January Resurrection

January Resurrection

Risk-on for small tech stocks, at least momentarily

January was magic for small and microcap stocks, with losses disappearing over the first four weeks of 2022. (Well, not exactly, although annualizing these returns would do the job). Nevertheless, the gains for many of the beaten-down stocks across Third Stream Research’s industry groups were impressive to start the year.

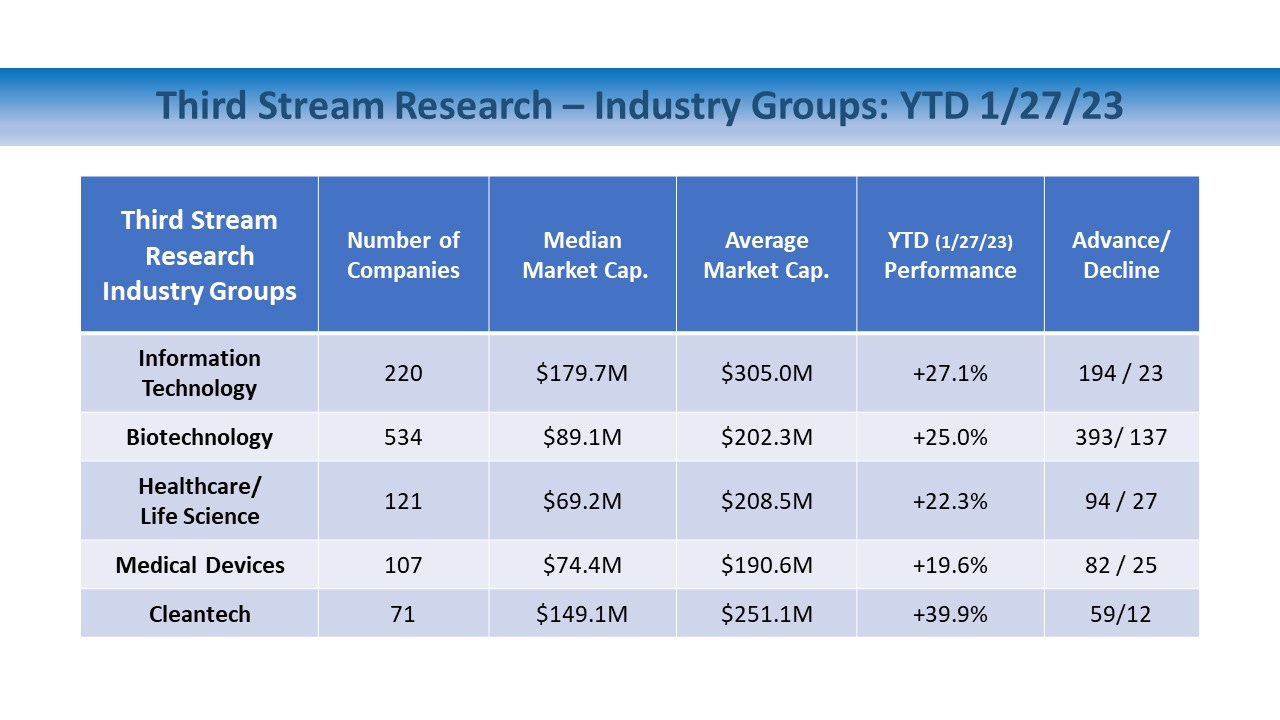

What a shift from last year’s trend. Cleantech, the biggest loser in 2022, recorded an average gain of +39.9% across its 71 components. Information Technology (+27.1%) ranked second, followed by Biotechnology (+25.0%), Healthcare/Life Science (+22.3%), and Medical Devices (+19.6%). The Russell 2000, by comparison, was up +8.5% over the the same period.

Calendar effects in markets are domain to market technicians, traders, short-term investors, and financial media. While the study of market patterns correlated to certain days, weeks, and months over the years may yield some interesting findings, it is of little use to fundamental investors with a long-term view. However, one curiosity that piques the interest of small and microcap investors every year is the ‘January Effect.’

We will not trail off into a discussion about the January Effect, but only point out that there is a strong tendency for year-end tax loss selling in low-priced, low institutional-owned stocks. This selling often weighs on illiquid stocks throughout the holiday period, leading to big percentage slides depending on the market environment and outlook. Investors begin the new year by either repositioning or searching for new bargains in oversold stocks.

