3D-Printing Entanglements

Will consolidation among the leading additive manufacturing firms add up?

Additive manufacturing, commonly known as 3D printing, has contributed in many ways to transform the engineering landscape. Notably, the technology speeds prototyping, reduces manufacturing costs, enhances product customization, and elevates product quality. These advantages have spurred adoption of 3D printing across industries.

For aerospace and defense companies, which use highly complex parts produced in low volumes, 3D printing is ideal. Using the technology, complex geometries can be created without having to invest in expensive tooling equipment. Automotive, manufacturing, medical and dental applications are also among the highest use cases.

Unlike a sculptor who cuts away clay, 3D printing works by adding layer upon layer of material; thermoplastics are most frequently used, but photopolymers, epoxy resins, and metals, are also popular choices. In essence, product designers and engineers upload a digital (CAD) file to a 3D printer, which then prints a solid 3D object.

According to 2022 reports by Emergen Research, 3D HUBS, IDTechEx, the additive manufacturing and additively manufactured electronics market, which consists of the sales of parts and the systems that make them, is expected to grow from $16 billion to more than $100 billion by 2030 at a CAGR of above 20%.

Stratasys: the main ingredient in the layer cake

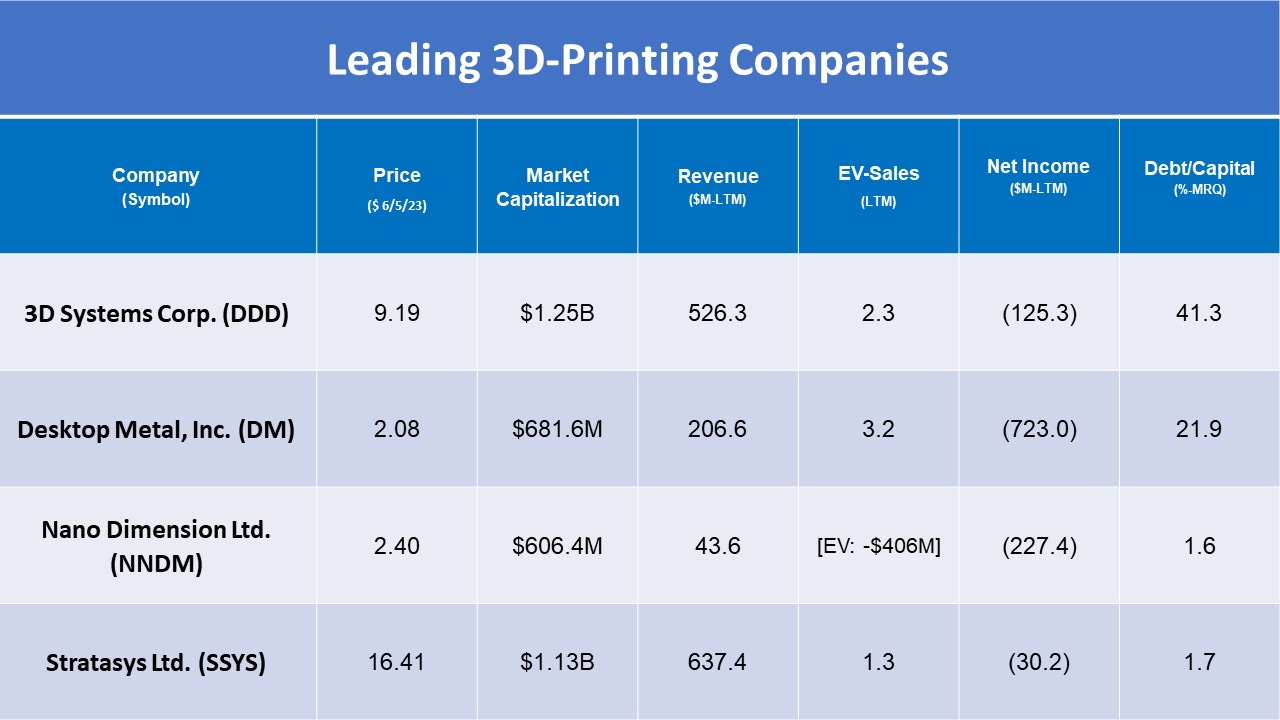

Stratasys (SSYS; $1.13B), a dominant player in polymer-based industrial 3D printing, has experienced a whirlwind of events in recent weeks. Following the announcement of its merger plans with Desktop Metal (DM; $682M), the company now finds itself in the midst of an unexpected twist. 3D Systems (DDD; $1.25B), another prominent industry giant, has made an unsolicited bid to acquire Stratasys.

Jeffrey Graves, CEO of 3D Systems, referred to “the compelling logic of merging our two businesses” as he urged the Stratasys Board of Directors to engage with their proposal and translate this vision into reality for the benefit of both companies' stakeholders, employees, and customers.

On May 25, Stratasys had unveiled its plan to acquire Desktop Metal in a $1.8 billion all-stock transaction, seeking to merge a trailblazer in metal 3D printing with SSYS. 3D Systems, a formidable player in its own right, tabled its own bid for Stratasys a few days later.

