Extreme Investing

Extreme Investing

Top-tier performers stand apart/Biotech dominates leaderboard/Small emerging-tech companies mired in bear market

Any observer of the universe of technology-intensive small, microcap, and nanocap stocks is aware of the incredible range of experiences and potentialities—from companies attracting substantial institutional buying to fledgling businesses running on fumes. This week, Third Stream Research quantifies this vast divide and explores the best performers over the last year.

The total market capitalization of the 1,000+ companies we track places this collective slightly above Salesforce (CRM; $199.7B) at approximately $212 billion. With an average market value below $200 million and median of ~$86 million, less than 1-in-10 operate profitably. Yet investors who learn to navigate this treacherous landscape, and identify underlying trends and patterns, can readily improve probabilities for successful outcomes.

Quintiles: How Do They Measure Up?

Data often embodies narratives and stories, which enlighten us about primary trends in support of investing strategies. By examining the stock performances of the companies in Third Stream Research’s industry groups, we discovered several valuable things.

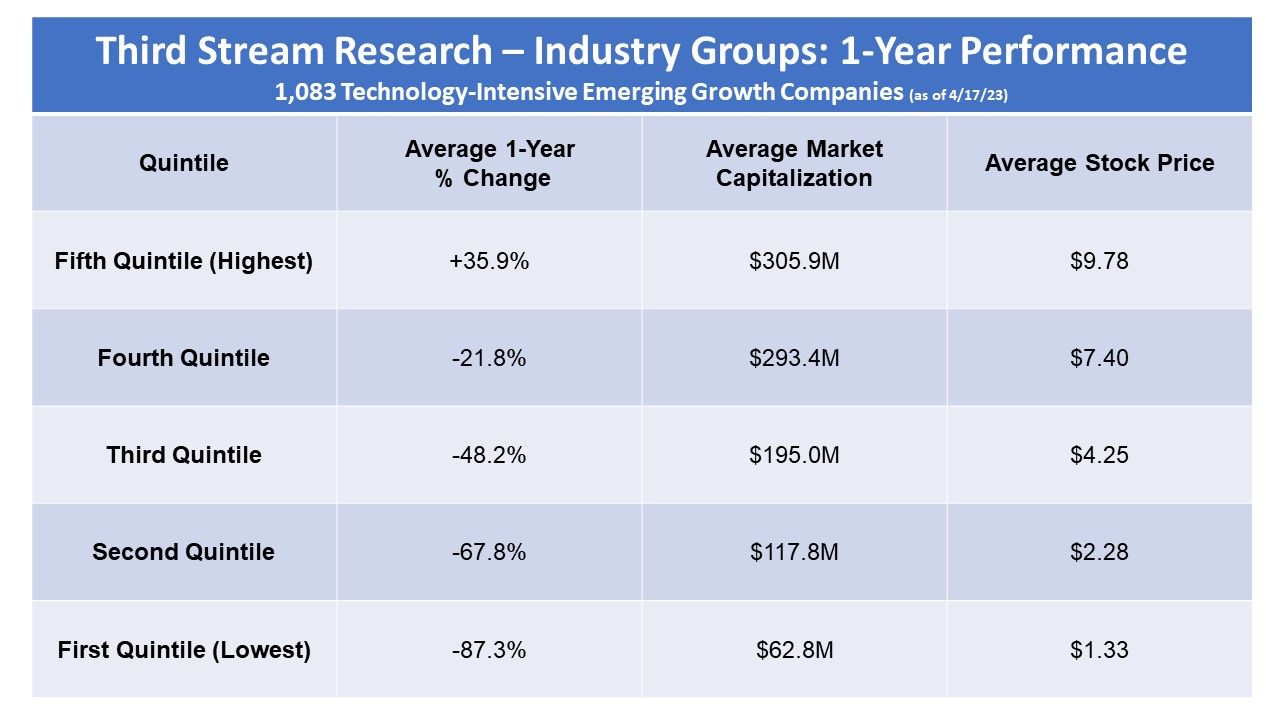

Overall, the 1,083 stocks in our scope (>$5M market cap) had an average decline of -34.1% over the past year (as of 4/17/23), well below the microcap benchmark and other major U.S. stock indices.

