Innovation’s Single Purpose

Innovation’s Single Purpose

Creating new value for customers

Innovation is the secret sauce that successful companies use to create new value. Insights into the recipe and process can be useful for investor outperformance in emerging growth stocks.

Management guru Peter Drucker (1909-2005), who devoted his life to understanding entrepreneurship, believed innovation to be the task of endowing human and material resources with new and greater wealth-producing capacity. Let’s start with this as the baseline.

In his 1985 classic “Innovation and Entrepreneurship” Drucker identifies seven sources for innovative opportunity. First, the internal sources:

The Unexpected

Exploiting phenomena that arise within the business’ sphere; an ability to recognize changing patterns and build a new market position on those patterns.

Incongruities

Often times disguised as macro-phenomena, which occur within a company or a business sector. They might resemble discrepancies in economic realities, in the logic of a process, or between perceived and actual customer values and expectations.

Process Need

One ‘missing link’, or a common realization that ‘there ought to be a better way’. There must be some sort of knowledge to do the job required, and the solution must fit the way people do the work and want to do it.

Market Structures

A change in industry structure offers exceptional opportunities, which don’t have to be perceived as threats. The most common trait of these indicators is the rapid growth of an industry.

Shifting to the three external sources:

Demographics

Changes in population, its size, age structure, composition, employment, educational status, and income. Businesses’ value propositions should be shaped around these differences.

Changes in Perception, Meaning, and Mood

More nuanced than demographic factors, but nonetheless essential for marketplace position. Companies must be able see what’s happening in the current environment and anticipate what will happen in the future.

New Knowledge

The knowledge-based source is time-consuming yet more valuable; it is also way riskier than the above-mentioned ones, and it therefore requires time for calculating the probabilities, or weighing risks vs. rewards.

Sources of innovation are constructive for investors as a checklist for organizing the various factors driving corporate innovation. Once identified, it becomes easier to analyze management decisions and actions.

Innovation cannot be isolated and measured like sales of product and services. Rather, it’s an all-encompassing process of doing business that evolves from corporate culture and permeates into all aspects of the company. When innovation is successful, the results translate directly to growth and financial performance.

A Measure of Success

Broad measurements of innovation by government agencies and consulting firms tend to look at either the macro (countries) or micro (corporations). Essentially they select various indicators of innovation and then plug them into a spreadsheet to create a list of winners and losers.

One popular annual ranking is supplied by Boston Consulting Group (BCG) — the second largest management consulting firm by revenue — which polls 1,600 global innovation professionals. To create its top 50 innovative company ranking, BCG uses four variables:

Global ‘Mindshare’: The number of votes from all innovation executives.

Industry Peer Review: The number of votes from executives in a company’s industry.

Industry Disruption: A diversity index to measure votes across industries.

Value Creation: Total share return.

