Emerging Narrative

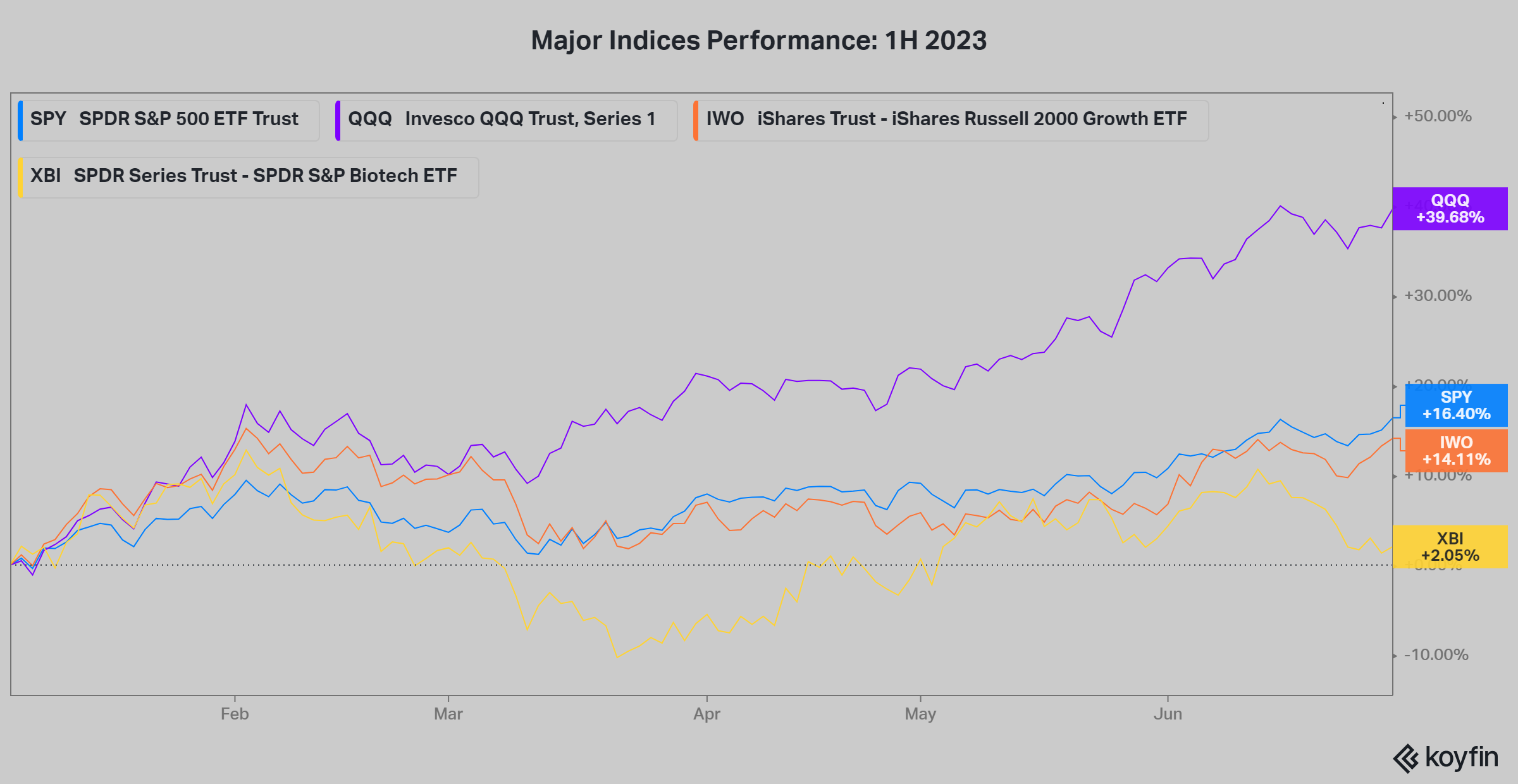

Narrowing gap between small growth stocks and market’s leaders

The valuation disparity between the large-cap S&P 500 and small-cap S&P 600 index has reached its widest point since 2001. The S&P 500 has surged nearly 16% year-to-date, with such momentum that, in early June, it stood 20% above its October low—a level technically defining the start of a bull market.

However, while certain sectors like the Nasdaq-100 and artificial intelligence stocks such as Nvidia (NVDA) have been performing exceptionally well, it is important to acknowledge the narrowness of this market.

