Biotech Retrenchment

Hope springs eternal for smallest companies at J.P. Morgan Healthcare Conference

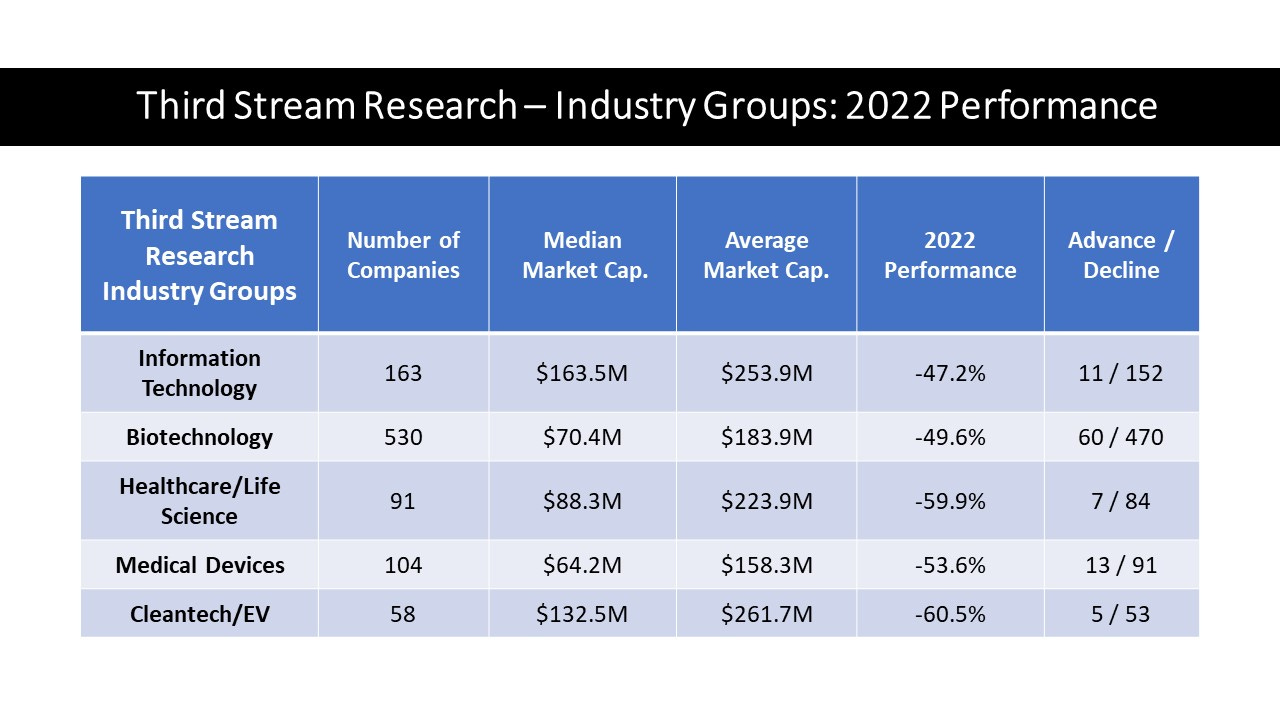

Third Stream Research’s Industry Groups are comprised of Information Technology, Biotechnology, Healthcare/Life Science, Medical Devices, and Cleantech. An essential part of Confluence in 2023 features weekly data, analysis and coverage of the emerging growth universe of technology-intensive companies (<$1 billion market cap).

Biotech investors are braving the rain and wind in San Francisco this week to attend the J.P. Morgan Healthcare conference, widely recognized as the most significant industry event. The annual conference – where biopharma companies large and small announce major corporate news, such as mergers & acquisitions or new research partnerships – returns this year after a two-year hiatus due to the pandemic.

As the economic fallout from the COVID-19 pandemic continues and recession concerns mount, biotech investors come together after one of the weakest years on record. The SPDR S&P Biotech ETF (XBI) fell 30.6% versus the S&P 500’s 19.4% decline in 2022.