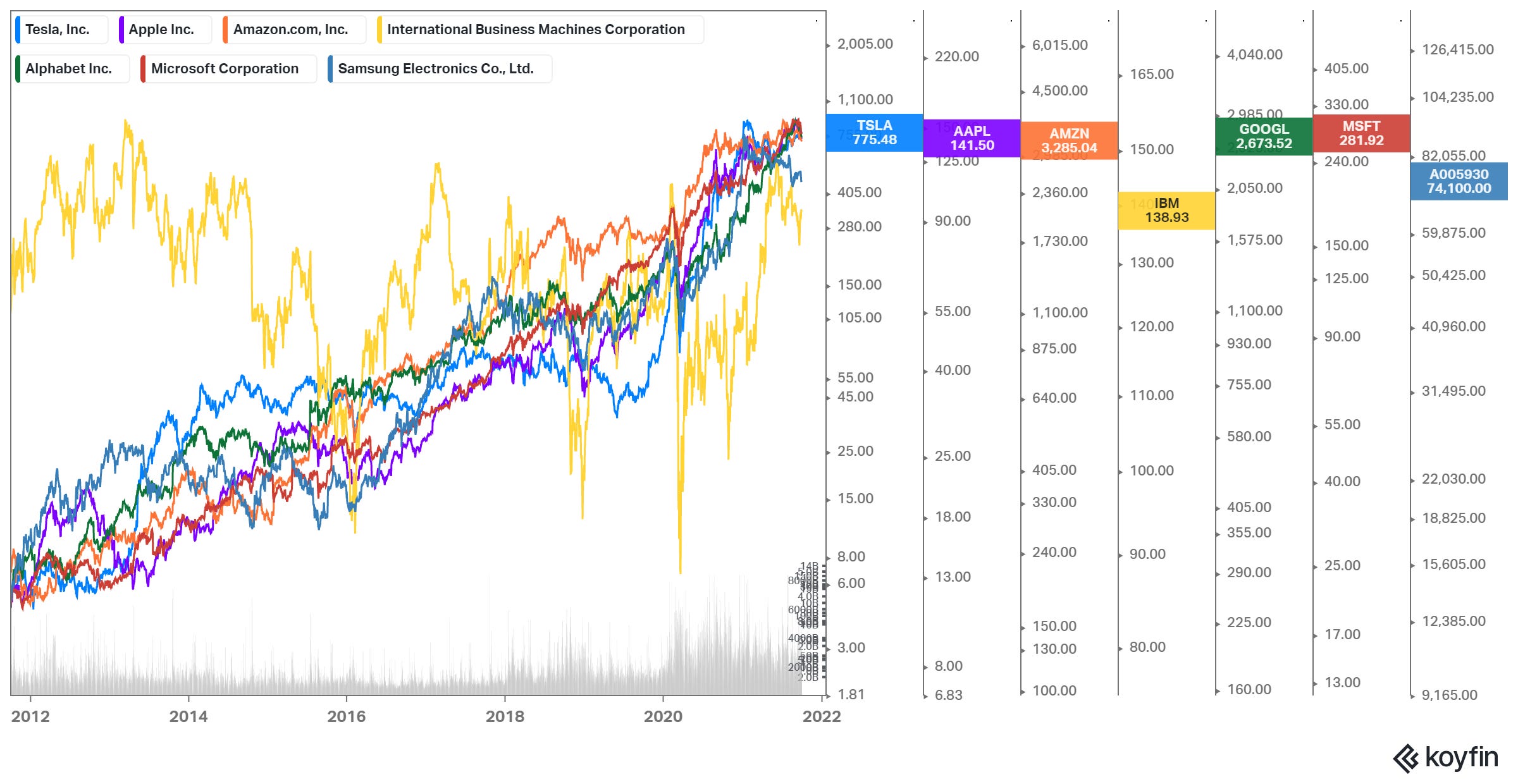

For the second year in a row, Apple claims the top spot on the 2021 list, followed by Alphabet/Google, Amazon, Microsoft, Tesla, Samsung and IBM. While the first six are fairly predictable, seventh-place IBM is a surprise: the company’s revenues have been on a downtrend for a decade and are currently 27% below its 2012 level. A comparison of the 10-year stock performance illustrates the IBM anomaly.

The CEO of IBM, Ginni Rometty, capped IBM’s decade-long pursuit of shareholder value, with this summation: “At the end of the day, it’s about returning value to shareholders.” The financial results of this approach speak for themselves: Apple is worth $2.4 trillion and Microsoft is worth $2.1 trillion. IBM is worth a mere sliver: $0.13 trillion.

IBM is still considered a leading innovator by its peers (three out of the four variables are indicators of popularity and influence), possibly because of its longstanding position as a top recipient of U.S. patents. In 2020 IBM led with 9,130 inventions, followed by Samsung, Canon, and Microsoft. Others in the top 10 include Apple and Intel.