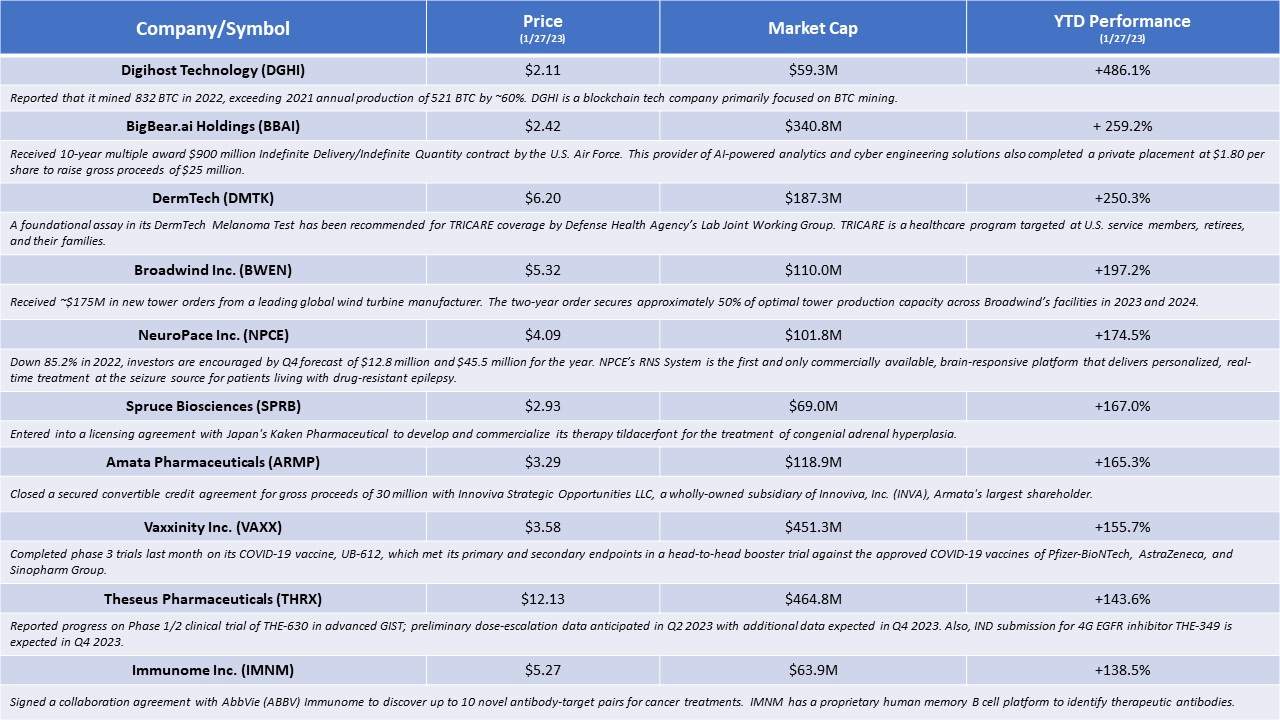

Now, let’s review the biggest winners through last Friday. We find that 44 of the 1,053 stocks tracked by Third Stream Research minimally doubled year-to-date (as of 1/27/23). Because 18 of the 44 stocks were priced below $2, we excluded them from our final tally for the Top 10 winners, which includes a note on what we perceive as the primary catalyst for each stock’s activity.

A few more thoughts on January’s ‘resurrection’ in the our emerging-growth universe of stocks:

The 44 stocks that gained at least 100% represent more than 4 percent of all companies we track. This is the kind of extreme activity that investors will not find in the components of any of the major equity indices.

The Top 10 stocks highlighted above were primarily driven by materially impactful events. Yet some buying was undoubtedly motivated by bargain hunting for attractive values after a lengthy market downtrend.

While enticing opportunities for tactical trading exist in the emerging-growth universe, investors are advised to keep money in a basket separated from long-term investments for this endeavor.

It is helpful to understand how the companies we track (1,053 technology-intensive, emerging-growth companies with market caps under $1 billion) are distributed by size. After the severe downturn last year, now micro-caps and nano-caps together account for more than two-thirds (71%):

Third Stream Research Industry Groups - 1,053 Companies By Size

Small-Cap ($301M - $1B): 308 (29%)

Micro-Cap ($50M - $300M): 370 (35%)

Nano-Cap (<$50M): 375 (36%)

The stocks in our universe are the trifecta-plus-one of volatility among all publicly-traded companies in the U.S. equity markets. Smallest market caps, lowest stock prices, most difficult technological challenges, and weakest corporate fundamentals. In other words, buyers beware. Any investment strategy applied to these stocks that isn’t grounded in understanding the fundamentals of a company is destined for big losses.