Drawdowns were more severe among small- and micro-cap players. Indeed, Confluence reported last week that biotechnology stocks fared slightly better than the overall 2022 performance (-52.1%) for the five industry groups and 946 companies tracked by Third Stream Research.

A total of 530 small- and micro-cap biotechs fell an average of 49.6% in 2022, according to Third Stream Research. The group had 60 advancers and 470 decliners. The average market cap is $183.9 million, and the median market cap is $70.4 million.

A World of Difference

It often becomes crowded at the edges of the performance spectrum for biotechs. The reason is that they operate in a mostly binary world of positive/negative outcomes and assessments for clinical trials. Though losers outpaced winners by nearly an 8-to-1 margin, there were numerous standouts on the upside, including the following 15 stocks that minimally doubled in 2022:

Aveo Pharmaceuticals (AVEO): 218.8%

Merrimack Pharmaceuticals (MACK): 193.1%

BioStem Technologies (BSEM): 187.5%

Astria Therapeutics (ATXS): 176.2%

ADMA Biologics (ADMA): 175.2%

Ardelyx (ARDX): 159.1%

Aerovate Therapeutics (AVTE): 148.5%

Trevi Therapeutics (TRVI): 146.7%

Cabaletta Bio (CABA): 144.1%

CTI BioPharma (CTIC): 142.3%

Voyager Therapeutics (VYGR): 125.1%

Fennec Pharmaceuticals (FENC): 118.2%

Aerie Pharmaceuticals (AERI): 117.2%

GlycoMimetics (GLYC): 110.4%

Viking Therapeutics (VKTX): 104.3%

Shares of the biggest winner, Aveo Pharmaceuticals (AVEO), jumped 72% in mid-October when the company announced it would be acquired by LG Chem (LGCLF) in an all-cash transaction for $15 per share. Aveo shareholders approved the acquisition last Friday. AVEO, a commercial stage, oncology-focused company, currently markets FOTIVDA® (tivozanib) in the U.S. for the treatment of adult patients with relapsed or refractory advanced renal cell carcinoma following two or more prior systemic therapies.

Number two performer Merrimack Pharmaceuticals (MACK) also ended the year with a bang. Its shares rocketed 183% on November 8 after its French partner for cancer therapy Onivyde, Ipsen S.A (IPSEF) said that the drug as a combination therapy met the primary endpoint in a late-stage trial for a form of pancreatic cancer. In 2017, MACK sold Onivyde to Ipsen and is entitled to receive up to $450 million in milestone payments related to the transaction. Interestingly, MACK does not have any ongoing R&D activities or employees; instead it uses external consultants for the operation of the company.

Unhappily, celebratory pivotal events in the biotech industry were the exceptions in 2022. Biotech investors’ patience was frequently tested by early-stage-focused pipelines and disappointing clinical results. In fact, 1-in-8 (67) suffered a price loss of 90% or worse; another 116 firms suffered drops between 75% and 89%.

A closer look at the data shows that an increasing number of biotechs are confronting an existential reckoning – one that will increasingly result in gut-wrenching decisions for corporate management and boards:

201 (38%) biotech companies are now worth less than the amount of cash they have in the bank.

109 (20%) have cash positions below $15 million.

Clearly this plight didn’t just appear overnight. Confluence warned about this condition and the inevitable fallout nearly 10 months ago: Small Biotech: Risk of Investor Burnout - Plummeting shares raise specter of costly financings (March 14, 2022). We wrote:

“Biotech stocks have been pummeled this past year. With prices sharply lower for so many companies, they confront an increasingly challenging road ahead. That’s because future stock sales may come at a far steeper cost than had been strategized six or twelve months ago.

Valuations have fallen so much that there are about 100 biotech companies whose cash stockpiles exceed their stock-market values, according to Truist, indicating that investors are deeply discounting the outlook for growth. This is up from two companies a year ago.