Sadly, the old-time tech giant failed to transform its capacity for innovation into new value for its customers. As Peter Drucker famously said, “there is only one valid purpose of a corporation: to create a customer.” Disrupted by smaller competitors over several decades, IBM has never been able to keep up as the industry accelerated through multiple transitions. Over the last 12 months, IBM’s sales declined 1.5% to $74.4 billion, underscoring the company’s continued growth challenges.

In comparing the leaders to the laggards, the most significant gap seems to be in what BCG calls innovation practices — things like project management or the ability to execute an idea that’s both efficient and consistent with an overarching strategy. To overcome this obstacle, BCG says companies need to foster a “one-team mentality” to increase interdepartmental collaboration and align team incentives. That’s consultant-speak for: go figure it out yourself.

Upstarts’ Takedown of the Goliaths

Twenty years after he introduced the theory of ‘disruptive innovation’, Clayton Christensen and two co-authors in 2015 attempted to clarify what classic disruption entails and acknowledge its shortcomings.

Common mistakes, they said, include failing to view disruption as a gradual process, (which may lead incumbents to ignore significant threats) and blindly accepting the ‘disrupt or be disrupted’ mantra (which may lead incumbents to jeopardize their core business as they try to defend against disruptive competitors). They wrote:

“‘Disruption’ describes a process whereby a smaller company with fewer resources is able to successfully challenge established incumbent businesses. Specifically, as incumbents focus on improving their products and services for their most demanding (and usually most profitable) customers, they exceed the needs of some segments and ignore the needs of others. Entrants that prove disruptive begin by successfully targeting those overlooked segments, gaining a foothold by delivering more-suitable functionality – frequently at a lower price. Incumbents, chasing higher profitability in more-demanding segments, tend not to respond vigorously. Entrants then move upmarket, delivering the performance that incumbents’ mainstream customers require, while preserving the advantages that drove their early success. When mainstream customers start adopting the entrants’ offerings in volume, disruption has occurred.”

The problem with conflating a disruptive innovation with any breakthrough that changes an industry’s competitive patterns is that “different types of innovation require different strategic approaches”, according to Christensen. This is evident in Drucker’s seven sources of innovation.

Companies with market capitalizations between $50 million and $5 billion, disruptive or not, tend to be more volatile and less liquid than larger companies. Emerging growth companies (EGCs) have more limited product lines, markets, or financial resources and typically experience a higher risk of failure than large cap companies.

While the stock market is the ultimate valuator machine, EGC investors can gain an important edge by putting a magnifying glass over how innovation works within an organization. In the context of Drucker’s sources of innovation or BCG’s methodology for compiling its top innovators’ list, smaller companies need to be judged differently than market leaders.