Small-cap stocks have struggled to keep pace. The anticipated rotation from large-cap to small-cap stocks at the beginning of June failed to materialize, as the ratio between the Russell 2000 (IWM) and S&P 500 (SPY) hit new relative lows.

Undeniably, the powerful AI narrative has contributed to the success of a handful of major US stocks, including Amazon (AMZN), Google (GOOG), Microsoft (MSFT), Meta Platforms (META), and Nvidia (NVDA). The top 10 companies in the S&P 500 accounted for 12.9% of the index's 16.9% gain in the first half of the year.

Interestingly, beyond their AI connections, these top performers share something else in common: significant losses in 2022, when the group experienced an average decline of over -50% from their 2021 peak. This prompts some skepticism about the exclusive influence of the AI theme, according to the Financial Times’ Robin Wigglesworth. “If AI were truly the driving force, why are 40% of Nasdaq composite stocks still down 75% or more from their two-year highs?”, he asks.

For 1H 2023, the two leading small-cap indexes—the S&P SmallCap 600 and the Russell 2000—have only seen modest gains of 4% and 6% respectively, while the biotech sector continues to struggle, with the SPDR S&P Biotech ETF (XBI) achieving a mere 2% increase. However, the Russell 2000 Growth ETF (IWO) has posted a respectable 14% gain, as depicted in the chart above.

It’s fascinating that this underperformance coincides with strong public sentiment favoring smaller companies.

According to a recent Gallup poll, small businesses enjoy the highest level of public trust among US institutions, with 65% of Americans expressing a great deal or fair amount of confidence in them. Additionally, the military is trusted by 60% of respondents, while the police only garnered the same level of confidence from less than half, at 43%.

Note that the U.S. Small Business Administration defines small business by revenue (ranging from $1 million to over $40 million) and by employment (from 100 to over 1,500 employees). An overwhelming majority of micro-cap firms, and many others in the small-cap tier, fit the bill.

Today a new narrative is emerging, suggesting that the fortunes of smaller stocks may be changing, making them an attractive investment choice versus large-caps for the first time in over 20 years.

Indeed, even smaller companies, more susceptible to economic fluctuations, have begun to join the market rally. The Russell 2000 index rose 7% in June after experiencing a 0.7% decline in the first five months of the year.

Yardeni Research regularly compares the forward price-to-earnings ratios of the S&P 500 and the S&P 600. Currently, the forward P/E ratio for the large-cap index stands at 19.1, while the small-cap index carries a forward multiple of 13.4. This represents the largest valuation gap between the two indexes since the dot-com bubble burst in 2001.

Historically, such wide valuation gaps between the S&P 500 and S&P 600 have ultimately narrowed significantly. Following the dot-com bubble, by late 2002, the forward earnings multiples for both indexes were nearly identical. Presently, there is a compelling argument that large-cap stocks are overvalued while small-cap stocks remain relatively undervalued.

The S&P 500 exhibited a higher forward earnings multiple in the latter part of 2020 through late 2021. Apart from that period, the large-cap index has not been this expensive since its post-dot-com bubble decline.

Meanwhile, the S&P 600 is rebounding from one of its historically lowest valuations based on forward earnings multiples. The only times when small-cap stocks were cheaper were during the 2008 crash and the COVID-19 sell-off in 2020.