3D Systems offered to acquire Stratasys for $7.50 in cash and 1.2507 newly issued shares of DDD common stock. Stratasys holders would own 40% of the combined company and receive approximately $540 million in cash.

If you haven’t been following the 3D printing industry, you’ll be surprised to learn there’s one more company in the mix.

On March 9, Nano Dimension (NNDM; $606M) had offered to acquire Stratasys for $18 a share in cash. Stratasys surged 14% in after hours trading; Nano Dimension fell 6.5%. At the time, the offer represented ~30% premium to SSYS’ stock price.

Nano Dimension, which has a negative enterprise value of -$406M with $1B in cash, had “constructive, informal” talks with the Stratasys regarding the non-binding offer and the merits of a combination, according to a statement. NNDM had stated in a letter to SSYS's board that it was prepared to complete due diligence and negotiate a definite agreement within 30 days.

Notably, Nano Dimension has been Stratasys's largest shareholder since July 2022 and currently owns a 13.7% stake on a fully diluted basis. In July 2022, Stratasys adopted a limited shareholder rights plan or ‘poison pill’ shortly after NNDM disclosed that it had a acquired a 12% stake in SSYS. The poison pill would go into effect when a person or group acquired 15% or more of the company's stock, with the pill set to expire next month, on July 24.

After the board of Stratasys unanimously rejected the unsolicited proposal it received from Nano Dimension, NNDM made two more bids at $19.55 and $20.05, both rebuffed by SSYS.

Nano Dimension has also been battling with a dissident shareholder, Murchinson Ltd., over board seats. Murchinson, a Toronto-based investment firm, which holds ~6.8% of NNDM, in March said it received “overwhelming support” for the removal of three directors and chairman at a shareholder vote, a vote that Nano Dimension called “illegal” and “invalid.”

Nano Dimension appears to have a good track record of making accretive acquisitions of additive manufacturing companies, yet its recent communications with shareholders and Wall Street at large has been a bit unsettling.

Now, returning to the deal between Stratasys and 3D Systems, Credit Suisse analyst Shannon Cross wrote in a note last Thursday that SSYS is likely to reject DDD’s ~$18 a share cash and stock takeover offer. Cross writes:

“We think cost synergies [which DDD claims to be $100 million] would be limited to elimination of duplicative costs, and 3D Systems would likely leverage Stratasys’s higher profitability to increase investment in its bio-printing efforts. We see minimal opportunity for scaling benefit (which is a key point of the SSYS-DM combination) given the businesses are of similar size and manufacturing operations are not centralized for either.”

From our limited perspective, of the three deals currently on the table—NNDM>SSYS, DDD>SSYS, and SSYS>DM—the probabilities appear to be highest for Stratasys acquiring Desktop Metal. But even that faces obstacles, reflected in the negative price action for both stocks following the announcement.

For starters, a “lack of transparency” around the drivers of Desktop Metal's revenue growth and the composition of its product portfolio is a red flag, according to William Blair analyst Brian Drab. He also points out that DM's financials are unattractive, highlighting its operating loss of $233 million in 2022.

The history of the 3D printing industry is filled with countless mergers and acquisitions, with the most pivotal being the Objet (Israel) and Stratasys $3 billion merger in 2012.

Unfortunately, Stratasys’s ambitious acquisition of Objet resulted in a big one-time loss. After spending $624 million to integrate the two companies, Stratasys in Q3-2020 reported a goodwill impairment of $386 million linked to the deal. This impairment primarily represented the premium paid for Objet, hinging on the intangible assets that the management anticipated would materialize in due course.

That big charge accounted for about 87% of the company’s $443 million in losses in 2020, which also was the sixth consecutive year of revenue declines before coming off the trough in 2021.