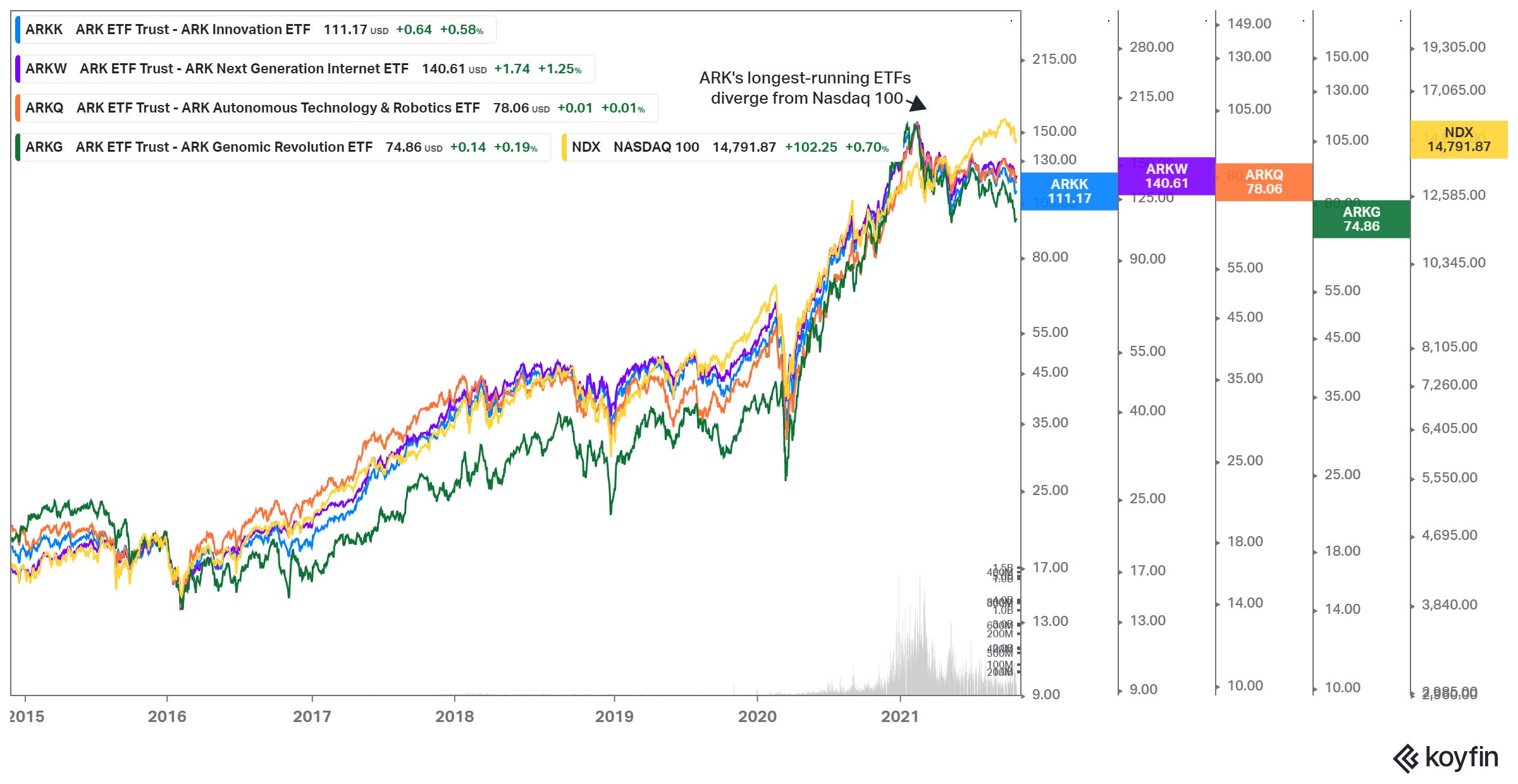

Perhaps no individual represents investment strategies for disruptive innovation better than Cathie Wood, CEO of ARK Investment Management. ARK frames disruptive innovation in broader terms than Christensen, seeing it as the introduction of a technologically enabled new product or service that potentially changes the way the world works.

In a recent Bloomberg interview, Wood described why she so fervently believes in the stocks her fund buys, covering tech segments like autonomous technology and robotics, next generation Internet, genomic revolution and fintech innovation:

“… Since the tech and telecom bust and the ’08-’09 financial meltdown, there’s been a significant increase in risk aversion in the market. And so many investors and analysts invest very closely to their benchmarks. They don’t want to stray much.

The problem is this innovation is going to be very disruptive to the traditional world order. So the benchmarks today are constructed based on companies’ past successes. But if disruptive innovation is evolving to such a rapid extent, there’s going to be disintermediation and disruption. Companies that have learned to satisfy short-term shareholders – who want their profits and want them now – have been leveraging up to buy back shares and pay dividends.

Companies haven’t been investing enough in innovation, and we’re going to see a lot of carnage out there increasingly during the next five to 10 years. At the beginning of the S&P 500 indexes initiation, the average lifespan of a company was 100 years. We believe it’s down to a little over 20 years now – but it’s going to collapse going forward.”