‘Adventure Stocks’ Up 12% in 1H 2023

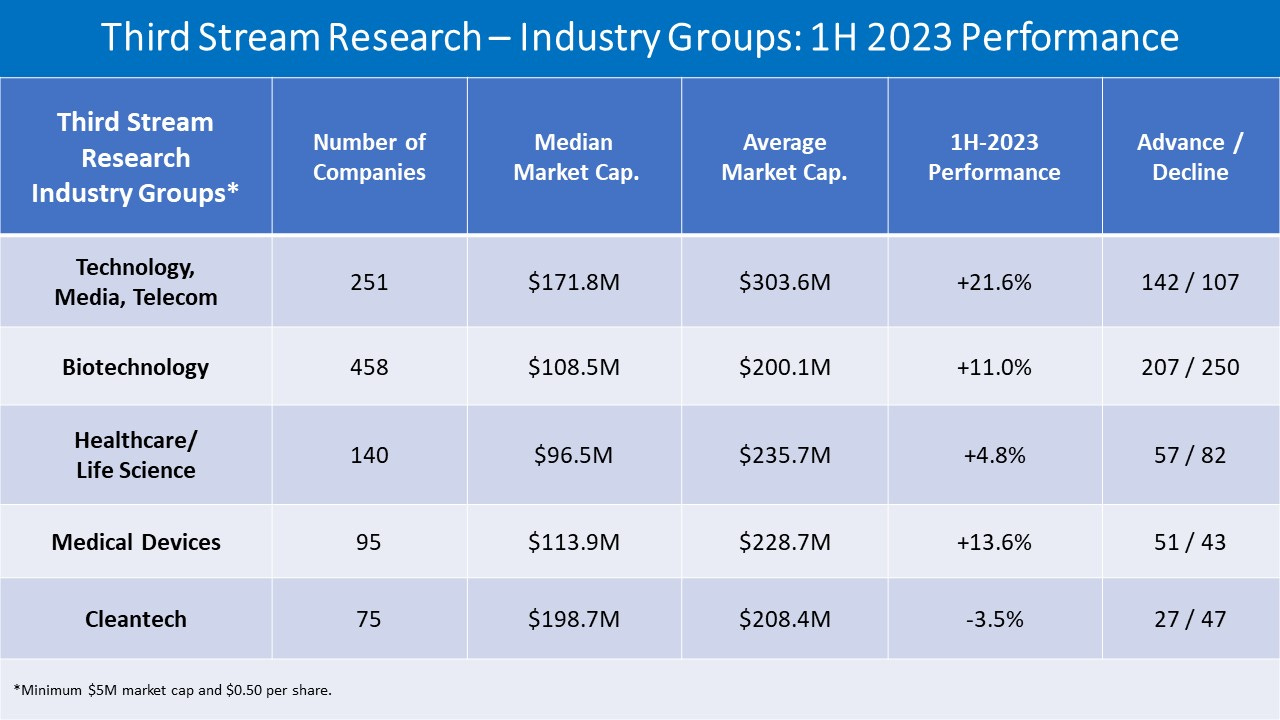

Third Stream Research tracks 1,200+ companies with market capitalizations up to $1 billion, covering the TMT, Biotechnology, Healthcare/Life Science, Medical Devices, and Cleantech industries. This universe of stocks is more diverse than most people think, so it’s crucial to understand the ecosystem and how it compares to the broader market.

In the top quintile of market capitalization, an impressive number of companies have successfully transitioned from micro-caps into formidable small-caps, while a modest portion are on the fast-track toward mid-cap status. Investors mining here will find a rich vein of strong prospects to explore.

At the low end (first quintile), we find a high percentage of revenue-challenged companies with sub-$1 share prices and market caps below $20 million. Unsurprisingly, cash issues loom large for many in this group, as does the potential for stinging dilutive events. In fact, every month brings another handful of firms to the end of their line—with announcements of mass layoffs, bankruptcy filings, and asset yard-sales.

Including all 1,200+ companies in the performance data (which measures the average percentage change), skews the numbers too heavily toward the weakest firms with immaterial market values and excessive volatility. Thus, we’re continually fine-tuning our process to accurately report what’s happening in this thorny area of the market.

For 1H 2023, we set minimums for market capitalization and share price at $5 million and $0.50, respectively. These yardsticks generated 1,019 companies with an average gain of +12.0% and average market-cap of $234 million.

The chart below highlights the performance of Third Stream Research’s five industry groups. Technology/Media/Telecom (TMT) led the way with a +21.6% gain for the first six months of 2023, and winners topping losers by a 142-to-107 margin. Cleantech (-3.5%) notched the only loss, with only two companies appearing on the list of 76 stocks that minimally doubled over this period.

Emerging growth stocks gained ground overall, yet several of the first half’s biggest winners came from a TMT sector that was arguably 2022’s biggest loser: crypto. Bitcoin mining stocks mounted impressive rallies with a handful players ranking among the top 50 performers. Their performance is closely correlated with the price of bitcoin, which is up 85% this year to more than $30,000.

Marathon Digital Holdings (MARA), the largest bitcoin miner with a current market cap of $2.3 billion, is up 297% this year. It’s a prime example of small-cap to mid-cap transformation—at least for now.

Biotech Dominates Top Performers in 1H 2023

Companies developing new and advanced therapeutics, even in the early stages, continue to make their mark among the best performers. Naturally, this is largely due to the binary nature of business models dependent on clinical trial results.

