Biotech Triumphs and Perils

Biotech Triumphs and Perils

A high-wire act for smaller companies

The stock market is a constant tug-of-war between risk management and reward maximization. Investors of companies developing new therapies and other medical advancements are familiar with the thrill of victory and agony of defeat that comes with the territory.

Anticipation in the weeks and days leading up to the release of data on late-stage clinical trials is an intense period for traders and investors who place big bets on either the long or short side. Moves in stock prices can be wild after news hits, with share prices in smaller firms often spiking up or down 50% and higher.

A great behind-the-scenes recounting of a fascinating episode is delivered by Sheelah Kolhatkar in “Black Edge: Inside Information, Dirty Money, and the Quest to Bring Down the Most Wanted Man on Wall Street”. Her book goes inside the long investigation by the SEC, FBI and the U.S. attorney in the Southern District into SAC Capital, the biggest hedge fund, and its founder and leader Steven A. Cohen.

Central to the Feds’ case was evidence surrounding massive bets on Elan and Wyeth, which had spent hundreds of millions of dollars formulating and testing bapineuzumab (‘bapi’) – a drug with prospects to diminish the effects of Alzheimer’s.

Cohen liked to make trades based on ‘catalysts’. The presentation of bapi clinical data at a big medical conference was a classic catalyst: if the results were promising, the stocks would soar, and Cohen and SAC would make a fortune since it appeared they had accumulated a huge position in Elan and Wyeth.

The backstory is extensive and reads like a suspense novel. So let’s quickly jump to the punchline. As soon as the bapi data was presented to the crowd, it became clear that the bapi trials had not been an unqualified success. When the market closed the following day, Elan’s stock had plummeted 40 percent. Wyeth’s had dropped nearly 12 percent.

Before the presentation, however, SAC Capital no longer owned any stock in Elan or Wyeth. In the eight days preceding the conference, Cohen had liquidated his $700 million position in the two companies, and had then proceeded to short the stocks, making a $275 million profit. In a week, Cohen had reversed his position on bapi by nearly a billion dollars.

Amazing gut instincts? Nope. It just took a private screening of presentation data by one SAC portfolio manager – before its release to the public.

How Do Small Biotech’s Stack Up?

Such pivotal events for the biopharma industry happened more frequently when many of the big firms relied on blockbuster drug sales. Now, as their patents expire, companies are increasingly devoting resources to targeted or specialized therapies or treatments, which has boosted demand for acquisitions of smaller developers immersed in research and development.

Biotechnology is a complex business fraught with uncertainties. With several hundreds of biotech firms in the $50 million to $2 billion market-cap range, it’s a challenge separating potential winners from losers. And because many ventures are in the development stage and lack cash flow, earnings or revenue, traditional financial analysis isn't much help.

Investors of small/microcap biotech companies must rely on qualitative analysis rather than quantitative methods of valuation. Which factors are the most important?

Product pipeline (tech platform, multiple opportunities, later stage clinical trials)

Patents (protection, exclusive rights)

R&D (track record, originality)

Management (experience in commercialization, meeting milestones, capital discipline)

Partnerships (commitment, ample terms/payments)

Financial resources (strong balance sheet/cash reserves)

Global R&D spending by the largest publicly-traded biotech companies grew 13.7% annually, from $4.8 billion in 2001 to $55.0 billion in 2020, according to the Tufts Center for the Study of Drug Development. And, by the end of 2020, 478 biotech products had won marketing approval in the USA, up from 127 approvals at the end of 2001, posting a 7.2% annual growth rate.

In 2019, large-cap biotech companies had spent about 24% of revenue on R&D, while their small-cap counterparts spent more than five times their revenue on R&D.

In stock performance, small-cap biotechs are lagging this year. Larger biopharmas, who have been supplying the world with Covid-19 shots and treatments, are carrying the load. Moderna and BioNTech are up 324% and 180% year-to-date respectively, while drug giant Pfizer has recorded a 21% gain.

There are now almost 187 million people fully vaccinated against Covid-19 in the U.S., with another near 6.8 million having received a booster shot, according to the CDC. Close to 10% of Americans over the age of 65 have now received a booster dose, the CDC data shows.