Additionally, more than one in four biotechs that went public in 2020 are trading below cash, according to a new STAT analysis of data from Sentieo – powerful evidence that too many biotechs raced to market in 2020, when drug developers capitalized on their lifesaving mission as the COVID-19 pandemic raged.”

This week, STAT reports that two-thirds of the 100 biotech and pharma executives recently surveyed by the publication said that financing – raising venture capital, launching an IPO, or selling additional stock to further fund R&D and other operations – will be a headwind in 2023. Then there are the current economic storm clouds, which will have varying effects on biotechs.

If a recession unfolds, biotechs may feel driven to adopt new technologies to save on costs. Such investments can lead to greater efficiencies and improve the way biotech scientists work. Other areas, such as R&D, are unlikely to see any changes due to a recession, at least not immediately.

Clinical trials, however, may face additional difficulties unless biotechs adopt technologies which will make the process more economical. Still, biotech management grappling with tight budgets and experiencing revenue losses may feel pressured to partner with larger pharma companies, or even agree to an acquisition. When such options fail to materialize, biotechs could be forced into more desperate measures.

Clinical Trials and Tribulations

Failed clinical trails often have a devastating impact on the stock price of a small biotech. Most of these companies have narrow pipelines, so any setback in one of their primary drug candidates – often based on their main scientific platform – can send investors fleeing for the exit. Let’s look at a few situations from December.

Raised liver enzymes had already struck both Centessa Pharmaceuticals (CNTA) and Surrozen (SRZN). Third Harmonic (THRD) was the latest company to discontinue a phase 1b study of its lead asset over two reports of liver toxicity. The news sent the biotech’s shares plummeting 78% on December 15. The trial in an inflammatory skin condition called chronic inducible urticaria was designed to evaluate the safety, efficacy and pharmacokinetics of three dose levels of the drug and lead asset, dubbed THB001, over 12 weeks of treatment.

Third Harmonic’s $300 million in cash as of Q3 2022 indicates it has the capital to march onward. But not all biotechs suffering from clinical trial disappointment have the resources to maintain status quo or workforce levels.

After missing its primary goal in Phase 2a trials for its long Covid drug, Axcella Health (AXLA) announced on December 15 that it will cut 85% of its workforce (including CFO), has hired a bank to explore strategic alternatives, and is reshuffling its pipeline. AXLA had raised approximately $30 million in mid-October, bringing its cash position to nearly $60 million. The financing occurred at a market price of $1.64. AXLA closed at $0.35 yesterday.

Clinical trial disappointments have also led Sensei Biotherapeutics (SNSE) and Instil Bio (TIL) to lay off 40% and 60% of employees, respectively. A trial flop on its lead program, pushback from a German billionaire stockholder and a massive stock slide preceded the pipeline makeover at Sensei. The biotech had 44 full-time workers as of November 1 and planned to shutter its Boston research site, leading to 17 workers let go.

Instil had 463 employees at the end of June. In conjunction with the major reorganization, Instil axed a Phase 2 trial of its asset ITIL-168, which was being investigated in patients with advanced melanoma, and also folded a Phase 1 study testing the autologous cell therapy – in combination with Keytruda – in patients with advanced solid tumors.

This is just a tiny sampling of the layoffs that occurred in the biotech industry during 2022. Fierce Biotech, which recorded 119 total layoffs among biotech companies in 2022, said that November was the toughest month of the year with 23 and December the slowest, with just three as of December 15.

Financial Engineering

When stock prices fall into the penny range, companies seize on reverse stock splits as a last resort to raise the stock price to maintain compliance for listing and stay on the radar for the most tolerant institutional investors. We highlight three since mid-December.

Biora Therapeutics (BIOR), a biotech focused on oral biotherapeutics, announced a 1-for-25 reverse stock split, dropping the number of authorized shares of its common stock to 164 million from 350 million. 180 Life Sciences (ATNF) effected a 1-for-20 reverse stock split of its common stock to reduce the number of shares of common stock issued and outstanding from ~40.5 million to ~2.0 million. Sintx Technologies (SINT) declared a 1-for-100 reverse stock split, reporting that it was primarily intended to bring the company into compliance with the minimum bid price requirements for maintaining its listing on the Nasdaq.