Ambrx Biopharma (ANAM; $985M) led all stocks tracked by Third Stream Research with a 7x return for the first half of 2023. ANAM, which had closed at $1.48 on February 13, recently traded above $16. Yet, stunning as this move is, ANAM remains below its June 2021 IPO pricing of $18. The stock’s surge this year is due to a series of positive reports on early-stage trails for treatments of prostate and breast cancer.

The biotech industry is experiencing a resurgence, fueled by the Federal Reserve's decision to halt rate hikes and a positive market sentiment. William Blair's investment banking team's recent quarterly review indicates that sentiment in the U.S. biopharma sector has rebounded after reaching a low point in the summer of 2022. The second quarter witnessed notable M&A activity, with 16 transactions amounting to $29.1 billion in deal value.

Eli Lilly's acquisitions of Sigilon Therapeutics and Dice Therapeutics for $35 million and $2.4 billion, respectively, along with GSK's $2 billion purchase of Bellus Health, were among the noteworthy deals. These transactions primarily involved later-stage assets that pharmaceutical companies can utilize to offset potential losses resulting from the expected expiration of patent exclusivity for key drugs.

De-risked acquisitions of phase 2 or higher biopharmas accounted for 92% of public acquisitions, while smaller companies pursued reverse mergers to gain access to public markets.

The biotech XBI index has lagged behind other major indices, indicating a challenging fundraising environment for investors. However, the renewed interest from generalist investors can be attributed to the significant M&A deals that have garnered attention.

In this environment we expect a gradual increase of reverse mergers and modest recovery in the IPO market—two examples being the recently priced public offerings of Apogee Therapeutics and Sagimet Biosciences.