1-Year Performance: As of April 17, 2023

TSR Industry Groups: -34.1%

Russell Microcap Index: -17.4%

Nasdaq 100: -7.9%

S&P 500 Index: -5.5%

Yes, the Adventure Stocks in our database generally underwhelmed. But when we sort the more than one-thousand stocks by quintile, we find that an exclusive group (the highest one-fifth) did astonishingly well. With a 35.9% gain for the year, the fifth quintile topped the S&P 500 Index by over 41 percentage points, despite having 21 stocks with losses.

A second important finding: beyond the exceptional performance of the fifth quintile, the stocks in the other four quintiles have been mired in a severe bear market. In fact, the bottom three quintiles averaged a -67.7% decline.

Moving from the second to fifth quintiles, we see a clear pattern: the stocks get progressively weaker on a fundamental basis and it’s strongly correlated with the size of the market capitalization and share price. In other words, the smaller the company, the more likely its stock performed badly over the past 12 months.

Fundamental Difference

Our data indicates a sharp divergence between the biggest winners and the majority of the companies, which declined in the 12-month period we’re examining.

Of the 1,083 companies:

More than 4-in-5 (82.5%) suffered share-price declines over the past year.

9-in-10 reported a net-loss over the past 12 months.

More than one-third (35.2%) generated under $1 million in revenues LTM.

A glance at the companies that doubled in price in one year reveals;

100%+ Gainers: 24 companies.

Average Market Capitalization: $491.2 million

Average Share Price: $12.34

A closer look at the 10 companies that minimally tripled confirms that bigger is better for investors navigating this landscape:

Only two are microcaps (market cap <$300M).

8 of 10 have double-digit prices (including one at $9.99).