Wood’s assessment of the markets, in general, is accurate. Same for the thinking on corporate strategies. ARK’s ETF funds target high-risk, high-reward investments that anticipate where the global economy will be in a decade or beyond. However, critics of ARK (e.g., short-sellers) see bubble-like values in mostly unprofitable companies, burning through cash in pursuit of otherworldly visions and pots of gold on the other side of rainbows.

Indeed short-sellers will have opportunities to capitalize on wild swings. Extreme volatility is part of the game. ARK Innovation, the flagship ETF launched seven years ago, is up 30% over the past year but down 29% from its Feb. 16 peak. ARK became a household name after this fund’s price quadrupled from March 2020 to last February.

In ARK, investors can allocate a thin slice of their portfolio to a mix of companies developing new and complex technologies, with the potential for disrupting entrenched businesses and industries. ARK also earns points for transparency by posting its holdings daily on its website and emailing trade notifications.

Assembling Stories and Narratives for EGCs

Inventing something new or novel is just one form of innovation. While we often think of R&D and innovation as being synonymous, the former is just one innovation technique.

A popular approach for gauging a company’s R&D quotient is calculating R&D spending as a percentage of sales. This metric works best when it is part of an analysis on competitors and peers, especially big pharma. Another common approach counts the number of patents and patent citations. Again this also generally applies to larger firms.

Companies innovate in several dimensions, like redesigning core operating processes to improve margins or targeting an underserved customer segment. The sources of innovation, as Drucker explains, are diverse and each source require us to consider a different set of criteria.

We said earlier that innovation permeates an entire organization. So there are several paths for mapping an EGC’s ability to innovate across segments of the company. Here are a few lines of inquiry (Focus/Questions/Reasons) where even minimal information and intelligence — from management and employees, experts and consultants, major shareholders, customers, suppliers and competitors — are worth the effort:

Management Vision

How would you describe the company's culture? (Perhaps the most telling characteristic of any company. Critical that it is well articulated.)

What differentiates company from competitors? (How company views its place in the competitive landscape and its strategic edge.)

What kind of company do you want to have in 2 years, 5 years? 10 years? (The company’s long-term vision; what it wants to be when it grows up.)

Originality of Ideas

What are the company's best or most original ideas? And why? (A good test to see if the company can back up its own PR.)

What is proprietary in technologies and products? (Important, strategically differentiating factors.)

R&D Strategy

Primary goals of R&D strategy? (EGCs are rarely successful when not laser-focused.)

What is history of R&D successes and failures? Payoffs? (Any track record would increase probability of future successes.)

What is primary focus, biggest programs, expectations? (Indicates priorities and where company sees highest potential value.)

Who are key people in R&D? Background? (People are most important resource, period.)

R&D spending multi-year trends? (If levels aren’t maintained or growing, the reason is important to learn.)

R&D spending by percentage: new product lines, new science or technology to company or market? (Should be aligned with company’s longer term strategy and strengths.)

Agility and Flexibility

How capable is company of pivoting? Any examples? (Could the company manage a pivot if it was confronted with the situation.)

Initiatives to adapt products to meet with customer demands? (Essential for delivering ongoing value to customers.)

Adjusting to marketplace changes in a business environment? (The big winners prove their worth during such events.)

Taking advantage of available human resources? (Again, the best performers strike quickly when the opportunities arise.)

Digital Transformation

Degree of digital transformation; what stage, long-term plans? (Companies pursuing DT have a decided edge over competitors at earlier stage of commitment.)

What changes have occurred; what are expectations? (Details can help to fill in blank spots in running of operations.)

Return on DT investment? (Is company investing wisely and experiencing tangible results.)

Which areas of the business most positively impacted? (Another angle into determining if company’s tech spending is aligned with broader strategies.)

Innovation is about quality. It’s about new value. It’s not about new things. Innovation is relevant only if it creates value for customers — and consequently for the company and its stakeholders. Thus creating new stuff, by itself, is not sufficient for business innovation.

See you next week, and thank you for your support.

Josh

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our Website and wish to rely upon, whether for the purpose of making an investment decision or otherwise.