Two small biotechs rocket on M&A deals

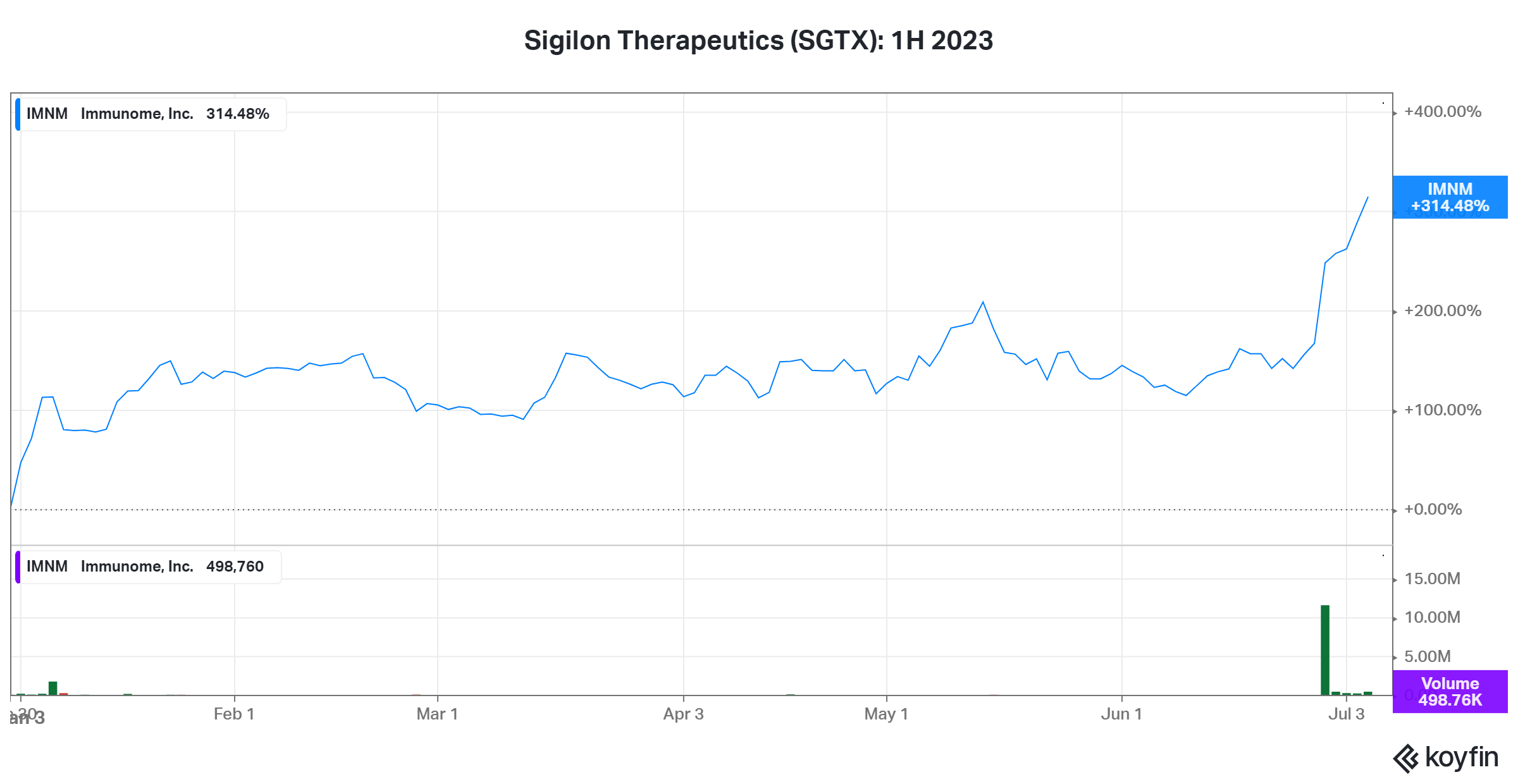

Eli Lilly (LLY; $427B) will acquire all the shares of Sigilon Therapeutics (SGTX; $54M) that it did not own to gain access to experimental cell therapies that can provide longer-term solutions for diabetes patients.

Pharmaceutical giant Eli Lilly has announced its plans to acquire Sigilon, a provider of diabetes drugs and insulin, solidifying its position in the market. As of March 27, Lilly already held a significant 8.44% stake in Sigilon, and now aims to acquire the remaining shares for $14.92 each, amounting to an upfront cash payment of $34.6 million.

Following the news, Sigilon's shares experienced an extraordinary surge of over 500%. Yet SGTX is priced at a fraction of the $1.5 billion market cap it had reached at the end of 2021. This is little consolation for the investors who paid huge multiples of the current price.

Still, the total compensation offered under the agreement could potentially reach an impressive $125.56 per share or $309.6 million if specific developmental, research, and regulatory milestones are achieved.

Shareholders of Sigilon stand to benefit from contingent payments, including an initial cash amount of $4.06 per share upon the first administration of a specified product during the inaugural human clinical trial. Furthermore, they may receive $26.39 per share in cash upon the completion of the first human clinical trial for registration purposes and an additional $81.19 per share in cash upon securing the first regulatory approval for a specific product.

Eli Lilly's acquisition of Sigilon is poised to contribute to the company's ongoing endeavors in the development of advanced treatments for both acute and chronic ailments, with a particular focus on addressing the challenges associated with type 1 diabetes. Recently, Eli Lilly garnered attention when it revealed positive results from a trial of its experimental diabetes and obesity drug, Retatrutide, showcasing the potential for patients to lose an average of up to 24% of their weight.

This outcome surpasses the efficacy of rival drugs such as Novo Nordisk's Ozempic, which demonstrated an average weight loss of 15% among patients. With the acquisition of Sigilon, Eli Lilly may enhance its portfolio of diabetes therapies and solidify its commitment to developing groundbreaking solutions for individuals battling chronic conditions.