Other biotechs effected reverse stock splits that were followed soon after by financings. Here are two examples:

CNS Pharmaceuticals (CNSP), a biopharmaceutical company specializing in the development of novel treatments for primary and metastatic cancers in the brain and central nervous system, announced a 1-for-30 reverse split on November 28. Two days later, CNSP priced a $6 million public offering. The stock lost more than half of its value within days.

OncoSec Medical (ONCS) effected a 1-for-22 reverse split on November 9. Two weeks later, ONCS raised $3.5 million in an offering of common stock and warrants priced at $3. The stock, which was down 80% in November, closed at $2.15 yesterday.

Biotechs that completed similar financings that did not align with reverse stock splits also received hits to their share price.

Hoth Therapeutics (HOTH) lost 38% December 15-19 after announcing a private placement to sell 2 million shares of its common stock and warrants to raise $10 million in gross proceeds. The private placement followed more than a twofold rise in HOTH shares after the company announced that the FDA accepted its application to begin a clinical trial for HT-001, a treatment for rash and skin disorders linked to cancer therapy.

After Erasca, Inc. (ERAS) priced an underwritten offering of 15.4 million shares at a price of $6.50 per share to net $100 million, the stock slid to below $4 over the subsequent two weeks. Sporting a current market cap of $557 million, ERAS focuses on discovering, developing, and commercializing therapies for patients with RAS/MAPK pathway-driven cancers.

Biotech’s IPO market cooled off last year with only 17 public issuances. This followed a hot streak that lasted from 2013 to 2021, when a total of 494 IPOs were completed, peaking at 96 in 2021. Interestingly, based on the LTM sales reported in the prospectus at the time of the IPOs, only 68 of the 494 companies went public with zero sales, though many of the companies with positive sales have research contracts producing revenue, rather than product sales. (Source: Jay R. Ritter, Cordell Eminent Scholar Warrington College of Business, University of Florida; January 5, 2023).

Small biotech’s struggles in the public market continue to carry over into the IPO pipeline. New issue candidate Melt Pharmaceuticals withdrew a $15 million IPO on January 4. A Phase 2 biotech developing non-opioid, non-IV sedatives and anesthesia, Melt had originally filed in September 2022.

Still, two tiny newbies did manage to clear the hurdle in recent weeks.

ALS drug developer Coya Therapeutics (COYA) completed its IPO on January 3. It consists of 3.05 million shares of its common stock and accompanying warrants to purchase up to 1.525 million shares of common stock. Each share and accompanying warrant were sold at a combined offering price of $5.00, for net proceeds of $13.2 million. COYA closed at $4.93 yesterday. COYA is focused on the biology and potential therapeutic advantages of regulatory T cells to target systemic inflammation and neuroinflammation.

Lipella Pharmaceuticals (LIPO) set sail on December 21 after closing of IPO offering of approximately 1.2 million shares of its common stock at $5.75 per share. The gross proceeds were about $7 million. In October, Lipella downsized its proposed IPO to $7 million from around $12 million. LIPO closed at $3.11 yesterday. The company is reformulating existing generic drugs for new purposes. Its lead product, LP-10, is in Phase 2 testing for the treatment of chronic, uncontrolled urinary blood loss associated with chemotherapy or pelvic radiation therapy.

Barron’s correctly observes that attendees at the J.P. Morgan Healthcare conference “will be looking for evidence of shifting attitudes toward biotech IPOs, which dried up last year amid a sense that too many companies had been taken public too early during the rush of 2021 and 2020.”

Considering the macro headwinds and market volatility, we would not be surprised if investors pause this year to reassess their biotech portfolios, especially for any micro- and nano-cap positions for which the clock is running out.

See you next week, and thank you for your support.

Josh

Connect with me on Twitter and LinkedIn.

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. I do not own shares of companies mentioned.