Gains for biotech stocks have historically been led by the larger companies with the rest of the group following, reports Bloomberg. And potential catalysts ahead for small-caps include positive results in clinical trials and clarity out of Washington on issues like mergers and acquisitions and drug pricing regulation.

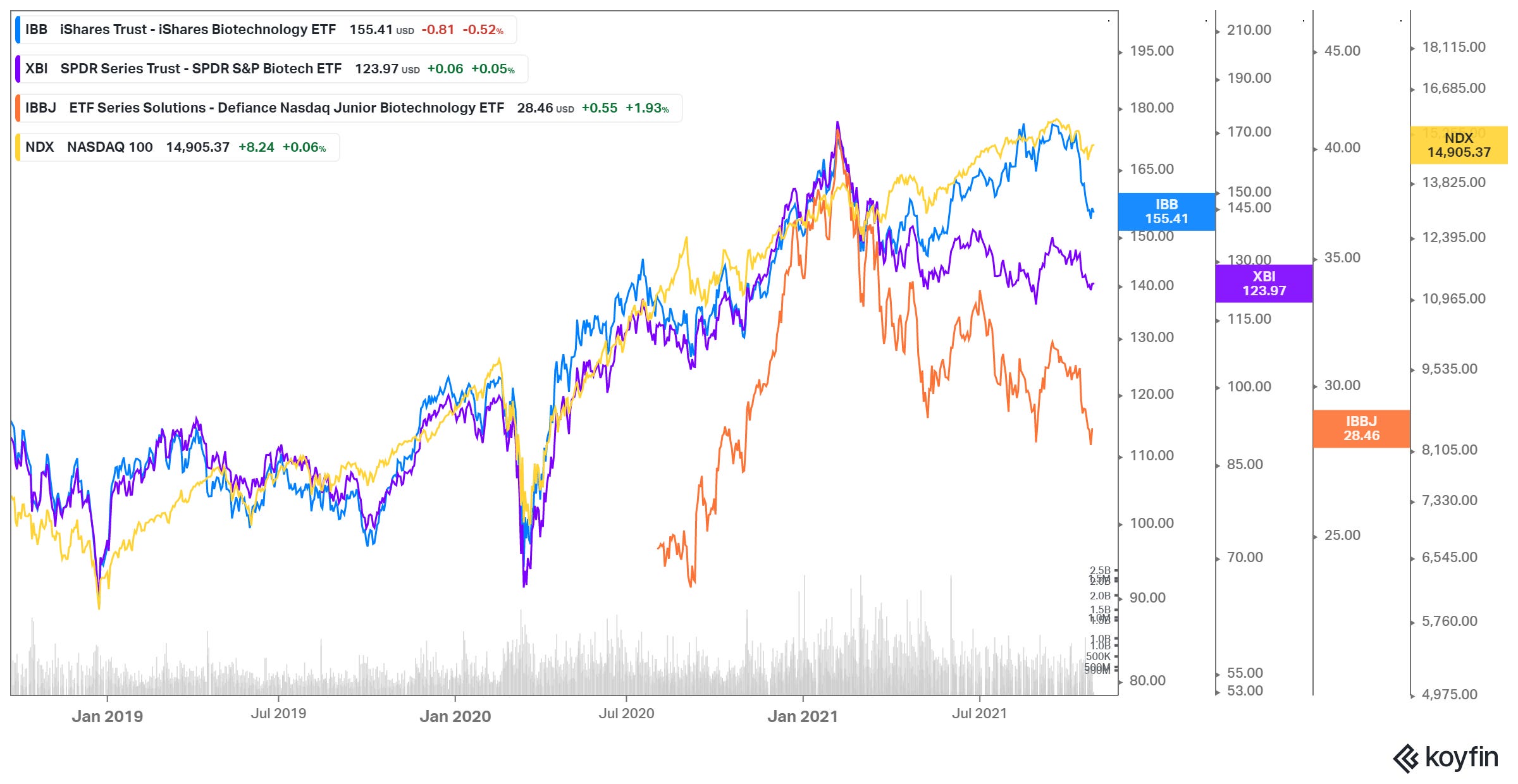

The chart below shows how wide the performance gap has been this year between the large biotechs and their smaller brethren. Here’s the breakdown:

Year-to-date performance (as of Oct. 8)

QQQ (Nasdaq 100): +15%

IBB (large-cap biotech): +2.4%

XBI (all biotech; emphasizes small) -12.3%

IBBJ (small-cap biotech): -18.8%

The key to success for the iShares Biotechnology ETF (IBB) has been Moderna, the biggest holding for the ETF, which has more than quadrupled this year. IBB’s top 10 holdings represent 51% of assets, with market caps ranging from $33 billion to $121 billion. The five biggest are Moderna (MRNA; 9.07%), Amgen (AMGN; 7.73%), Gilead Sciences (GILD; 6.42%), Illumina (ILMN; 5.41%) and BioNTech (BNTX; 4.35%).

The SPDR S&P Biotech ETF (XBI) also includes Moderna in its holdings. However, it uses a modified equal weighting; no single stock makes up even 1% of XBI's overall holdings, thus providing investors with balanced exposure to biotechs of all sizes.

IBBJ is relatively new, beginning on April 30, 2020. IBBJ’s top 10 holdings add up to 22% of assets, with market caps ranging from $4.6 billion to $10 billion. The five biggest are Intellia Therapeutics (NTLA; 3.04%), Zai Lab (ZLAB; 2.99%), BridgeBio Pharma (BBIO; 2.51%), Fate Therapeutics (FATE; 2.25%) and Beam Therapeutics (BEAM; 2.22%). Despite the market-cap levels of this group, nearly all of IBBJ’s holdings are small and microcap stocks.

The value of the global pharmaceutical market rose from about $390 billion in 2001, to about $1.25 trillion at the end of 2019. Whether for cancer research, or a vaccine or treatment for Covid-19, strong demand is likely to continue with support from government regulation and policies that prioritize these sectors.

Uncertainty on public policy regarding consolidation and drug pricing as well as the appointment of a permanent FDA commissioner has weighed on smaller biotech companies this year. Product approvals or positive clinical data announcements, meanwhile, can always electrify a biotech stock.

Two Biotech Companies, Two Different Paths

To illustrate the perils and triumphs experienced by investors in small and microcap biotechs, it’s useful to review the 2021 storyline for two companies – CorMedix (CRMD) and Xenon Pharmaceuticals (XENE). First, a little background.

CorMedix, with a market cap of $185 million, is developing therapeutic products for the prevention and treatment of infectious and inflammatory diseases. Its lead investigational drug product, Defencath, is an antimicrobial and antifungal solution designed to prevent catheter-related bloodstream infections in patients with end-stage renal disease receiving hemodialysis through a central venous catheter.

CorMedix has reported average annual losses over last five years of $24.6 million on revenues that never exceeded $400,000, and were $200,000 over the last 12 months. Its cash position as of the end of Q2 (June 30) was $78 million.

Xenon Pharmaceuticals’ market cap is currently $1.6 billion, more than three times its level at the start of the year. The company develops therapeutics for neurological disorders, particularly epilepsy. A significant focus of its discovery efforts has been on human channelopathies, enabling Xenon to develop strong capabilities in small molecule ion channel drug discovery and understanding of the genetics of channelopathies.

While the pharmaceutical industry is very interested in channelopathies, a general inability to target ion channels selectively with a pharmaceutical agent has limited the development of more effective or safer therapeutics. Xenon believes it can develop a pipeline of novel ion channel inhibitors for diseases in areas of high unmet medical need.

Xenon had a loss of $60.4 million over the last 12 months. This compares to the average of $31.7 million it reported over the last five years. Revenues are on a better trajectory, rising from zero in 2018 to $6.8 million in 2019 and $32.2 million in 2020.

CorMedix’s Pain Treatment

Early this year, in February, B. Riley analyst Andrew D’Silva issued a bullish note on CRMD. He increased the probability of success related to an FDA approval from 70% to 85% and said that Defencath could save the healthcare system around $1 billion a year. In line with investors’ general optimism about the stock, D’Silva rated CRMD an ‘Outperform’ along with a $25 price target.