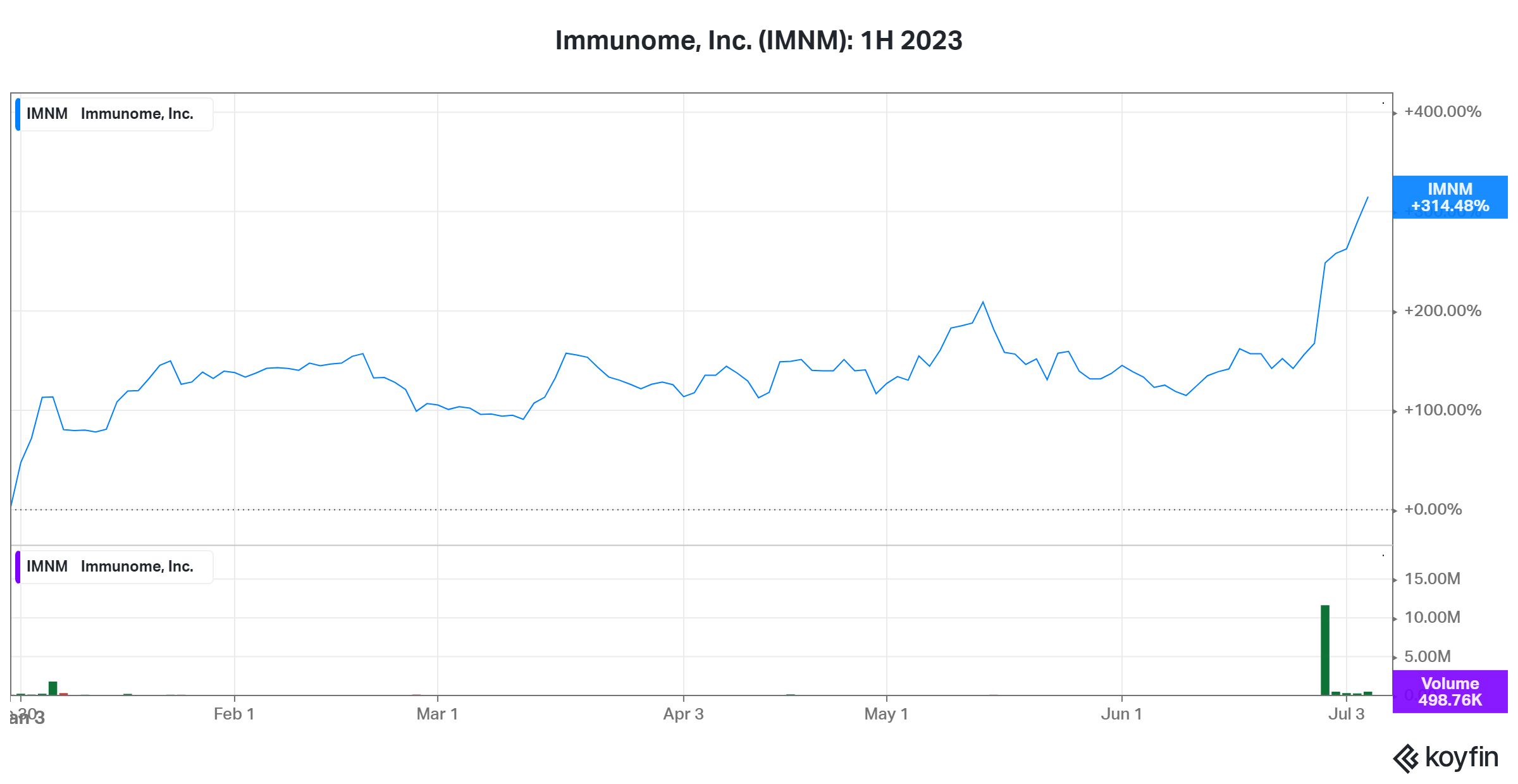

Immunome (IMNM; $101M) surges on merger agreement with Morphimmune, a private biotechnology company developing innovative solutions for challenging cancers.

Immunome and Morphimmune received unanimous approval from their respective boards of directors for an all-stock transaction. The merged entity will operate under the name Immunome and retain its ticker symbol.

Under the terms of the deal, Immunome will acquire Morphimmune through a reverse subsidiary merger, with Immunome's shareholders anticipated to own 55% of the stock.

The companies are raising $125 million through an oversubscribed private placement investment. Prominent institutional investors played a significant role in this funding round, showcasing their belief in the merged company's potential. Both the merger and private placement are expected to close by the end of Q4 2023.

Shares of Immunome scored an impressive rally this year, surging over 300% as of June 30, in stark contrast to the industry's overall decline of 9.8%.

This strategic move brings together the expertise, technologies, and pipelines of Immunome and Morphimmune, with the aim of expediting the development of therapies in the battle against cancer.

Proceeds from the private placement will be instrumental in advancing Immunome's combined pipeline. The company's research candidates include a revolutionary anti-IL-38 monoclonal antibody, a folate receptor-targeted TLR7 agonist, and a FAP-targeted radioligand, all aimed at combating cancer through innovative mechanisms.

The merged company plans to submit three investigational new drug (IND) applications within 18 months of the transaction's closure. Notably, the anti-IL-38 program is scheduled for an IND submission in Q1 2024. Pre-clinical studies have shown promising results, indicating that targeting IL-38 with antibodies helps activate the body's natural tumor-fighting mechanisms.

See you next week.

Josh

Connect with me on Twitter and LinkedIn.

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. Joshua Levine and Third Stream Research were not compensated by any company, directly or indirectly, mentioned in Confluence, and we do not own shares in any companies mentioned.