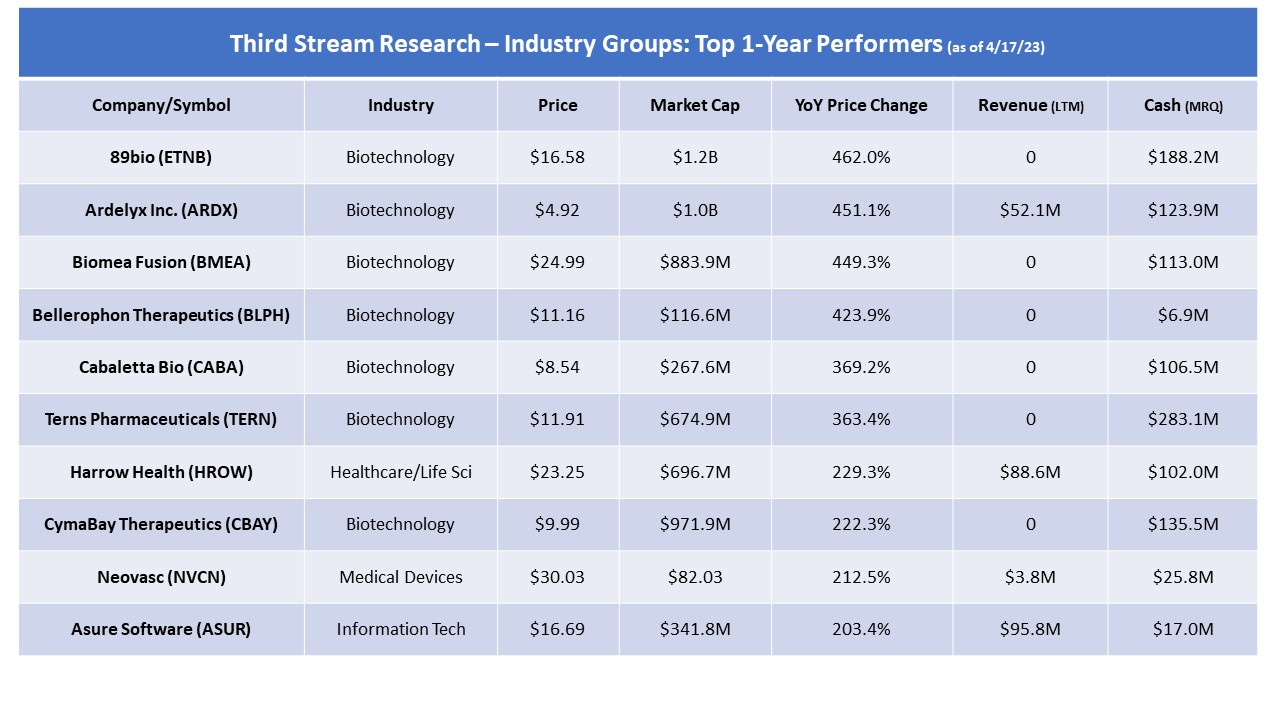

More strikingly, biotech companies dominated among the leaders; revenues, or lack of them, makes little difference:

6 of 10 reported zero revenue for the past 12 months.

7 of the top 8 gainers are in the Biotechnology industry.

While revenues are not necessarily a requisite for big winners in emerging growth, cash does matter. We find that 7 of 10—six biotechs—are blessed with at least $100 million in cash and cash equivalents. There’s a lesson here for investors.

89bio, Inc.’s (ETNB) Rollercoaster to the Top

89bio, the best performer in our industry groups with a 462% gain, didn’t exactly start at the bottom.

89bio was founded in 2018 as a subsidiary of Teva Pharmaceuticals (TEVA) with the goal of developing therapies for liver and metabolic disorders. Its lead drug candidate, BIO89-100, is a long-acting glucagon-like peptide-1 analog being developed for the treatment of nonalcoholic steatohepatitis, a type of liver disease that affects millions of people worldwide.

In 2018, 89bio raised $60 million led by OrbiMed Israel together with OrbiMed US and Longitude Capital, and joined by RA Capital Management and Pontifax. In 2019, TEVA spun off 89bio as an independent publicly traded company. The spinoff was completed through a distribution of 89bio shares to Teva's shareholders.

89bio launched a successful, upsized IPO on November 13, 2019 that priced at $16.00 per share. The gross proceeds of the offering were approximately $97.6 million which included the exercise in full by the underwriters of their option to purchase additional shares of common stock. ETNB traded as high as $47 in March 2020 before hitting as low as $2.00 in April 2022.

Following the spinoff, 89bio continued to develop BIO89-100, which has shown promising results in early-stage clinical trials. The company also expanded its pipeline to include other novel therapeutics for liver and metabolic disorders.

The spinoff allowed 89bio to operate independently and focus solely on its R&D efforts, without the potential distractions and constraints of being part of a larger pharmaceutical company. It also provided an opportunity for Teva to streamline its operations and focus on its core business areas. 89bio is headquartered in San Francisco with operations in Herzliya, Israel.

ETNB raised an additional ~$275 million last month in a public offering price at $16.25 per share. At the end of last year, the company had reported a cash balance of $188.2 million, so 89bio is in good shape to develop its pipeline.

Double Club

In addition to the top 10 companies with gains above 200%, an additional 14 stocks at least doubled for the year ending April 17, 2023. Once again, biotechs led with eight spots.

Ambrx Biopharma (AMAM/Biotech/$608.9M): +176.1%

Aldeyra Therapeutics (ALDX/Biotech/$608.1M ): +127.8%

Broadwind (BWEN/Cleantech/$95.8M): +125.6%

Entrada Therapeutics (TRDA/Biotech/$595.7M): +122.3%

Reviva Pharmaceuticals (RVPH/Biotech/$98.3M): +120.6%

Annexon Inc. (ANNX/Biotech/$240.8M): +119.8%

Maxeon Solar Technologies (MAXN/Cleantech/$1.28B): +114.8%

Assertio Holdings (ASRT/Healthcare/LifeSci/$345.4M): +110.5%

Compass Therapeutics (CMPX/Biotech/$405.4M): +109.8%

scPharmaceuticals (SCPH/Biotech/$368.7M): +107.4%

Ocuphire Pharma (OCUP/Biotech/$121.5M): +107.1%

Merrimack Pharmaceuticals (MACK/Biotech/$182.0M): +105.6%

AVITA Medical (RCEL/Med Devices/$391.4M): +104.3%

eMagin Corp. (EMAN/Info Tech/$179.7M): +103.7%

The characteristics we cited about the top 10 gainers are similar here, reinforcing the strong bias in the current market environment toward biotech companies with sufficient capital to support late clinical-stage pipelines for at least two years. Wildly speculative ventures in biotech and the other industry groups are largely out of favor in the current market environment.