First Biotech IPOs in 2023

Cadrenal Therapeutics (CVKD; $28M) and Genelux Corp. (GNLX; $138M) completed their IPOs in January, making them the only biotech companies to do so in what has been an unusually quiet start for new issues this year.

Settling for Less

Cadrenal Therapeutics launched on January 20, with its shares priced at $5. After trading as high as $6.75 in its first hours, CVKD sunk as low as $3.83 and closed day one at $4.12. The shares trended lower in subsequent days, closing at $2.62 on January 30, down nearly 50% from its IPO price.

The company offered 1.4 million shares at $5 per share, raising $7 million. The deal was downsized from an earlier proposal that sought to raise $10 million.

Cadrenal is developing a compound called tecarfarin for the prevention of blood clots in patients with end-stage kidney disease or atrial fibrillation. On January 23, the FDA had granted a Fast Track designation to tecarfarin for the prevention of systemic thromboembolism, more commonly referred to as blood clots of cardiac origin in patients with end-stage renal disease and atrial fibrillation.

Genelux began trading on January 26 with its $15 million IPO. The company offered 2.5 million shares priced at $6 per share. Underwriters were given a 30-day option to buy up to 375,000 additional shares to cover any over-allotments. GNLX first filed for an IPO in June, seeking around $30 million.

Genelux has been working on oncolytic viral immunotherapies for aggressive or hard-to-treat cancerous tumors. The company recently started Phase 3 clinical trials for its lead drug candidate, Olvi-Vec, in the treatment of ovarian cancer.

GNLX traded as high as $7.94 on its first day before ending at $6.15. The shares closed at $5.83 on January 30, down slightly from its $6 offering price.