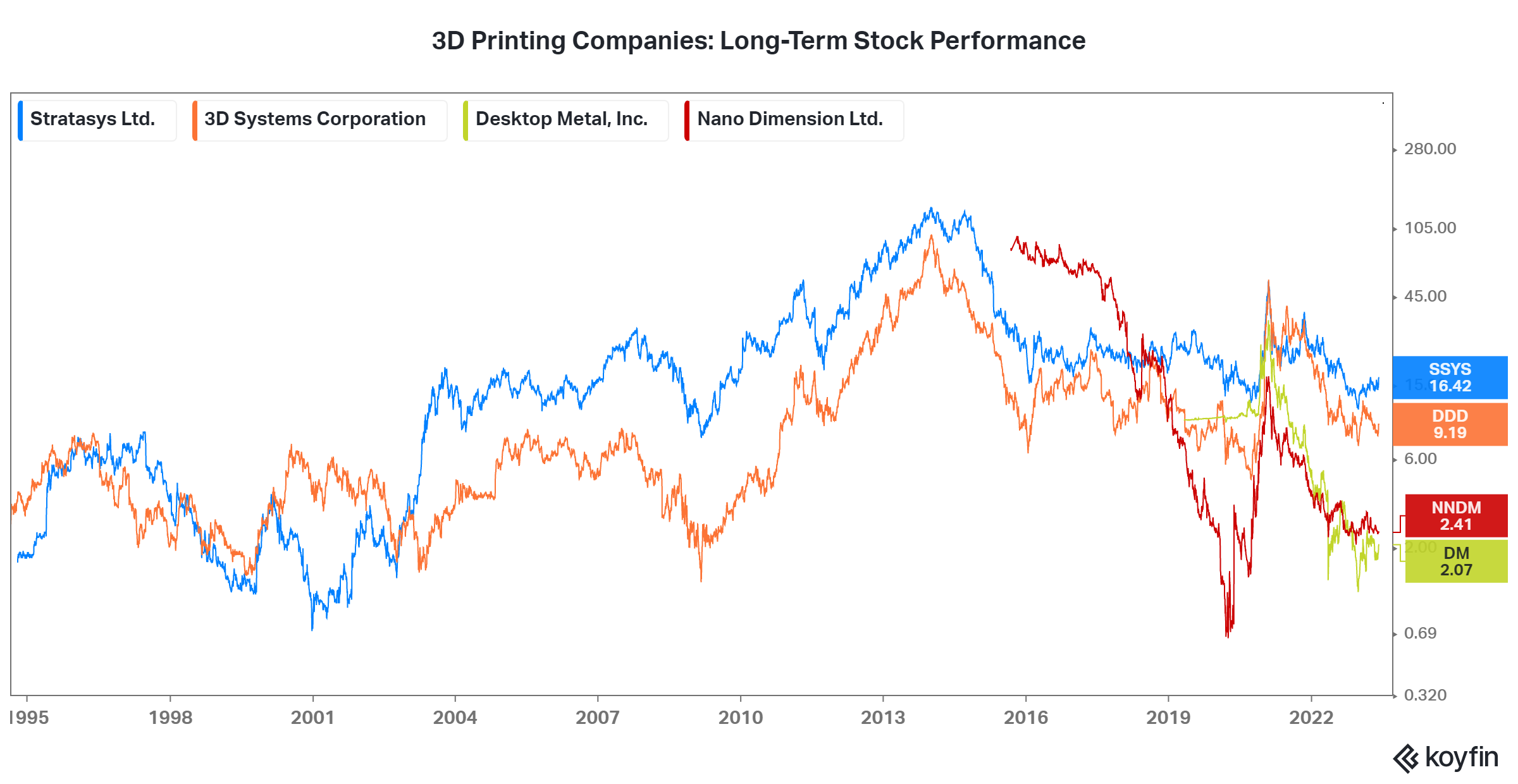

Stratasys’s merger with Objet was an early high-water mark in 3D printing consolidation. In fact, from 2011 to 2016, the majority of M&A deals went to the two largest 3D printing companies, according to CB Insights. 3D Systems drove the bulk of activity with 30 M&A transactions, followed by Stratasys with 6. As the chart below indicates, this correlated with the years when their share prices were at peak levels.

Mergers and acquisitions continued in the subsequent years, for SSYS and DDD as well as other industry players, including several large, diversified industrial firms. But none have rivaled the Objet-Stratasys deal.

Sad truth is that more than two-thirds of all mergers fail to be accretive or fail completely. Similar to big free-agent signings of top athletes, corporate M&A is often better on paper than in reality.

Whether it’s cultural clashes, ego incompatibility among leadership, layoffs and talent flight, or overly-optimistic predictions about cost savings and synergies for technologies and product development, complications inevitably arise in the months and years following the honeymoon.

Questioning consolidation in 3D printing industry

When mergers and acquisitions are managed well and premised on sound strategies rather than get-rich-quick financial engineering, such deals can be a boon to intellectual property and to the bottom line. But M&A, by its nature, can also lead companies into unforeseen labyrinths.

Share prices for the two big players, Stratasys and 3D Systems, are down sharply from their all-time highs, with drawdowns of 85% and 76% respectively.

A large number of acquisitions by Stratasys, 3D Systems and other active players have targeted small private firms for some combination of key personnel, intellectual property, or specialty product and market access. Typically, too little is disclosed about such items once the deals are completed, so it can be difficult for even the most wired-in industry analysts to gauge the success of a particular acquisition and determine what, if any, value was created.

For large deals like Stratasys-Objet, the tale of the tape is revealed only after a massive impairment charge is taken years later. Thus, given the record of consolidation in the 3D printing industry, investors should be skeptical about this latest round in motion for this quartet of top players.

Ultimately, the erratic performance and general lack of transparency of the companies—in part due to the staggering range of acquisitions, product types, and market niches—presents enormous challenges for anyone enticed by the promise and opportunities in additive manufacturing.

See you next week, and thank you for your support.

Josh

Connect with me on Twitter and LinkedIn.

Disclaimer

The content provided in this newsletter is intended to be used for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on our website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. Joshua Levine and Third Stream Research were not compensated by any company, directly or indirectly, mentioned in Confluence, and we do not own shares in any companies mentioned.