On March 1, CorMedix’s shares plummeted 50% premarket after announcing that the FDA declined to approve its DefenCath catheter lock solution, citing concerns at its third-party manufacturing facility. The FDA, in its complete response letter, did not specify the issues; CorMedix intended to work with the manufacturing facility to develop a plan for resolution when the health regulator informs the facility of the specific concerns.

Additionally, the FDA required a manual extraction study to show that the labeled volume can be consistently withdrawn from the vials despite an existing in-process control to demonstrate fill volume within specifications. The agency did not request additional clinical data, and did not identify any deficiencies related to the data submitted on the efficacy or safety of DefenCath from LOCK-IT-100.

In April, CorMedix met with the FDA to discuss solutions to the deficiencies identified in the Complete Response Letter to its marketing application for DefenCath. The discussions also involved the third-party manufacturer who was cited by the FDA in the CRL after a review of the records.

After a few months of relative calm, CorMedix shares plummeted 22% on Sept. 7 after saying it had faced delays at its contract manufacturer. CRMD was informed there were issues unrelated to DefenCath manufacturing activities, and that the timeline to address deficiencies at the facility for resubmission of the DefenCath New Drug Application was uncertain.

The fallout extended to CorMedix’s executive team within weeks. Its CEO retired from his role on Oct. 4, also resigning from the company’s Board of Directors. It went further: the executive VP retired the same day. CRMD reported that the Board initiated a search process for a permanent CEO.

At a current price of $4.89, CRMD shares are down 72% from their Feb. 2021 high.

Xenon Pharmaceuticals Executes Plan

Xenon began 2021 with some major changes in its leadership, too. On Jan. 14, the company named a new CEO and CFO, effective in June. Its previous CEO took on the new role of Executive Chairman and was replaced by the exec who was already president and CFO. The new CFO was previously Xenon’s VP, Finance. This was a well-planned, orderly transition.

In mid-March, XENE raised approximately $100 million at $18.90. With the company’s pipeline in good shape, investors began looking ahead to topline results from the Phase 2b X-TOLE clinical trial, which evaluated the clinical efficacy, safety, and tolerability of XEN1101 – a differentiated Kv7 potassium channel modulator – administered as adjunctive treatment in adult patients with focal epilepsy.

These results were expected in a window from late September to mid-October. Along the way, on Aug. 23, Xenon appointed a new chief medical officer to oversee all clinical development and medical affairs strategies, guiding the development of Xenon’s portfolio of neurology-focused therapeutic programs.

On Sept. 8, the company received a $10 million milestone payment from its Neurocrine collaboration. The company said it expects Neurocrine to initiate a Phase 2 trial for NBI-921352 for the treatment of focal-onset seizures in adults later this year. Upon FDA acceptance of a protocol amendment for NBI-921352 in pediatric patients (aged 2-11 years) with SCN8A-DEE, Xenon is eligible to receive an aggregate payment of $15 million.

Xenon’s momentum culminated last week (Oct. 4). XENE reported positive topline results from Phase 2b X-TOLE clinical trial. The trial met its primary efficacy endpoint with XEN1101 demonstrating a statistically significant and dose-dependent reduction from baseline in a monthly focal seizure frequency when compared to placebo.

XENE’s shares doubled (+102%) in response to the news. But there was an encore by the company on the next day.

On Oct. 5, Xenon priced a public offering of 8.47 million common shares and, pre-funded warrants to purchase up to 1.69 million common shares. The shares and warrants were offered at $29.50 per share and $29.4999 per warrant, respectively. Gross proceeds were expected to be around $300 million.

The differences between CorMedix and Xenon are significant when considering the most important factors – product pipeline, patents, R&D, management, partnerships and financial resources – that small/microcap biotech investors should be monitoring. While nothing is guaranteed in the world of biotech, the companies that rate well across all factors will always have the highest probabilities for success.

See you next week, and thank you for your support.

Josh

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our Website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. I do not own shares of companies mentioned.