An additional four biotech companies had earned their way among our top gainers lists, but were either acquired or merged at premiums during Q1 2023. Three of the four buyers were non-U.S. companies.

AVEO Oncology (formerly AVEO), a commercial stage, oncology-focused biopharmaceutical company merged with LG Chem (South Korea). AVEO stockholders received $15.00 per share in cash upon the closing of the transaction, which had an implied equity value of $571 million.

AVEO plans to accelerate the commercialization of new anti-cancer drugs developed by LG Chem Life Sciences. With strong capabilities in early-stage R&D and production process, LG Chem Life Sciences will pursue promising anti-cancer therapies and commercial processes for pre-clinical and early clinical trials, while AVEO, with its broad expertise in clinical development and sales in the U.S. market, will oversee clinical development and commercialization.

Concert Pharmaceuticals (formerly CNCE) was acquired by Sun Pharmaceutical Industries Limited (India) for an upfront payment of $8.00 per share of common stock in cash, or $576 million in equity value. Concert stockholders also received a contingent value right, based on sales milestones, entitling them to an additional amount of up to $3.50 per share of common stock in cash. The deal is the Indian drugmaker's biggest since its $3.2 billion acquisition of generic drug maker Ranbaxy Laboratories Ltd in 2014.

Concert's lead candidate, deuruxolitinib, is currently being evaluated in a late-stage study as a treatment for autoimmune condition alopecia areata, which affects more than 300,000 people in the United States each year. Sun Pharma said its immediate focus would be to follow Concert's plan to submit a marketing application for its lead candidate to the FDA in the first half of the year.

F-star Therapeutics (formerly FSTX) was acquired by invoX Pharma, a U.K.-based wholly-owned subsidiary of Sino Biopharmaceutical Limited (China), for an aggregate cash consideration of ~$161 million, or $7.12 per share.

F-star is currently executing Phase 2 trials in Europe and the U.S. in patients with PD-1 acquired resistant head and neck cancer, and in checkpoint inhibitor-naïve patients with non-small cell lung cancer and diffuse large B-cell lymphoma. The Company also has further earlier clinical studies underway with patients in both geographies.

Imara Inc. (formerly IMRA) merged into Enliven Therapeutics (ELVN; $816M), a clinical-stage precision oncology company focused on the discovery and development of next-generation small molecule kinase inhibitors. Concurrent with the merger, Enliven completed a $165 million private placement, giving ELVN a cash runway through multiple clinical milestones and into early 2026.

In connection with the closing of the merger, Imara enacted a 1-for-4 reverse stock split of its common stock and issued one right for each outstanding share of Imara held by stockholders of Imara. Following the reverse stock split and closing of the merger, there are approximately 41.1 million shares of the combined company’s common stock outstanding, with prior Imara stockholders owning approximately 16% and prior Enliven stockholders holding approximately 84%.

Knowledge-driven hypotheses, data-supported speculation, and analytically-derived methodologies

Our findings suggest the market is currently rewarding emerging-growth companies in technology-intensive industries (particularly biotechnology) that are mature relative to the majority. Advantage is far less connected to present revenue levels than it is to stage of development, probability of intangibles value appreciation over the next three to five years, and potential sales and earnings power.

When the market for the most speculative companies in our industry groups begins to turn, it will happen faster than most investors can even acknowledge and react. But for those who identify the shift early, there will be tremendous value and opportunities to exploit. In the meantime, the best active strategy is a focus on prospects that retain demonstrable assets, a track record of execution, and credible partners and customers.

See you next week, and thank you for your support.

Josh

Connect with me on Twitter and LinkedIn.

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. I do not own shares of companies mentioned.