Biotech and Life Science Companies Take Hits on Securities Offerings

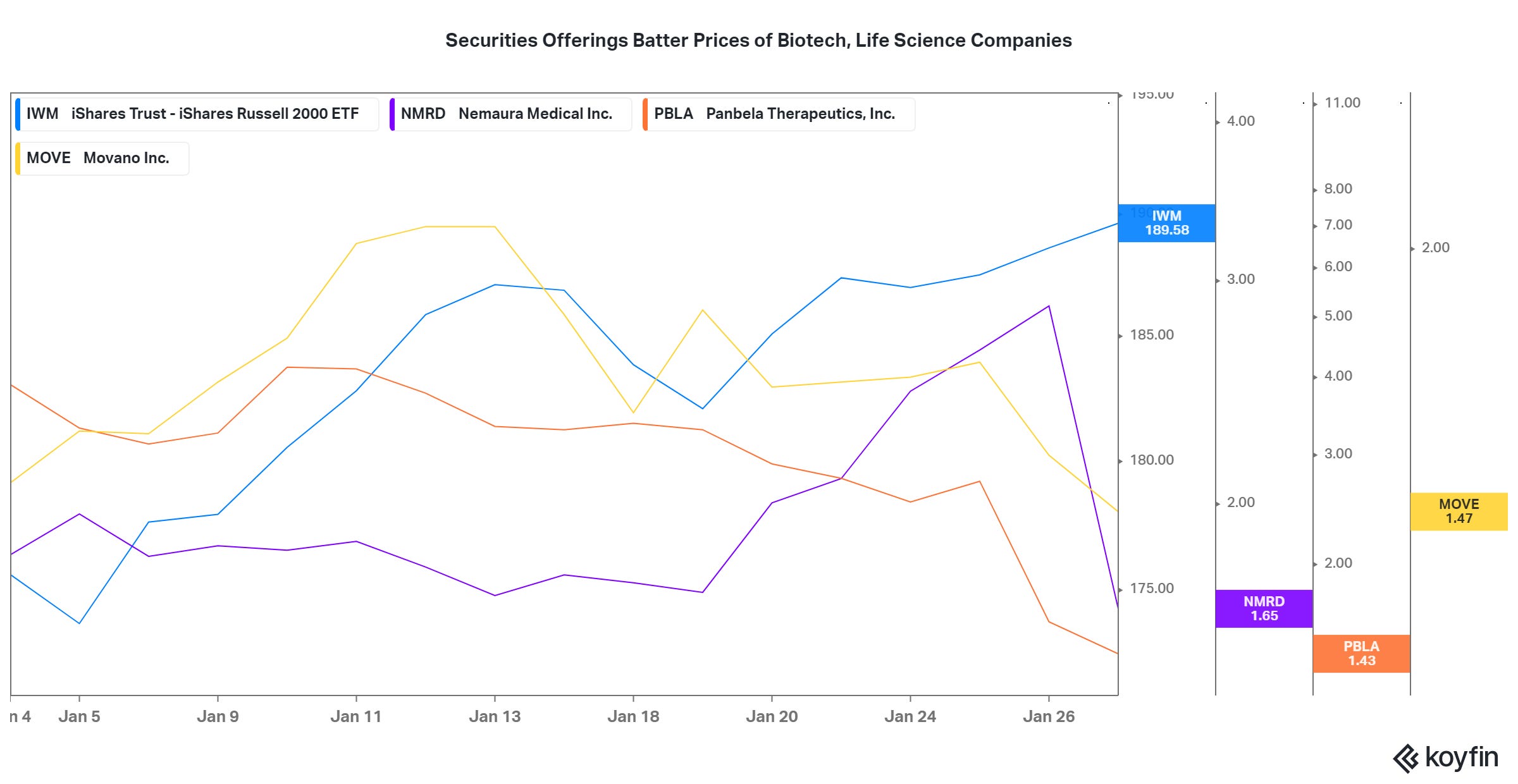

Share prices of Nemaura Medical (NMRD), Panbela Therapeutics (PBLA), and Movano Health (MOVE) fell sharply after each company announced a securities offering. Although stocks typically drop in response to such deals, the steep declines reflect current hurdles for small biotech and life-science firms in need of cash to sustain R&D efforts and progress in early-stage pipelines.

Nemaura Medical (NMRD; $36M) shares plunged 43% last Friday after the company priced a ~$8.4M securities offering. The offering comprises 4,796,206 shares of common stock, issued in a registered direct offering, and warrants to purchase up to 4,796,206 shares, issued in a concurrent private placement.

The combined purchase price for one share and one warrant is $1.75. The warrants have an exercise price of $2.00/share. NMRD closed at $1.58 on January 30. The company, which is developing a non-invasive wearable sensors and supporting personalized lifestyle and weight reduction programs, reported $580,000 in revenue over the last 12 months.

Panbela Therapeutics (PBLA: $13M) priced its public offering last Thursday. It consisted of 6,675,000 shares of its common stock and warrants to purchase up to 13,350,000 shares at $2.25 per share and warrant. The warrants will have an exercise price of $2.75 per share and will expire five years following the date of issuance.

Shares dropped 41% following the news of the ~$15 million raise. PBLA, which executed a 1-for-40 reverse split in January, is down 99% over the last two years.

Panbela is a clinical-stage biopharmaceutical whose lead assets target the suppression and prevention of tumor growth, enhancement of anti-tumor activity of other anti-cancer agents, and modulation the immune system. That’s a tall order for a biopharma of any size.

Movano Health (MOVE; $46M) priced its $6.5 million securities offering last Friday, comprising 4,644,000 shares of the firm's common stock and warrants to purchase up to 2,322,000 shares of common stock, each issued at $1.40. The warrants are being sold at the rate of one warrant for every two shares of common stock and will be exercisable at a price per share of $1.57.

MOVE shares held up reasonably well following the news, sliding less than 15%. It closed at $1.27 on January 21.

The healthcare solutions company is developing the Evie ring, designed to help women track and manage their sleep quality and menstrual cycles through perimenopause. Movano did not report any revenue for the last 12 months.

Expect biotechs to cut research spending and more aggressively pursue partnering deals and M&A in 2023

A recent report published by the life sciences arm of accounting and consulting firm BDO provides the findings from its annual poll conducted with 100 of the sector’s CFOs.

Nearly 20% of responders are planning to reduce research costs, compared to only 2% who indicated the same entering 2022.

Forty-five percent plan to sign a collaboration or licensing deal to extend their cash runway. Mirroring our main points in the first Confluence of this year, BDO reports that most respondents said investors are doing more due diligence than they were in recent years, and about half indicated funding is harder to secure.

The most popular methods of preserving cash involve outsourcing development, manufacturing and clinical operations jobs. Next are partnership deals and M&A, though executives are considering layoffs, pipeline reorganizations and debt raises as well.

Surprisingly, 13% of respondents are eyeing an IPO, compared to 6% a year ago and more in line with the numbers reported in 2020 and 2021.

The biotech finance infrastructure — encompassing venture capital and the public equity markets — remains vibrant and always ready to reaccelerate. However, when the allure of IPOs returns, investors will have a greater appetite for companies beyond phase 1 and 2, and as far along as the product stage. Capital allocators to pre-clinical and early-stage biotechs will become progressively more discriminating this year.

See you next week, and thank you for your support.

Josh

Connect with me on Twitter and LinkedIn.

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. I do not own shares of companies mentioned.